By Lambert Strether of Corrente.

Two narratives dominate accounts of wildfire causality: Careless or malevolent individuals (arsonists, ideally liberal Democrat donors) and climate change. From the New York Times:

While wildfires occur throughout the West every year, the link between climate change and bigger fires is inextricable. Wildfires are increasing in size and intensity in the Western United States, and wildfire seasons are growing longer. Recent research has suggested that heat and dryness associated with global warming are major reasons for the increase in bigger and stronger fires.

In an earlier post I showed that it was not possible to give an account of this year’s wildfires in Canada without considering the impacts of tree plantation monocultures. More generally, wildfire post mortems must examine not two layers — climate and the individual — but a third as well: Political economy. In Canada, timber companies. In California, real estate development.[1]

The current literature buries political economy under the anodyne phrase “Wildfire and the Wildland Urban Interface” (WUI). From FEMA:

The WUI is the zone of transition between unoccupied land and human [i.e., real estate] development. It is the line, area or zone where structures and other human development meet or intermingle with undeveloped wildland or vegetative fuels… The WUI area continues to grow by approximately 2 million acres per year. Approximately one in three houses and one in ten hectares are now in the WUI.

California has the greatest number of houses in the WUI. It’s easy for real estate developers to sell houses in the WUI because people[2] want to live in the woods:

“Many people like to live in places that happen to be susceptible to wildfires,” said study co-author Nicholas Irwin, an assistant professor in the UNLV department of economics. “It’s very attractive where the forest is, with beautiful trees in your backyard and unspoiled wilderness. People want to live there because of all of the natural amenities[3].”

From PNAS, “Rapid growth of the US wildland-urban interface raises wildfire risk“:

The wildland-urban interface (WUI) is the area where houses and wildland vegetation meet or intermingle, and where wildfire problems are most pronounced. Here we report that the WUI in the United States grew rapidly from 1990 to 2010 in terms of both number of new houses (from 30.8 to 43.4 million; 41% growth) and land area (from 581,000 to 770,000 km2; 33% growth), making it the fastest-growing land use type in the conterminous United States. The vast majority of new WUI areas were the result of new housing (97%), not related to an increase in wildland vegetation. Within the perimeter of recent wildfires (1990–2015), there were 286,000 houses in 2010, compared with 177,000 in 1990. Furthermore, WUI growth often results in more wildfire ignitions, putting more lives and houses at risk. Wildfire problems will not abate if recent housing growth trends continue.

This “non-abatement” of real estate development in California WUIs puts a lot of housing investment at risk. From the Sacramento Bee:

More than $20 billion worth of property was destroyed in the 2017 and 2018 fires. Nearly 3 million homes lie within the various “severity zones” mapped by Cal Fire, with thousands sitting in the “very high fire hazard severity zones,” the agency’s designation for the worst risks. A McClatchy analysis of Cal Fire’s wildfire risk maps revealed that more than 350,000 Californians live in towns and cities that lie almost entirely within those riskiest areas. Notably, almost all of Paradise sat in the highest risk zone before last November’s Camp Fire destroyed most of the town’s housing stock and killed 85 people. According to Zillow, the Riverside area has the most homes facing significant wildfire risk: 113,520 properties worth a combined $40 billion.

Of course, the Wildland-Urban Interface isn’t shifting the wild into the urban by magic, or because little elves are pushing it; it’s being moved by real estate interests:

Last year, fires destroyed over 1,000 structures in southern California. Despite this, the healthy real estate market facilitates further redevelopment. In addition to the market, increased population benefits California’s tax base, further motivating increasing population in the state.

If you’re like me, you might be wondering how this could happen. One main reason is related directly to the second point—that there is a high demand for prime real estate in California, leading to an increase in development.

Instead of curbing development in high fire risk areas, the California government is facilitating urban growth.

FAFO….

California, the Federal government, and the insurance business have all taken measures to mitigate wildfires, though none (almost none) have addressed the issue at the level of political economy. Instead, we have developed techniques of (you guessed it) “personal risk assessment”, as well as programs of collective risk assessment: forestry, tech, code enforcement, the courts, and insurance companies (of which only the last seems likely to succeed). Let’s take a quick tour of all these mitigations.

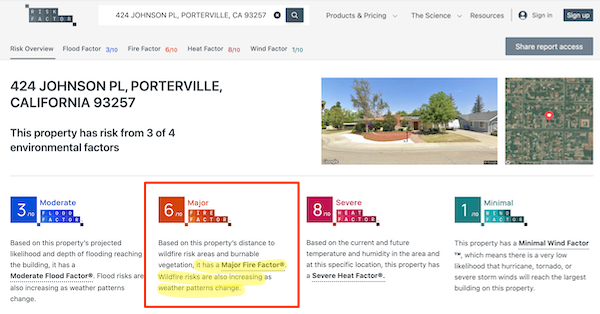

Personal Risk Assessment. I searched Zillow for California real estate, and this property came up at the top right:

424 N Johnson Place, Porterville, CA 93257 (Porterville being near the Valley Fire of 2015). As it turns out, there’s a new site from Risk Factor alluringly titled “What will climate change cost you?.” I typed in the address, and this screen came up:

Hoo boy (note all the vegetation[4] close to the house. Fire risk!) Will Risk Factor’s site, at the individual level — a real estate broker closing a deal with some PMC type who wants to work from home while looking out at Nature — make any difference at all? I’m guessing no, based on experience with personal risk assessment in our ongoing Covid pandemic. I think people think “It will never happen to me” along with “anyhow, I’m insured” (which we’ll get to).

Now to collective risk assessment in the form of tinkering round the edges public policy.

First, forestry. Unsurprisingly, the Biden Administration’s efforts have been trivial, and fail to address real estate development (a.k.a. WUI encroachment) at all:

Using chainsaws, heavy machinery and controlled burns, the Biden administration is trying to turn the tide on worsening wildfires in the US west through a multibillion-dollar cleanup of forests choked with dead trees and undergrowth.

Yet one year into what is envisioned as a decade-long effort, federal land managers are scrambling to catch up after falling behind on several of their priority forests for thinning even as they exceeded goals elsewhere. And they have skipped over some highly at-risk communities to work in less threatened areas, according to data obtained by the Associated Press, public records and congressional testimony.

If a latter-day King Canute sought to hold back wildfire instead of the tide, this is the approach he might take.

Second, tech. From the Santa Barbara News-Press:

California is deploying new tools – including AI, satellites, cameras, drones, and real-time intelligence alongside its largest standing army of firefighters and a fleet of aerial firefighting unmatched in number anywhere else on the planet.

Gov. Gavin Newsom joined state fire officials in Grass Valley to talk about the preparations that are taking place and the tools available to, and developed by California for seasons such as the one expected./p>

“In just five years, California’s wildfire response has seen a tech revolution. We’re enlisting cutting-edge technology in our efforts to fight wildfires, exploring how innovations like artificial intelligence can help us identify threats quicker and deploy resources smarter. And with the world’s largest aerial firefighting force and more firefighters on the ground than ever before, we’re keeping more Californians safer from wildfire,” Gov. Newsom announced.

Let me know how that works out. Somewhat more effective — at least ultimately — because actually addresssing real estate development–

Third, code enforcement From the International Journal of Disaster Risk Reduction:

The International Wildland-Urban Interface Code has established minimum building code standards which can improve home survivability from wildfires. Although technically designed for international use, these model codes have primarily been adopted within the United States and adapted for local jurisdictions’ use. For example, in California, construction in the WUI and other hazardous areas must comply with Chapter 7A of the California Building Code, the state’s variation of the International Wildland-Urban Interface Code. Compliance with these WUI building codes can prevent structure ignition[5], but the international codes and their site-specific variations (such as Chapter 7A) are relatively recent standards and often apply only to new construction. Codes enacted today may protect structures built in the future, but would not provide immediate protection in WUI areas.

More effective, since real estate development can actually be halted–

Fourth, the courts. One example from New York Magazine:

[Centennial’s] Tejon Ranch is an especially egregious place to put a brand-new mini-city. Here in the foothills, the risk of wildfire is already very high, and adding humans makes a spark more likely, meaning the state will be forced to mount a costly defense of people and property. And then there’s the challenge of supporting 60,000 people essentially in the middle of nowhere — at least 30 miles from any major job centers or public transit — along with all the cars needed to haul them around and maintain their daily lives. These arguments in the lawsuit from Climate Resolve — which sued successfully to stop a freeway from being built in the nearby High Desert — are the latest in a quarter-century saga of legal attempts to prevent development at Tejon Ranch.

And from The Real Deal:

A Lake County Superior Court judge ruled this week that the so-called Guenoc Valley Project can’t move forward until planners figure out what would happen should a mass evacuation sends thousands of residents fleeing down the small country roads that lead to the community.

The development, proposed by Lotusland Investment Group of San Francisco, features the homes along with a golf course, culinary school and five boutique hotels on 25 square miles of rolling hills snuggled between Sonoma and Napa counties — but on land that has been hit by fires four times in the last 10 years, and 11 times since 1952, according to the suit.

Finally, the Big Kahuna: The insurance business:

But State Farm’s exit from California last month due to wildfire hazards caused a stir.

“So now that they’ve bowed out, that’s going to be a real issue, especially in those heavy fire markets where you’re paying premium for that,” Josh Altman, co-founder of The Altman Brothers, told Yahoo Finance Live. “Now, that’s going to be a major, major blow to those properties.”

State Farm cited “historic increases in construction costs outpacing inflation, rapidly growing catastrophe exposure, and a challenging reinsurance market” for its decision.

The move from State Farm follows AIG’s announcement last year that it was leaving the California market. AIG recently stated that it was limiting property insurance coverage in New York, Delaware, Florida, Colorado, Montana, Idaho and Wyoming, according to the Insurance Journal.

And last week, Nationwide announced “it is taking [action] to mitigate risk and manage the personal and commercial lines portfolios in the current environment.” Although no details have been outlined regarding which personal insurance lines will be impacted, the changes vary by state and territory, according to the Insurance Journal.

As more insurers leave California it could morph into an impending issue as costs rise making homeownership pricier than it presently is with mortgage rates at 6.75%, Scott Sheldon, branch manager at New American Funding, told Yahoo Finance.

If insurance rates get high enough — or if insurance isn’t possible — will that bring real estate development in California’s WUIs to a halt? Time will tell[6].

I don’t really have a policy recommendation here, other than at least freezing real estate development in wildfire-prone areas, an unrealistic proposition (“not politically feasible,” and how to grandfather existing properties?). Perhaps the insurance industry will stop the madness to avoid its own collapse, but the magic of the marketplace hasn’t been working too well lately, has it? At least for most of us. I hate to say “Let it all burn,” but isn’t that where we are?

So to remind us all that a different world was and is possible, I’ll close with this alternative approach to fire from Charles C. Mann:

Like people everywhere, Indians survived by cleverly exploiting their environment. Europeans tended to manage land by breaking it into fragments for farmers and herders. Indians often worked on such a grand scale that the scope of their ambition can be hard to grasp. They created small plots, as Europeans did (about 1.5 million acres of terraces still exist in the Peruvian Andes), but they also reshaped entire landscapes to suit their purposes. A principal tool was fire, used to keep down underbrush and create the open, grassy conditions favorable for game. Rather than domesticating animals for meat, Indians retooled whole ecosystems to grow bumper crops of elk, deer, and bison. The first white settlers in Ohio found forests as open as English parks—they could drive carriages through the woods. Along the Hudson River the annual fall burning lit up the banks for miles on end; so flashy was the show that the Dutch in New Amsterdam boated upriver to goggle at the blaze like children at fireworks. In North America, Indian torches had their biggest impact on the Midwestern prairie, much or most of which was created and maintained by fire. Millennia of exuberant burning shaped the plains into vast buffalo farms. When Indian societies disintegrated, forest invaded savannah in Wisconsin, Illinois, Kansas, Nebraska, and the Texas Hill Country. Is it possible that the Indians changed the Americas more than the invading Europeans did? “The answer is probably yes for most regions for the next 250 years or so” after Columbus, William Denevan wrote, “and for some regions right up to the present time.”

Here, the very concept of a WUI is irrelevant; the Indians worked on a continental scale. A different political economy indeed…

NOTES

[1] Many California wildfires have also been caused by Pacific Gas & Electric (PG&E), which has not seemed to believe that clearing trees and brush away from its power lines is part of its corporate mission; see NC here, here, and here. Now they are changing their tune, and have asked for a $7 billion Federal loan to bury their power lines. For the purposes of this post, I will assert that the location of PG&E power lines is a function of real estate development.

[2] People who can afford housing, that is. “To keep a house payment below 30% of your income after putting 20% down, a person would need to earn roughly $16,693 per month or $200,316 per year – just to buy a median-priced home in California.” So when we talk about houses burning down in California wildfires, the odds, at least if the house is new, are that we are not talking about working class Californians.

[3] A tree is not an “amenity.” This is the vile “ecosystem services” paradigm rearing its ugly head again.

[4] I give the sellers points for the xeriscaping.

[5] Granting that structure ignition were prevented on the ground, code won’t address power lines, other environmental factors like roads and grasses, and of course the damage to the “wild” itself, including trees, animals, water, air, etc.

[6] I would expect a push for government insurance, as for people whose houses are on flood plains or on the ocean shore.