Signature Bank shares have now lost nearly half their value in 2022 as its exposure to free-falling cryptocurrencies continues to weigh on the S&P 500 component.

Signature Bank SBNY joined the S&P 500 in December and has fallen as much as 48% this year through Thursday, compared with a 23.1% drop by the S&P 500 index SPX and an 18.4% decline in the SPDR S&P Regional Banking exchange-traded fund KRE.

The bank’s shares had soared to a record close of $366.00 on Jan. 12, but closed Thursday at $167.55, the lowest close since Feb. 1, 2021. They have fallen 15.3% this week, on track for the biggest weekly drop since April 2020, and have dropped 45.3% while losing ground in 11 of the past 13 weeks.

While the bank has held about $29 billion in deposits for cryptocurrencies, the shares appear to have been oversold, analysts have said in recent weeks. But the stock has continued to weaken amid sharp losses in bitcoin BTCUSD and other cryptocurrencies. Bitcoin has plummeted 56% this year, as of morning trading Friday.

Also Read: Bitcoin crash: These three metrics show how bad the carnage is, and what to expect next

Jefferies analyst Casey Haire said last month that Signature Bank’s (SBNY) 2023 earnings would still come in at $20 a share even when stripping out its entire crypto deposits business. The profit figure would still convert to a price-to-earnings ratio of 9.5, Haire said, which is in line with the SPDR’s regional banking ETF (KRE).

The FactSet consensus for 2023 earnings per share was $26.70.

“Given our belief that SBNY’s crypto deposit franchise will survive, we view the stock as oversold at these levels,” Haire said at the time.

When Haire penned his research note on May 13, Signature Bank’s stock closed at $201.20.

The stock was up 1.9% in morning trading on Friday, but has dropped 15.1% since May 13, while the regional banking ETF has slipped 4.6%.

FactSet, MarketWatch

Despite the rocky reception to Signature Bank in the stock market, analysts have only slightly reduced second-quarter earnings estimates, according to FactSet data.

At last check, Wall Street expected Signature Bank to earn $5.09 a share in the second quarter, down from $5.10 a share as of May 31 and $5.13 a share as of April 29, according to FactSet.

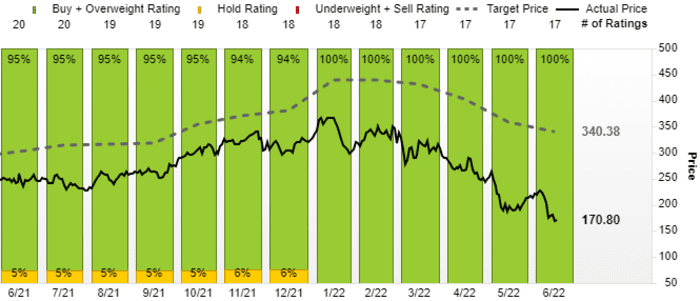

And all 17 analysts surveyed by FactSet have the equivalent of buy ratings on the stock, with the average price target of $340.38 implying a near doubling in price.

FactSet

The company’s mid-quarter update as of May 13 revealed core loan growth of $1.7 billion, and a drop of $1.4 billion in deposit balances, related to volatility in crypto space.

Sifting through those numbers, Janney analyst Jake Civiello on May 16 reiterated a buy rating and issued a $325 a share fair value estimate.

“We have long-believed that SBNY has been a conduit for non-bank investors to get exposure to digital assets via a highly regulated financial institution,” Civiello said. “We reiterate that SBNY exposure is almost entirely deposit-based, not loan-oriented. That said, recent stock price volatility serves as a reminder that the pendulum swings both ways with respect to momentum investors.”

Also Read: Crypto lender BlockFi sees ‘increased institutional demand,’ CEO says, as competitor Celsius pauses withdrawals