Yves here. I imagine many will take issue with the headline statement, since the inflation that matters is your inflation, as in the one that shows in the basket of goods and services you buy.

Your humble blogger is still seeing increases in food prices, either overtly or through package shrinkage: in dairy, fish, wine, coffee, snack foods, even staples like frozen spinach and black beans. Eggs may not be rising in price but the baseline is now so high as it feels like they are still rising. Consumers are very sensitive to food prices because food is essential and it’s purchased frequently.

Gas and energy prices generally are down but I am seeing price increases in all sort of places, like connectivity and medical charges. And the only place I have seen a decrease is in cut roses (I was buying them for my mother before she died, so I maintain an interest in this category), which ran up and then ran down to their former price.

Note Wolf Richter has a less cheery take, as telegraphed in his headline: For 7 Months, “Core” CPI Hasn’t Improved at All, Stuck at 2.5x Fed Target. Services CPI Accelerates, Rents Not Playing Along, Used Vehicle CPI Spikes. But Energy Plunged

Readers?

By New Deal democrat. Originally published at Angry Bear

Let me cut to the chase right from the outset: except for the very lagging measures of shelter; motor vehicle parts, repairs and insurance; and to a lesser and waning extent, food; consumer inflation is now well-contained and close to the Fed’s target rate.

First, let’s look at the headlines, with the monthly and YoY rates of change:

Total CPI up 0.1% m/m and 4.0% YoY (lowest since April 2021)

Core CPI up 0.4% m/m and 5.3% YoY (lowest since November 2021)

CPI less shelter up +0.1% and 2.2% YoY (lowest since February 2021)

Core CPI less shelter up +0.3% and 3.4% YoY

Energy down -1.2% m/m and down -11.7% YoY

Food up +0.2% m/m and up 6.7% YoY (lowest since December 2021)

New cars up +0.2% m/m and 4.7% YoY (lowest since May 2021)

Transportation services (parts, insurance, repairs): up +0.8% and up +10.3% YoY (vs. October 2022 peak of 15.3%)

Owners Equivalent Rent up 0.6% m/m and 8.0% YoY (down -0.1% from all time YoY high)

This is the same pattern as we saw last month ago, just even more amplified: “Lowest since…” for almost everything *except* shelter, which is close to its all-time YoY high set one month ago.

And let me further headline that fact right here: CPI less shelter since last June is only up 0.7%:

That’s an annualized rate of 0.8%.

Keep in mind that shelter component of official inflation, which is 1/3rd of the total, and 40% of the “core” measure, badly lags the real data – as in, by a year or more.

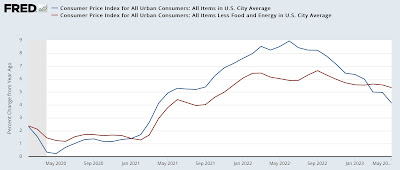

Next, here is the YoY% change in headline inflation (blue), core inflation (red), and inflation ex-shelter (gold)

Both have been in decelerating trends since last June (headline and ex-shelter) or last September (core).

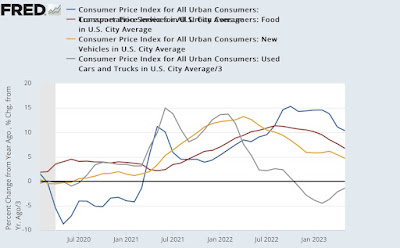

Here are the other big drivers of inflation for the past several years outside of shelter: food (blue), new vehicles (gold), used vehicles (gray), and transportation services (red, /4 for scale!):

All of these are well off their highs, and used vehicles have been negative YoY for a number of months. Aside from food, which is weighted at 13.4% of the total, transportation services are only 5.9%, and new and used vehicles combined only 7.0%.

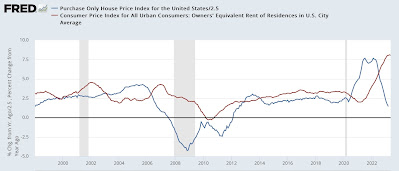

Next, because of the importance of shelter to my analysis, here is an updated long term YoY graph of the big culprit, Owner’s Equivalent Rent (blue), which increased another 0.5% in April, with the FHFA house price index (red, /2.5 for scale), which has been declining since last June and was up 4.0% as of its last reading for February:

Exactly as I have been saying for the past 18 months, house prices dragged OER higher and with it the CPI indexes, with about a 12 month delay. House prices on a YoY basis plateaued for a year between late spring 2021 and mid year 2022, and now OER has finally plateaued as well. The only remaining issue is how long it will remain at that plateau before it follows house prices back down.

Finally, here is “sticky” core inflation ex-shelter:

Even this measure is declining, although less than a “non-sticky” index would be.

As noted above, the FHFA index is only up 3.6% YoY as of March. If it has continued to decline in the 2 months since then at the same rate, it is only up about 2.0% YoY currently, vs. 8.0% for OER. If the FHFA index were substituted for OER, then total YoY CPI for May would only be 2.7%. Core inflation would only be up 3.5%. Neither of these warrants continued restrictive interest rate policy.

In summary, properly measured inflation is no longer a significant issue. Even if OER is a valid way to measure housing inflation, because of the serious lag the Fed should be relying on house prices, and at very least pause.

House prices may have bottomed, YoY price increases (leading inflation) have declined, Angry Bear, New Deal democrat.

Have We Whipped Inflation Now? Angry Bear, Dean Baker, CEPR.