Patient readers: One more cross-post while the Internet is out in the Third World country where Yves currently resides. I am to ask if UK readers, especially Colonel Smithers, agree with Murphy’s thesis. –lambert

By Richard Murphy, a chartered accountant and a political economist. He has been described by the Guardian newspaper as an “anti-poverty campaigner and tax expert”. He is Professor of Practice in International Political Economy at City University, London and Director of Tax Research UK. He is a non-executive director of Cambridge Econometrics. He is a member of the Progressive Economy Forum. Originally published at Tax Research UK

A pile of commentators have appeared on this blog over the last day or so telling me that the interventions by the Bank of England in financial markets are in no way related to pension funds and do not benefit them. Many have been deleted for their tone. A few I have posted to make clear just how wrong they are.

Why are they wrong? Because they look at what the Bank is doing by buying gilts through a QE process and say that this does not directly help the funds. It does instead provide liquidity to conventional (and now index-linked) gilt markets. So, they claim that pension funds do not get direct help.

Why do I disagree with them? Because the crisis has been caused by illiquidity in markets caused by gilt sales by pension funds desperate to sell assets to cover calls for collateral cover.

What is the aim of the intervention? It is to take away the need for those urgent sales by funds at what are likely to be undervaluations.

Do the pension funds benefit as a result? Of course, they do. But it’s not direct, and so those criticising me say I have got it all wrong.

So what is going on here? That’s easy to explain. Those who are criticising are looking at what is happening as economists do. They see market interventions as a result of which pension funds need not sell so they say pension funds are not involved. As a political economist, I ask why the intervention is happening, which is so that the pension fund may either not sell, or may do so in an orderly fashion with smaller losses, and so, of course, the pension fund gains.

Which approach is more useful? That is the political economist, of course, because they answer the real questions in life.

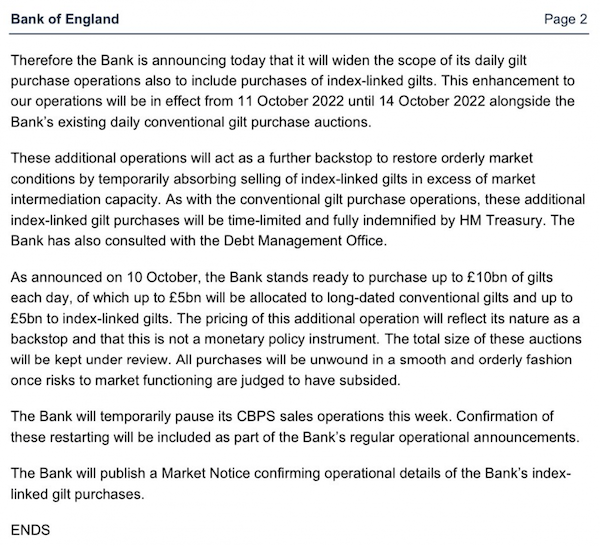

And how do I know I am right? The Bank of England says so. Take these comments from the Bank of England issued this morning as they extend this emergency programme as evidence:

LDI activity is essentially only by pension funds.

Those seeking to make similar comments again today will be deleted.