After becoming the target of multiple state attorney general lawsuits and investigations, nationwide class action lawsuits, a Department of Justice criminal probe, and the likely target of a recent FBI raid in Atlanta, RealPage – a private equity-owned corporation that creates software programs for property management – is finally responding to allegations it orchestrated a national rent price-fixing cartel that has sent rent prices through the roof.

Texas-based RealPage is accused of acting as an information-sharing middleman for real estate rental giants. The lawsuits against it and large property managers [1] contend that the latter agreed to set prices through RealPage’s software, which also allowed the companies to share data on vacancy rates and prices in many of the US’ most expensive markets.

Many of the rental markets dominated by large landlords have seen astronomical growth in rental prices in recent years (even before the pandemic), as well as a rising number of evictions and spikes in homelessness. The lawsuits against RealPage and the rental management companies contend that its software covers at least 16 million units across the US, and private equity-owned property management companies are the most enthusiastic adopters of the RealPage technology. A separate lawsuit filed last year targets Yardi Systems and property management companies [2] using its price-setting software to collude on at least another eight million units.

It’s worth reproducing the RealPage’s June 18 statement in full to then dissect it:

Starting in October 2022, false and misleading claims about RealPage and its revenue management software have been reported to the media and in legal filings. These factual inaccuracies threaten to undermine the essential benefits RealPage’s solutions provide to both renters and housing providers. In fact, RealPage’s revenue management software contributes to a healthier and more efficient rental housing ecosystem.

“The time is now to address a number of false claims about RealPage’s revenue management software, and how rental housing providers operate when setting rent prices,” said Dana Jones, RealPage CEO and President. “Housing affordability should be the real focus. RealPage is proud of the role our customers play in providing safe and affordable housing to millions of people. Despite the noise, we will continue to innovate with confidence and make sure our solutions continue to benefit residents and housing providers, alike.”

Housing affordability is the real problem

Housing affordability, including the lack of affordable rental housing, is a critically important national problem created by a host of complex economic and political forces, including:

- persistent undersupply of rental housing units,

- increasing demand for rental housing in many areas of the country,

- inflationary pressures that affect costs to build, insure and manage housing properties,

- inefficient or unnecessarily onerous permit and zoning requirements,

- higher mortgage rates and home prices driving more people to rent rather than own their own homes, and

- changes in where and how people choose to live.

Setting the record straight

Here are the facts about RealPage’s revenue management software solutions:

- RealPage revenue management software benefits both housing providers and residents.

- RealPage customers:

- decide their own rent prices,

- always have 100% discretion to accept or reject software price recommendations,

- are never punished for declining recommendations, and

- accept recommendations at widely varying rates that are far lower than has been falsely alleged.

- RealPage revenue management software makes price recommendations in all directions – up, down, or no change – to align with property-specific objectives of the housing providers using the software.

- RealPage revenue management software never recommends that a customer withhold vacant units from the market. In fact, properties using our revenue management products consistently achieve vacancy rates below the national average.

- RealPage uses data responsibly, including limited aggregated and anonymized nonpublic data where accuracy aids pro-competitive uses.

- RealPage revenue management software serves a much smaller portion of the rental market than has been falsely alleged.

RealPage revenue management software offers prospective residents and housing providers more options and flexibility in lease terms, aids compliance with Fair Housing laws, does not use any personal or demographic data to generate rent price recommendations, and helps ensure that prospective residents have access to the best pricing available to everyone.

But statements provided by users of the RealPage software and even RealPage executives’ past statements indicate that the company is now likely lying in at least the following ways:

On Affordability

While issues that RealPage mentions like undersupply and increasing demand in certain areas no doubt play a role, RealPage officials have also bragged about the outsized effect their software has on rental market prices. Company executive Andrew Bowen once said that the software was “driving it,” referring to rental price increases. He added: “As a property manager, very few of us would be willing to actually raise rents double digits within a single month by doing it manually.”

On Undersupply and Vacancy Rates

Again, the lawsuits against RealPage and statements by the company’s founder indicate that RealPage played a role in undersupply by advising property companies to leave units vacant in order to create an artificial scarcity of rentals. This anti-competitive behavior is made possible because property managers know that their “competitors” are also using RealPage’s system and will not undercut them.Here’s what one of the lawsuits alleges:

“RealPage allows participating Lessors to coordinate supply levels to avoid price competition. In a competitive market, there are periods where supply exceeds demand, and that in turn puts downward pressure on market prices as firms compete to attract lessees. To avoid the consequences of lawful competition, RealPage provides Lessors with information sufficient to “stagger” lease renewals to avoid oversupply. Lessors thus held vacant rental units unoccupied for periods of time (rejecting the historical adage to keep the “heads in the beds”) to ensure that, collectively, there is not one period in which the market faces an oversupply of residential real estate properties for lease, keeping prices higher.”

And here’s former RealPage CEO Steve Winn:

‘During an earnings call in 2017, Winn said one large property company, which managed more than 40,000 units, learned it could make more profit by operating at a lower occupancy level that “would have made management uncomfortable before,” he said.

The company had been seeking occupancy levels of 97% or 98% in markets where it was a leader, Winn said. But when it began using YieldStar, managers saw that raising rents and leaving some apartments vacant made more money.’

It’s worth noting the correlation between the increase of homelessness and RealPage really taking off following its 2016 acquisition of its main rival. A 2022 study from The Guardian and the University of Washington found that across 73 US cities and counties there were at least 18,000 deaths of people experiencing homelessness over the 2016 to 2020 time period with the number increasing 77 percent over that five-year period. (The federal government makes no effort to count the number of homeless deaths, and many believe the number to be much higher.) [3]

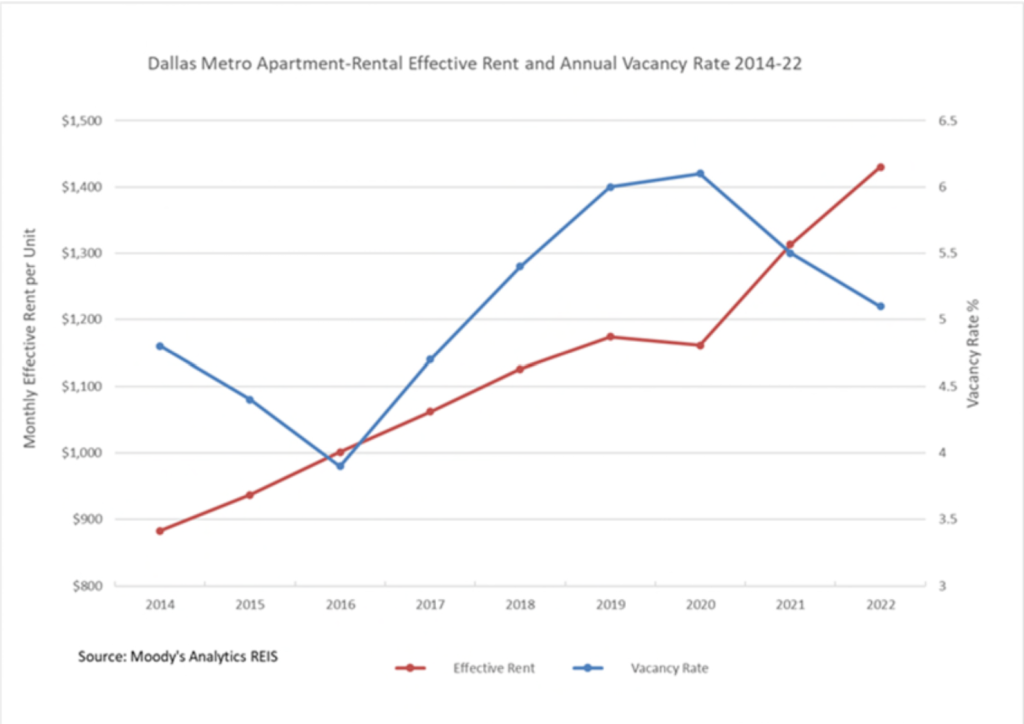

The lawsuits against RealPage document how in many metropolitan areas increase rents every year, whether vacancies were rising or falling, and in most instances, both rents and vacancy rates trended higher from 2014-2020, across various metropolitan regions where RealPage operates. For example in Nashville and Dallas:

On “Inflationary Pressures”

Over the past ten years, rent inflation has outpaced overall inflation by 40.7 percent. A witness in one of the lawsuits says the price increases have little to do with inflation but with collusion:

Another early developer of RealPage’s pricing software (“Witness 9”)44 reflected on how RealPage’s facilitation of collusion among property management companies and owners has pushed rents higher at a breakneck pace: “[T]hese optimization systems are really efficient at extracting value and they will push things until they start to break.”

And RealPage’s role might extend beyond just the millions of apartments priced using its software. Maureen Tkacik argues the following:

RealPage not only raised the rent, but it baked eternal rent hyperinflation into the forecasting math of multifamily housing, fueling a dramatic plunge in underwriting standards (and attendant rise in valuations) that lined the pockets of every manner of real estate speculator in 2021 and 2022. This maneuver led to extreme blowback when interest rates—and the floating-rate interest payments owed on the thousands of apartment buildings that changed hands during those years—began to balloon. Perhaps even more insidiously, when mortgage payments rose in 2022 and landlords should have, by conventional market logic, been jumping to fill empty apartments, RealPage instead gave them the tools to extract ever-higher revenues out of powerless renters, no matter how trash-strewn, roach-infested, or crime-ridden their homes had become.

On RealPage’s Price “Recommendations”

They would appear to be more than just mere recommendations. From one of the lawsuits:

Beginning in approximately 2016, and potentially earlier, Lessors replaced their independent pricing and supply decisions with collusion. Lessors agreed to use a common third party that collected real-time pricing and supply levels, and then used that data to make unit-specific pricing and supply recommendations. Lessors also agreed to follow these recommendations, on the expectation that competing Lessors would do the same.

Here’s an Associate Vice President of one of the defendants talking up the collusionary aspect of the software, which was featured in RealPage’s own literature:

With LRO [RealPage’s Lease-Rent Options] we rarely make any overrides to the [pricing] recommendations . . . [W]e are all technically competitors, LRO helps us to work together . . . to make us all more successful in our pricing . . . LRO is designed to work with a community in pricing strategies, not work separately.”

The lawsuits also allege that there was considerable pressure to follow the “recommendations”:

To ensure that the landlords abide by these “recommendations,” RealPage puts significant “pressure” on them “to implement RealPage’s prices,” including by requiring clients to submit requests to deviate to the “corporate office” and tracking the “identity of the client’s staff that requested a deviation.” Multifamily Compl. ¶¶ 17-20, 261-86. As a result, landlords using RealPage adopt RealPage’s recommendations 80-90% of the time.

Furthermore, according to a joint legal brief from the DOJ and FTC, even without the additional pressure, these types of recommendations via algorithm are still illegal:

It is per se illegal for competing landlords to jointly delegate key aspects of their pricing to a common algorithm, even if the landlords retain some authority to deviate from the algorithm’s recommendations. Although full adherence to a price-fixing scheme may render it more effective, the effectiveness of the scheme is not a requirement for per se illegality.

FBI Raid in Atlanta

RealPage’s statement comes four weeks after the FBI raided the Atlanta headquarters of Cortland Management on Wednesday, May 22 as part of the federal investigation into RealPage and the real estate management companies that use its software.

Why Atlanta and why Cortland? Well, for one, it owns nearly 85,000 apartment units (as of June 2022), and uses RealPage’s software. Atlanta also might provide some of the clearest evidence of RealPage’s devastating effects on renters. According to Bis Now:

…software-driven pricing affects 81% of [Atlanta] multifamily rental units. Since 2016, rents in the city have surged by 80%, despite rising vacancy rates that would typically result in lower rents.

The city is also a hotspot for Wall Street-owned single-family homes. According to a May report by the U.S. Government Accountability Office that looked at investor-owned single-family rental properties in 20 major US cities, Atlanta came out on top with 25 percent or about 72,000 properties.

And a recent report from Georgia State University, “Horizontal Holdings: Untangling the Networks of Corporate Landlords” published in the Annals of the American Association of Geographers, found that more than 19,000 were owned by just three companies — Invitation Homes, Pretium Partners and Amherst Holdings. The latter two are backed by private equity.

“These companies own tens of thousands of properties in a relatively select set of neighborhoods, which allows them to exercise really significant market power over tenants and renters because they have such a large concentration of holdings in those neighborhoods,” said Taylor Shelton, an assistant professor in the Department of Geosciences at Georgia State.

Atlanta Is Representative of Wider Trend Across the Country

As investors continue to snatch up properties, a trend that really took off during Obama’s foreclosure regime, they are also the driver behind the spread of RealPage’s price-setting software. From ProPublica:

RealPage’s influence was burgeoning. [In 2017], the firm’s target market—multifamily buildings with five or more units—made up about 19 million of the nation’s 45 million rental units. A growing share of those buildings were owned by firms backed by Wall Street investors, who were among the most eager adopters of pricing software.

…Somewhere around 2016, according to one trade group, the industry’s use of the pricing software began to achieve “critical mass.”

And it’s only gotten worse since. Corporate investors have continued to snatch up even more properties since the outbreak of the COVID-19 pandemic, in part because many smaller landlords were hit hard by non-payment from tenants who were protected by eviction moratoria.

Atlanta has the largest market for this kind of corporate landlord activity in the country, according to another study by Shelton. “You have to add up the next two or three largest markets in the U.S. together to have the same amount of corporate landlord investment that Atlanta has,” Shelton said.

And the big landlords are now making off like bandits. From a recent Common Dreams write up on the Accountable.US report on corporate landlord behemoths:

…more than 100 million people who rent their homes in the U.S. are not seeing the benefits of what one Biden spokesperson called “the great American comeback” in their housing costs, particularly millions of people whose homes are owned by corporate landlords.

The government watchdog found that the six largest corporate landlord companies brought in close to a combined $300 million in increased profits in the first quarter of 2024, with the profits mostly stemming from rent hikes.

Overall in the U.S., rent prices have skyrocketed by 31.4% since 2019 while wages have increased by just 23%, meaning tenants need to earn nearly $80,000 per year to keep from being rent-burdened and spending 30% or more of their income on rent.

The six companies included in the Accountable.US analysis on Wednesday have more than rent increases in common: They have all faced lawsuits regarding their use of the property management software company RealPage, which is alleged to have used an algorithm to fix rent prices, impacting about 16 million rental units in the United States.

The largest net income increase Accountable.US found among the six corporate landlords was that of Camden Property Trust, which increased its net income by 97% in the first quarter of this year to $85.8 million. The company spent $50 million on stock buybacks that it said were made possible by its “weighted average monthly rental rate,” which went up nearly 2% year over year.

Their profits are no doubt aided by RealPage, which along with the rental management companies has bragged about how they can increase rents regardless of market conditions, including downturns or recessions.

A Common Thread

While ProPublica reports that Wall Street-owned real estate management companies have been some of the most eager adopters of RealPage software, RealPage itself is also owned by the private equity firm Thoma Bravo.

As the scrutiny of RealPage intensifies, it has not dissuaded public pension funds from investing in Thoma Bravo, which acquired RealPage in 2021, according to the Private Equity Stakeholder Project:

Despite the lawsuits against RealPage, more than 30 US public employee pension funds have invested a total of almost $4 billion in Bravo’s Fund XIV, the fund that acquired RealPage. These pension funds include the California Public Employees Retirement System, New York State Common Retirement Fund, and the Washington State Investment Board. The University of Texas Investment Management Company (UTIMCO) has been a large investor in Thoma Bravo, making six separate commitments into the company totaling $425 million. These commitments included a $125 million commitment to Bravo’s Fund XIV, (the fund which acquired RealPage in 2021). The University of Texas at Austin is also collaborating with Steve Winn, the founder of RealPage, to develop $200 million sustainable research facilities. Winn claims that Texas has “a fragile ecosystem that we need to protect,” and states that preserving the “land and the water for future generations of Texans is important.” However, The Real Deal notes that the facilities would be adjacent to Winn’s Mirasol Springs, a 1,400 acre development that has been the subject of concerns about ecological harm. The collaboration appears to be an opportunity for some positive press for the billionaire.

While Senators Bernie Sanders, Elizabeth Warren, Ed Markey, and Tina Smith, took an interest in the RealPage cartel and urged the DOJ to investigate last year, the Biden Administration has taken little public interest in the issue. A brief mention in the most recent State of the Union address was about all.

Much of the legal architecture that muddied the waters of price-fixing prosecution was established by the Clinton Administration and later sanctioned by Obama. “Information sharing” largely wasn’t prosecuted due to a Clinton-era loophole introduced by HRC in 1993 that allowed it in the healthcare industry (purportedly to help lower prices, although the opposite of course happened), but importantly, the rules were interpreted to apply to all industries. Those rules were further liberated in 1996 and then again in 2011 under Obama’s Affordable Care Act and its Accountable Care Organizations provision.

The current DOJ announced the end of that no-enforcement arrangement last year, however, when it closed those Clinton-era information-sharing loopholes. Principal Deputy Attorney General Doha Mekki explained the rationale behind the decision, saying that the development of technological tools such as data aggregation, machine learning, and pricing algorithms have increased the competitive value of historic information. In other words, it’s now (and has been for a number of years) way too easy for companies to use these so-called “safety zones” to fix wages and prices. Here’s Mekki at an antitrust conference in Miami:

An overly formalistic approach to information exchange risks permitting – or even endorsing – frameworks that may lead to higher prices, suppressed wages, or stifled innovation. A softening of competition through tacit coordination, facilitated by information sharing, distorts free market competition in the process.

Notwithstanding the serious risks that are associated with unlawful information exchanges, some of the Division’s older guidance documents set out so-called “safety zones” for information exchanges – i.e. circumstances under which the Division would exercise its prosecutorial discretion not to challenge companies that exchanged competitively-sensitive information. The safety zones were written at a time when information was shared in manila envelopes and through fax machines. Today, data is shared, analyzed, and used in ways that would be unrecognizable decades ago. We must account for these changes as we consider how best to enforce the antitrust laws.

The FTC also recently came out with a set of general guidance around algorithmic price setting. It’s titled “Price fixing by algorithm is still price fixing.”

Is the crackdown on RealPage the result of this new enforcement policy or did the company push too far even under the previous rules? It would appear to be a little bit of both. From ArentFox Schiff LLP, a national law and lobbying firm, on the shift at the DOJ:

The withdrawal of the policy statements forecasts greater DOJ scrutiny of information sharing; however, it is still clear that not all information sharing is illegal. Both the Supreme Court and the DOJ have recognized that, in many instances, competitors need to share information to achieve legitimate pro-competitive goals. However, exchanges of information could violate the Sherman Act, which prohibits a “contract, combination…or conspiracy” that unreasonably restrains trade, if they allow competing sellers to collude or tacitly coordinate in an anti-competitive manner, such as by coordinating prices. Generally, courts will balance these two competing concerns. The Supreme Court has protected information exchanges where the data was publicly available, was historic rather than current or forward-looking, and/or was aggregated to make the information anonymous. It has also emphasized that certain exchanges of current price information and information exchanges in concentrated markets may receive greater scrutiny.

Either way, a wide amount of latitude seems to rest with the DOJ and FTC. So while this is good news for now, there would appear to be little to prevent future DOJs and FTCs from issuing guidance that says the information-sharing safe zones are open for business again and the next FTC from declaring that “price fixing by algorithm is no longer price fixing.”

Notes

[1] Here are some details I could track down of the real estate goliaths named in the lawsuits who were using RealPage software to allegedly collude and keep rents artificially high:

- Greystar: The nation’s largest property management firm with nearly 794,000 multifamily units, including roughly 100,000 student beds under management.

- Trammell Crow Company, headquartered in Dallas, is a subsidiary of CBRE Group, the world’s largest commercial real estate services and investment firm.

- Lincoln Property Co. Manages or leases over 403 million square feet across the US.

- FPI Management. Currently manages just over 155,000 units in 18 states.

- Avenue5 manages $22 billion in multifamily and single-family assets nationwide.

- Equity Residential, the 5th largest owner of apartments in the United States, primarily in Southern California, San Francisco, Washington, D.C., New York City, Boston, Seattle, Denver, Atlanta, Dallas/Ft. Worth, and Austin.

- Mid-America Apartment Communities, which as of June 30, 2022, owns or has ownership interest in 101,229 homes in 16 states throughout the Southeast, Southwest, and Mid-Atlantic regions.

- Essex Property Trust (62,000 units). This fully integrated real estate investment trust (REIT) acquires, develops, redevelops, and manages multifamily apartment communities located in supply-constrained markets on the west coast.

- Thrive Community Management (18,700 units in Washington and Oregon).

- AvalonBay Communities, Inc. As of September 30, 2022, the Company owned or held a direct or indirect ownership interest in 293 apartment communities containing 88,405 apartment homes in 12 states and DC.

- Cushman & Wakefield, with a portfolio of 172,000 units.

- Security Properties portfolio reflects interests in 113 assets encompassing nearly 22,354 multifamily housing units.

- Cardinal Group Holdings, LLC. 89,000 units managed with more than 100,000 beds and a heavy presence in student housing.

- CA Ventures Global Services LLC. Manages more than 60,000 beds in 69 university markets.

- DP Preiss Co. Specializes in student housing and has more than 30,000 beds in 12 states.

Consumer complaints against above landlords operating in Arizona can be filed here with the Arizona Attorney General case.

More information on the federal class action suit against RealPage is available here, along with an investigation request form if you rented through one of the above companies.

[2] Included in the lawsuit against Yardi are the following property management companies (I’ve tried to track down just how many rental units these companies control, listed here):

- Alco Management Inc. Based in Memphis, Tenn. Manages more than 6,000 apartment homes in 9 states.

- Bridge Property Management. Manages more than 50,000 multifamily units across the country. Headquartered in Salt Lake City with affiliated offices in New York, San Francisco, and Orlando.

- Calibrate Property Management. “Based in Seattle, Washington, Calibrate is expanding its market reach. Now managing properties in Washington, Illinois, Arizona and Minnesota, Calibrate Property Management oversees approximately 1900 units and is rapidly growing.”

- Clear Property Management. Manages apartment communities across Texas. Total number unclear.

- Creekwood Property Corp. (Tonti Properties). Headquartered in Dallas and manages properties across Arizona, Colorado, Florida, Louisiana, North Carolina, and Texas. Total number unclear.

- Dalton Management. Manages more than 1,500 apartment units across California, Oregon, and Washington.

- HNN Associates. Manages roughly 7,000 units in the Seattle area, as well as others across Washington and Montana.

- Jones Lang Lasalle (JLL). A Fortune 500 company with annual revenue of $19.4 billion, operations in over 80 countries. Launched commercial real estate’s first AI-driven GPT model last year. JLL provides comprehensive real estate services in more than 4,000 buildings across the US and Canada.

- KRE Group. Founded by Jared Kushner’s uncle, it managed more than 20,000 multifamily apartments throughout thirteen states.

- LeFever Matson. Manages more than 3,000 units across California.

- Legacy Partners. Manages a portfolio of over 50 multifamily communities with more than 12,000 apartment homes

- Manco Abbott. As of 2005 (the most recent I could find), manages about 5,000 units in Central California.

- McWhinney Property Management. Based in Colorado with more than 4,000 apartment units completed or under construction.

- Morguard Corp. Manages nearly 18,000 units in the US and Canada, as well as 33.8 million square feet of commercial real estate.

- Pillar Properties. More than 2,000 units under management.

- Summit Management Services. More than 4,000 units across the country.

- Towne Properties. More than 15,000 units under management.

- Tribridge Residential. 6,000-plus units across Florida, Georgia, North Carolina, South Carolina, and Tennessee.

More information on the federal class action suit against Yardi Systems is available here, along with an investigation request form if you rented through one of the above companies.

[3] A report from the University of California, San Francisco released last year – the largest representative study of homelessness in the state in thirty years – found that economic factors were the main driver of homelessness, including low wages, a sudden unaffordable expense, and the rising cost of housing.