Yves here. The latest offering by Satyajit Das shows, conclusively and depressingly, that there’s no way out of our energy mess save an extreme consumption diet, which is certain not to happen.

By Satyajit Das, a former banker and author of numerous works on derivatives and several general titles: Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006 and 2010), Extreme Money: The Masters of the Universe and the Cult of Risk (2011), A Banquet of Consequences RELOADED (2021) and Fortune’s Fool: Australia’s Choices (2022)

Abundant and cheap power is one of the foundations of modern civilisation and economies. Current changes in energy markets are perhaps the most significant for a long time. It has implications for society in the broadest sense Energy Destinies is a multi-part series examining the role of energy, demand and supply dynamics, the shift to renewables, the transition, its relationship to emissions and possible pathways. Parts 1, 3, 4, 5 and looked at patterns of demand and supply over time, renewable sources, energy storage, economics of renewables, the energy transition and the inter-action between energy policy and emissions. The last two parts outline the energy endgame. This piece -part 7- outlines the framework that will shape events. The final part will look at possible trajectories.

The energy endgame will be shaped by the interaction of several forces – power demand and supply, economics, physics and domestic and international politics.

Energy Demand > Supply

Demand is a function of population and energy needs per capita.

The world’s population, currently around 8 billion, is expected to continue to rise to 8.5 billion in 2030, 9.7 billion in 2050 and 10.4 billion by 2100. Some forecasters argue that due to falling fertility rates it will peak in the middle of the 21st century and decline gradually.

Energy density, a function of living standards and climate, has stabilised and even declined in advanced economies but continues to rise in emerging countries. If the world’s 4 billion people with limited incomes and access to power increase their energy use to merely a third of advanced economies’ per capita level, then global demand will rise by around two times US total consumption or around 30 percent of all global energy needs.

Extreme temperatures which drives consumption for heating and air-conditioning may also affect demand. In India, the consumption from newly installed air conditioners largely offsets power produced from new solar farms.

Most technological developments, designed to improve lifestyles, are energy dependent. Aviation and information technology illustrate this aspect of energy demand.

$1 billion in aircraft produced will consume around $5 billion in aviation fuel over their 20 year lives. As of 2023, Airbus and Boeing’s order books were for over 12,000 commercial aircraft reflecting demand for travel. While some will replace older less-fuel efficient aircraft, the overall growth in numbers will offset lower fuel consumption. The required supply of sustainable aviation fuels, using waste such as cooking oil and plants, which the aviation industry is relying on to reduce emissions, will be difficult to satisfy. A credible path to net zero emissions for aviation is difficult.

Similarly, data centres in which over $100 plus billion is invested each year consumes $7 billion in electricity over a similar time horizon. Data and computation intensive applications, such as artificial intelligence, and virtual or augmented reality such as that of the metaverse, will require significant amounts of energy.

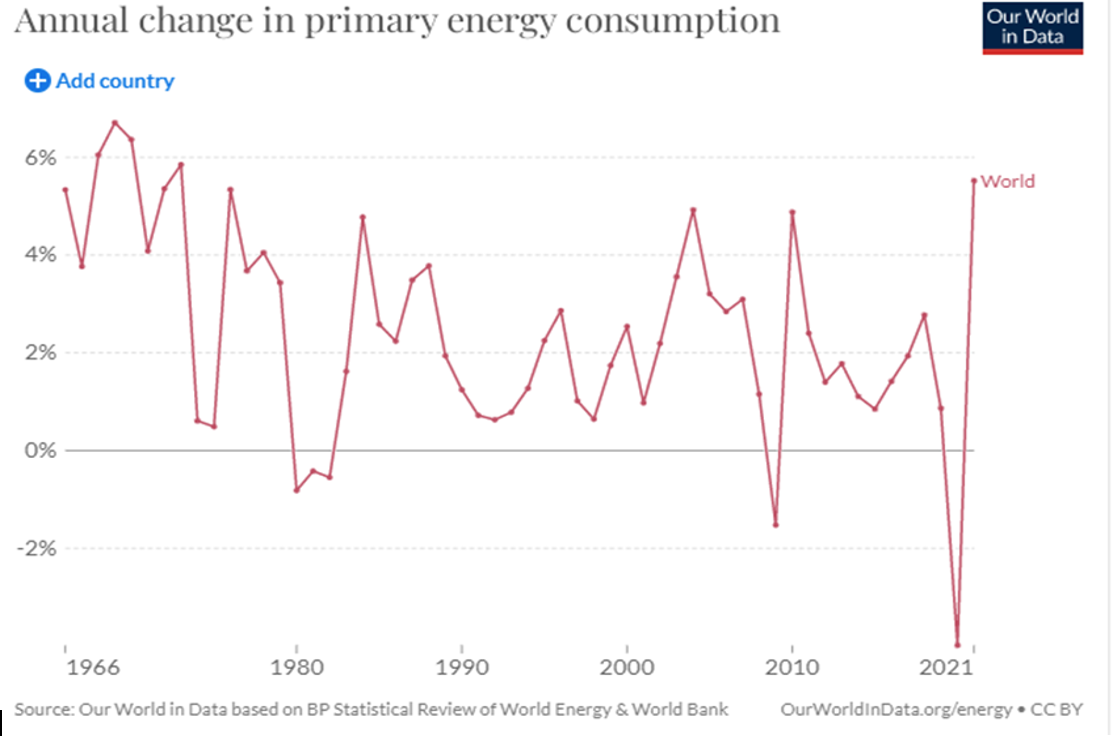

Increases in energy efficiency perversely lead to higher energy usage. Since 1990, global energy efficiency has improved by around 33 percent but energy use increased by 40 percent primarily due to economies growing by 80 percent.

Improved aviation technologies have reduced fuel use by around 70 percent since the mid-1990s but increased travel driven by lower airfares has resulted in global aviation fuel demand rising by over 50 percent. In 1960, the cost of a one-way flight between New York and London was around $300, roughly the same as the lowest fare before the pandemic despite general price levels having risen by around 900 percent over the period. Between 1990 and 2019, the number of passengers traveling by air globally rose from 1 billion to 4.5 billion. An economy-class flight from London to Sydney uses a fifth of the remaining per capita carbon quota available, while in first-class it would deplete 60%. The Swedish concept of flygskam, flight shame, has not yet taken off.

In computing, energy use per byte has decreased by an astonishing 10,000 times over a similar period but global computing demand for electricity has risen sharply due to the proliferation of devices and a 1,000,000+ times increase in data traffic.

This phenomenon is the Jevon’s effect, named after the 19th century English economist William Stanley Jevons, which found that technological progress or government policy that increases the efficiency with which a resource is used and reduces its cost leads to growing demand, increasing, rather than reducing, use. Environmental and energy policymakers today frequently assume the opposite; that is, efficiency gains will lower resource consumption.

Most climate proposals are based on consuming 25 percent less energy, a fact which is frequently ignored.

This is unlikely to be achievable. There has not been a single 20-year period where per capita demand has fallen by more than 0.1 percent since 1965 (the period covered by BP’s statistical dataset). Energy demand has only slowed or declined during major economic downturns, such as the 2008 recession and the 2020 Covid19 pandemic. The 25 percent reduction assumed by the Intergovernmental Panel On Climate Change over the next 30 years would require a major reduction in economic activity and living standards.

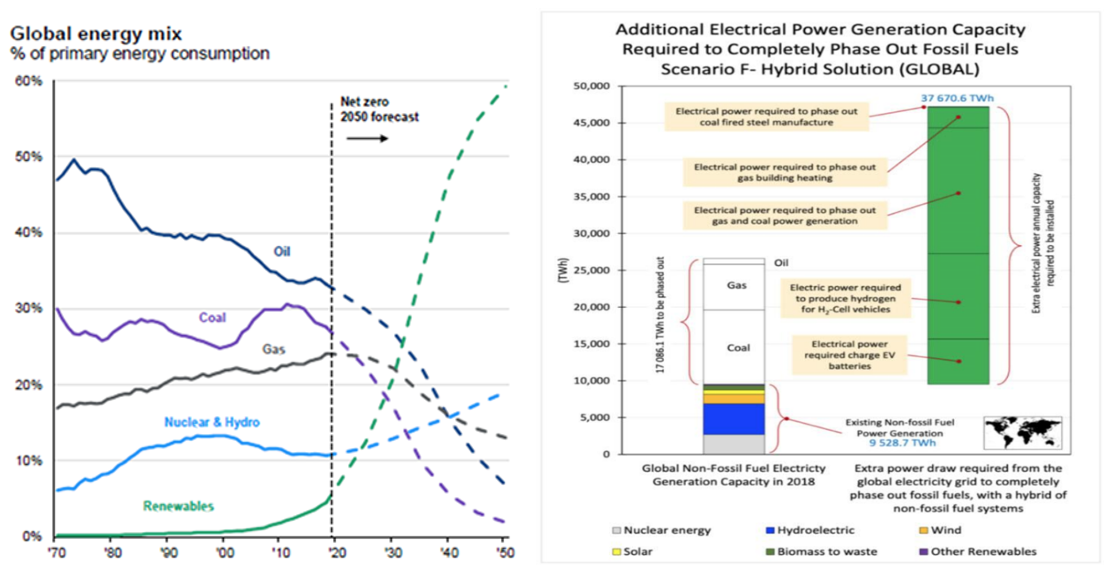

Over the last 150 years, fossil fuels, primarily coal, oil and natural gas, have been the main energy sources, currently supplying about 70-80 percent of the world’s requirement. These resources are finite. In the absence of new discoveries or improved extraction technologies, oil and gas reserves will be exhausted in around 50 years. Coal reserves have longer lives, perhaps 3 times that of hydro-carbons. This ignores the threat to the environment posed by continued use of fossil fuels.

The current focus is on replacing fossil fuels with renewables which currently make up around 20-30 percent of power sources. The proposed shift over-emphasises electrification.

Converting the entire US electricity system to renewables would leave around 70 percent of American hydrocarbon use unaffected. The worldwide replacement of internal combustion engine power cars with of EVs would reduce global oil usage by around 15-20 percent. Heavy transportation, aviation and heavy energy using industries (steel, cement, ammonia) rely on hydro-carbons.

A successful shift to renewables, to replace dwindling supplies of fossil fuels and reduce emissions, would require electrification of many activities and the ability to convert electricity into a fuel such as hydrogen economically and efficiently. Unfortunately, this process is complicated by energy physics.

Energy Physics

For example, in winter, ERCOT, manager of Texas’s power supply, anticipates 6,000 megawatts of its total 31,000 megawatts of installed wind capacity (around 20 percent) will be available. Renewables have lower energy density, surface power density and lack portability.

Converting renewable energy into a true alternative rather than a source of supplemental power will require backup generation or large scale energy storage. Since 2000, US power utilities have added significant fossil fuel powered generating capacity (usually gas turbines) to compensate for uncertain renewable output into the grid to meet consumer requirements for uninterrupted power.

The major storage options are pumped hydro or batteries. Pumped hydro is cheaper but requires large land areas, suitable geography and revamping of the grid and transmission networks. Australia’s Snowy 2.0 scheme is designed to generate an additional 2,000 megawatts of dispatchable, on-demand generating capacity and approximately 350,000 megawatt hours of large-scale storage sufficient to power three million homes for about a week. The project, which uses an existing hydro scheme not a new greenfield site which should have made the project easier and less risky, is over-budget (cost increased from A$2 billion to A$10 billion) and late (from 4 years to 10 years).

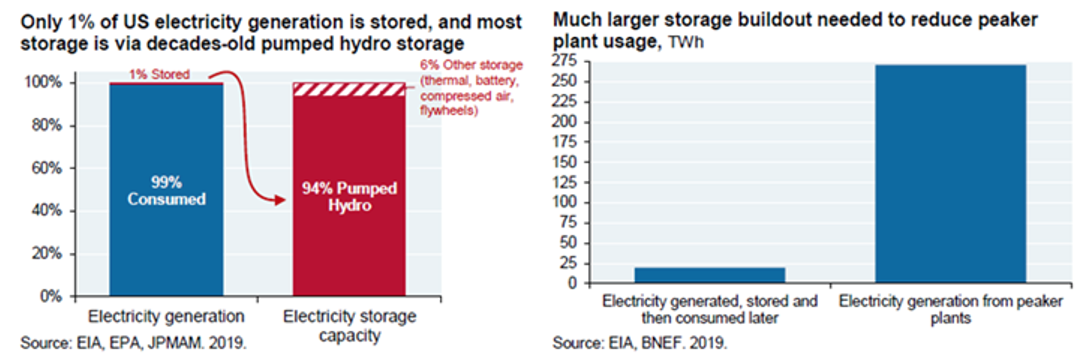

While flexible and portable, current battery technology is unlikely to meet the storage needs of the energy transition. The energy equivalent of around 1 kilogram (2.2 pounds) of hydrocarbons requires approximately 70 kilograms (120 pounds) of the best currently available batteries. One barrel of oil (159 litres or 42 gallons) weighs 136 kilograms (300 pounds) and can be stored in a $20 tank The energy equivalent requires 9,000 kilograms (20,000 pounds) of Lithium batteries costing $200,000. This limits applications like mediumto long-haul flights which would require rechargeable batteries weighing more than a normal twin-aisle long range jet and costing $60 million.

In the US, the current utility scale battery banks augmented by EV batteries can store only a few hours of national electricity demand. Fabricating batteries sufficient for 2 days of storage would require hundreds of years of the total output of the $5 billion Tesla Gigafactory in Nevada, currently the world’s biggest battery manufacturing facility.

The use of hydrogen as a store of renewable energy and fuel requires improvements in technology, production facilities and costs to be viable. It also requires significant amounts of water.

While technology and manufacturing advances will lower costs, batteries cannot meet the energy storage requirements of a totally renewable powered energy system in the foreseeable future without major scientific breakthroughs.

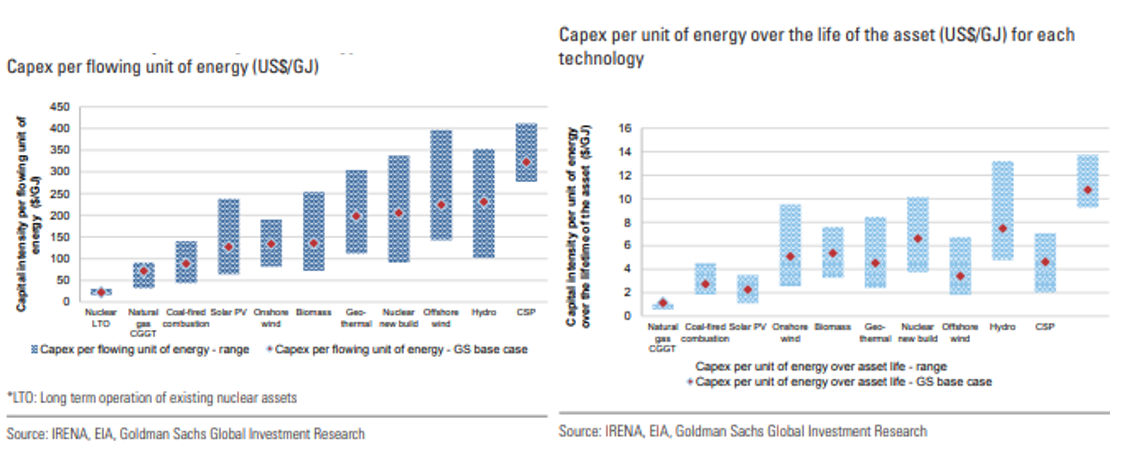

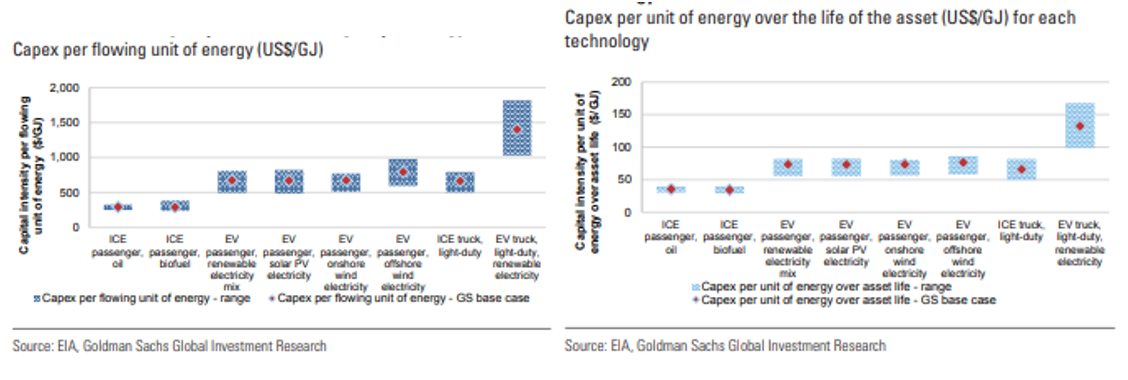

Renewables also have lower energy return on energy invested (EROEI) than fossil fuels and nuclear plants especially where energy storage is factored in. Delivering the same level of final net energy consumption will necessitate more energy and materials lowering efficiency and increasing cost.

Current energy policy is predicated on an unshakeable faith in technology. Increasingly, as pressure mounts, policy makers envisage a Jules Verne like science fiction future where innovation will solve all problems and lower costs to allow the status quo to continue indefinitely.

Policy makers and investors of questionable scientific and general literacy under the influence of the latest snake-oil salesman are enamoured of ‘disruption’. A frequent analogy is the rate of improvement in digital technologies. Moore’s law is cited although most users are unsure whether the reference is to Intel’s Gordon Moore or actress Demi Moore.

Unfortunately, the physics of information and energy are different. In an acerbic commentary, Mark Mills, a physicist, used a telling analogy to highlight the differences. If solar power scaled like semi-conductors, then a single postage-stamp-size solar array would power the Empire State Building and a battery the size of a book, costing three cents, would power trans-continental jet flights. While additional efficiencies are likely, digital-like 10 times gains do not exist for solar or wind energy because of limits to conversion and capture rates. Given that maximum theoretical energy in oil is 1,500 percent greater in weight terms than that in battery chemicals, 10 times gains do not exist for energy storage.

The practical challenges are epitomised by the famous description of “academic reactors” by Admiral Hyman G. Rickover who directed the development of US naval nuclear propulsion and its operations for three decades. The characteristics of an academic reactor are simplicity, small, cheap, light, quickly constructed, flexible, and with minimal development requirements as it uses available generic components. Such technology was, he found, always in the study phase rather than in production. In contrast, a practical reactor, in his experience, had different features: complicated, large, expensive, heavy and required large amounts of developments including on apparently trivial items. It was currently in production but behind schedule and over budget.

In the absence of radical, unexpected changes in energy science which would require re-inventing fundamental principles, renewable technologies will not achieve the efficiencies of fossil fuels. It may be as Star Trek’sMontgomery Scott, Chief Engineer of the original Starship Enterprise, reminded Captain Kirk: “I cannae change the laws of physics, Cap’n!”

Energy Economics

Substitution of energy sources will affect the cost of power to users.

Advocates argue that renewable energy costs are now lower than fossil fuels. The claim, which relies on misleading premises, is disingenuous. If renewables are as effective and low-cost as claimed, there should be no need for government subsidies for broad adoption.

The commonly used levelized cost of electricity (LCOE) is based on lifetime costs for an energy installation divided by energy production but excludes energy storage, back-up supply (usually from fossil fuels), other expenses such as expansion of the energy grid and externalities.

Costs will come under pressure as prices for transition critical materials increases because of supply shortages. In addition, as the best geographic sites for solar and wind are utilised, new facilities will need to be built in less favourable areas. This may lower already modest producing levels (around 35 percent). Competing demands for land will also increase costs as citizen opposition mounts, already evident in the Renewable Rejection Database.

The cost of battery storage remains high due to a combination of rising demand and rising cost of raw materials. For example, EV battery costs could increase by up to 22 percent by 2026.

Forecast investment needs show significant variation. Consulting firm McKinsey suggested a contested total cost of over $275 trillion by 2050, equivalent $9.2 trillion per annum. The UN High-Level Climate Champions, estimated $125 trillion. Most estimates are around $50 trillion. One study argues that not only is a 100 percent renewables energy system possible by 2050 but would be economically benefit the global economy by between $5-15 trillion after incorporating climate and non-climate-related economic benefits. The methodologies used are not strictly comparable. For example, the impact of stranded investment and likely bank loan losses are ignored. Many are clearly manipulated by partisan advocates of a particular position. Irrespective of the exact figure, it will undoubtedly be substantial.

Even at 3-5 percent of global GDP per annum, it is unclear whether that can be funded because of stretched public finances in advanced economies and the lack of resources in developing countries. This is compounded by other claims on public revenues for defence and social welfare programs especially health and aged care for aging populations. Increasing costs of dealing with and adapting to extreme weather events driven ironically, in part, by climate change will make increasing claims on treasuries. Most of the required expenditures remain unfunded. For example, the European Commission estimated its Green deal will cost €620 billion but has allocated €82.5 billion (13 percent) to date.

In general, the energy transition will entail moving to more capital intensive technologies. As the cost of capital normalises from the artificial lows due to the now-reversing regime of low rates, this means that costs will rise.

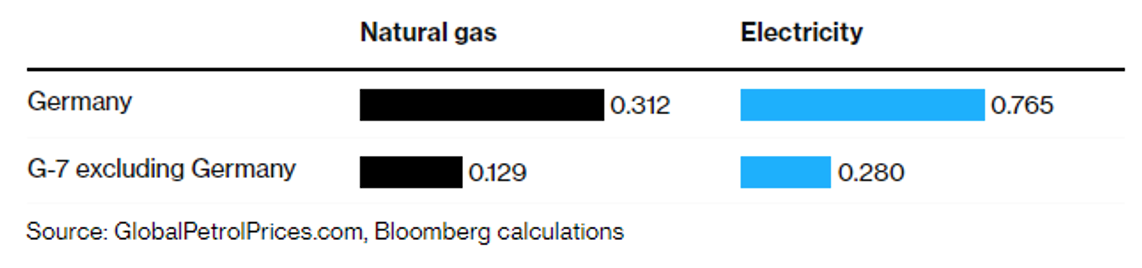

This will translate into higher energy costs for consumers. This will affect inflation levels, disposable income and living standards. The probable effects are evident in economies which have pursued ambitious energy policies. California’s electricity costs are the highest in continental US. German electricity costs are amongst the highest in the world.

Cost relative to per capita income affects the ability to manage higher energy costs. Germans and Americans with GDP per capita of around $51,000 and $70,000 respectively may be able to absorb high electricity costs although lower income segments of the population will be disadvantaged. Emerging nations will find it difficult; for example China and India’s GDP per capita are $12,000 and $2,250 respectively.

The issue of affordability can be seen in demand for EVs. 85 percent of Americans cannot currently afford EVs because they are more expensive than traditional automobiles. This creates a perverse redistribution of wealth with subsidies benefitting high income households who can afford to buy EVs at the expense of low income taxpayers.

The scale of the task is monumental. In order to replace fossil fuels, renewable energy would have to expand 90-fold in 20-30 years. Ancillary work such as reconfiguring the American hydrocarbon-based electric generation system alone over a similar period would require a construction rate 14-fold greater than any time in history. The scale for building appropriate energy storage for the transition to renewables is similar.

This assumes availability of raw materials, manufacturing facilities, skilled staff, regulatory support and an acquiescent population. Those conditions may prove more difficult to satisfy in practice than theory.

Emissions Abatement

The higher costs and lower living standards may be acceptable if the shift to renewables reduced emissions. It is far from clear whether the current energy policies will achieve this objective, rightly regarded as an existential concern.

The required reduction in emissions is very large. In fact, it would be necessary to go to zero emissions immediately supplemented by actual carbon removal from the atmosphere (negative emissions) to meet temperature targets. Current agreements, even in the highly dubious case of these being met, are inadequate.

The shift away from fossil fuels is likely to be slow, at best, because of growing energy demand from increasing populations and living standards. It is also uncertain whether the supply of raw materials for the transition will be available. Annual demand for copper, central to electrification, is projected to reach a level by 2050 equal to all production consumed in the world between 1900 and 2021.

In addition, renewable energy sources have lower emissions than fossil fuels but have significantly higher material intensity. The proposed electrification, renewable and battery-centric energy transition will require a vast amount of scarce resources such as lithium, copper, nickel, graphite, rare earths, cobalt as well as water. Significant amounts of energy, primarily derived from fossil fuels, will be needed to explore and develop resources, extract and produce the necessary materials and transport it for use.

Many of these mines and plants producing raw materials for the energy transition are in developing countries. China dominates processing of some transition critical minerals. The energy mix in these countries are weighted towards coal, oil and gas and may be a significant source of additional emissions. China, which currently produces around 70-80 percent of all batteries used globally, relies on fossil fuels for 70 percent of its power meaning that EVs using Chinese batteries will increase rather than decrease carbon dioxide emissions. Net emissions may fall less than forecast or not all.

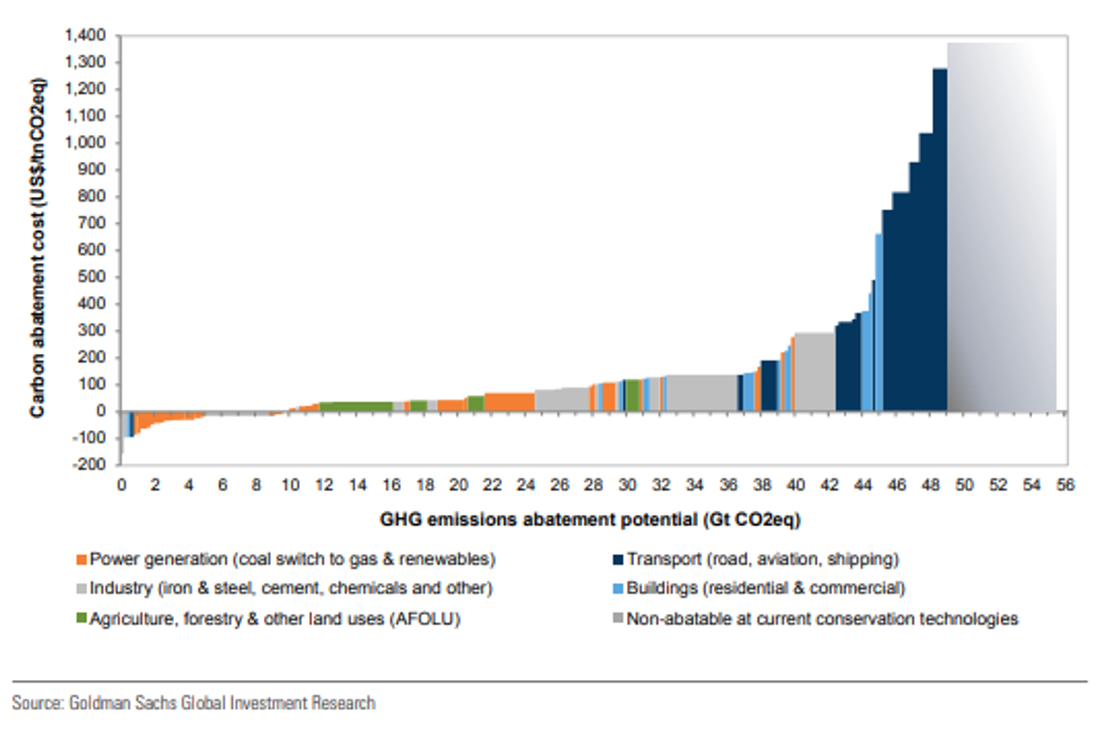

The cost of abatement also rises as more difficult to decarbonise processes are addressed.

The high cost will adversely affect energy economics leading to pressure to retrench emission reduction initiatives.

A fundamental concern is the difficulty of global co-operation to tackle climate issues. The effects of actions of individual countries and states is highly variable. Developed country incremental emission are in structural decline in part because high emission activities and industries have been re-located to emerging economies, such as China and India which are rolling out significant new fossil fuel power generators. Grand standing policies amongst well-meaning but naïve policy makers and citizens in advanced countries are unlikely to have the effect on emissions often proclaimed. US Climate Czar John Kerry reluctantly admitted that the US going to net zero emission may have no discernible impact of rising temperatures unless other high emission nations follow suit.

It is highly unlikely that developing nations will abandon fossil fuels due to significant ongoing energy needs. Even wealthier Germany and California, which have claims to being greener than most, have significant reliance on fossil fuels despite clear policies, extensive subsidies, high quality engineering expertise and low incremental demand due to slower population growth.

Limiting temperature rises requires, for example, a large fall in global coal production, by more than two-thirds by 2030 and a progressive complete phase out. In fact, coal use rose to record levels in 2022. Some European countries, like Germany, affected by the loss of Russian gas supplies, reverted to coal fired power plants. China increased its use of coal-fired power plants during the first half of 2023 due to reductions of hydroelectric generation in the southern provinces as a result of drought. Coal use may fall by less than a fifth by 2030 – even this may be difficult to achieve as emerging countries have plans for a significant number of coal-fired power plants. 80 percent of coal reserves must remain unused if climate change targets are to be met placing a significant burden on countries and peoples where these resources are located.

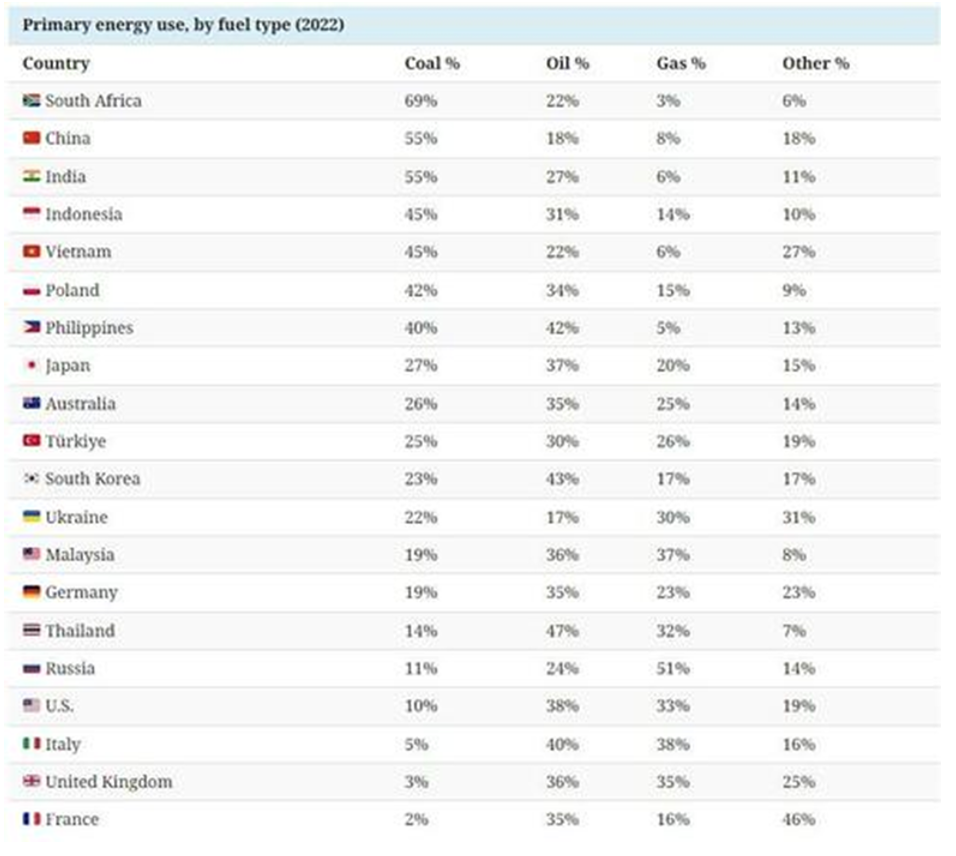

The table below illustrates how coal continues to be as an important source of energy, particularly in emerging economies where demand is expanding rapidly.

The lack of global co-ordination is evident in simple things like the lack of standards. The $13 billion plus US government supported investment in EV charging infrastructure is bedevilled by the exact voltage requirements and the length of cable need to reach individual EV’s charging port – Nissan Leaf’s in the front, Hyundai Ioniq 5’s. Volvo’s the back left.

Political Influences

Societal and political factors will influence the future of energy.

The social contract between politicians and populations implicitly relies upon uninterrupted, unlimited and cheap power that underpins living standards. In richer countries, availability of energy for climate regulation (air conditioning and heating), personal mobility (private cars), travel and data usage, is taken for granted. Even gas cooking and coal or wood fired pizza ovens are seemingly sacrosanct. The consequences of any impingement on these ‘freedoms’ or ‘choices’ is unknown. In poorer countries, the population aspires to energy intensive Western lifestyles as part of the promise of development. It would be risky politically to seek to alter these expectations. At a minimum, changes in energy availability and affordability will lead to a sharp fragmentation of domestic politics.

Geo-politics throughout history has revolved, in part, around access to vital resources. Since the late 19th century, access to hydro-carbons has been seen as an important aspect of foreign policy and economic power. Britain’s power relied on access to coal. America’s rise was underpinned by access to oil. Wars have been fought over access to energy, including being a factor in Adolph Hitler’s Third Reich’s and Japan’s actions which led to World War 2.

The transformation of the energy complex will fundamentally alter existing relationships.

Existing hydro-carbon and coal exporters, such as Saudi Arabia, the Gulf countries, Russia, Australia and the US, face interesting choices. Decarbonisation pressures may be perceived to lower the value of their resources. This may encourage over-production in the short run to maximise revenues and, in part, to suppress prices to change cost relativities between fossil fuels and renewables. Revenues may be directed, as in Saudi Arabia, to change the industrial structure to one less reliant on fossil fuel revenues.

But given the likelihood that the energy transition and attempts to reduce emissions will not proceed as planned, the transformation may be more complex.

In the initial phase, the hydro-carbon producers may struggle for influence and power. Producers of transition critical materials will gain in importance during this period. This reflects the concentration of the supply of relevant minerals in a few countries; for example, the Democratic Republic of the Congo (cobalt); Australia (lithium, cobalt, and nickel) and Chile (for copper and lithium). Other nations rich in the relevant minerals include Peru, Russia, Indonesia and South Africa. In this part of the cycle, these countries gain in economic and political terms as commodity revenues surge. They move to the centre of geo-political alliances with larger powers needing access to critical raw materials.

Low-cost hydro-carbon producers experience flat to declining revenues. Saudi Arabia, Iran, Iraq and Russia may expand their market share due to their lower cost of production from 45 percent currently to 57 percent in 2040. Higher cost and smaller producers like the US. Canada, smaller Gulf states, north Africa, sub-Saharan Africa, Europe (Britain, Norway) are at a disadvantage. Some like America, Brazil, Canada and Australia increase production of other minerals to offset part of their lost fossil-fuel earnings.

At a certain point, the cycle may shift back. As problems around the energy transition become obvious, the need to secure access to dwindling hydro-carbon supplies for activities which cannot be electrified efficiently lead to a resurgence of producers. The resulting shift in alliances and relationship requires a balance between suppliers of oil and gas and transition critical minerals.

Increasing resource nationalism will affect availability and the prices of energy as well as transition critical materials. States may nationalise vital resources, such as those under consideration for lithium in Latin America. Other measures include export bans in total or actions like Indonesia’s restriction on overseas sales of raw nickel (planned to be extended to other minerals) to force investment in onshore refining to increase local revenues. Other alternatives are high taxes and royalties. The objective is to increase individual state’s revenues as well as control of critical resources. The position will be complicated by growing trade wars, sanctions and intellectual property rights which will make sharing technologies more difficult.

In effect, global industrial supply chains and power structures will become more volatile in the decades ahead being tied increasingly to the need to secure access to energy and related critical raw materials.

Policymakers will recognise former Russian Prime Minister Viktor Chernomyrdim’s lament: “we wanted the best but it turned out like always”. They may need to follow another of his sage observations: “there is still time to save the face…later we will be forced to save some other parts of a body”.

© 2023 Satyajit Das All Rights Reserved

A version of this piece was published in the New Indian Express.