The German military’s recklessness has been getting a lot of attention recently due to the leaked audio of German military officers casually discussing attacks on Russia.

You can draw a direct line from the foolishness of attacking Russia with a total of 100 Taurus missiles to the ongoing rapid economic decline at home. The incompetence evident in both continues to be on display as decisions in Berlin only make matters worse, and Germany’s insistence on austerity for the rest of Europe are helping to ensure the rest of the EU will be dragged further down as well.

The ramifications of such policies are likely to be substantial as Europe’s working class is increasingly opposed to the conflict with Russia and are becoming increasingly hostile to the EU, and in response elites are cracking down on democratic rights, threatening to ban parties and limiting speech.

The ineptitude – from Berlin to Brussels and across most European capitals – is so pervasive it’s enough to leave one wondering whether it’s intentional as part of some sort of targeted demolition with an ulterior goal.

“Dramatically Bad”

The economic growth forecast for Germany was recently slashed down to 0.2 percent in 2024, plunging from the previous projection of 1.3 percent. Germany’s economy minister Robert Habeck is now complaining about Germany’s elevated energy prices that are driving companies in Germany to move production out of the country. He recently said the country is performing “dramatically bad.” Habeck, from the Greens, has been economy minister since 2021. And one doesn’t need to look much further than him and his team for why the situation is as it is.

Germany’s economic slump is now widely seen as structural rather than temporary, as the country is struggling with higher energy prices following the loss of cheap and reliable Russian energy. Habeck and the Greens were some of the staunchest supporters of the conflict with Russia and getting rid of Russian fossil fuels, as well as Germany’s nuclear power, so they must be ramping up clean energy, right?

Not exactly. According to a report released March 7 by the German Federal Court of Auditors. It found that the expansion of renewable energies and the electricity grid is way behind schedule, and that there isn’t enough generation capacity to meet demand.

Habeck, who is also the federal minister of climate action, dismissed the report, saying it “does not reflect reality.”

The reality is inflation continues to be problematic, the economy is contracting as industry shrinks, exports to China are declining and there is constant pressure from Atlanticists to self-impose a further reduction, living standards are declining, social spending is being scaled back in favor of more military spending, wealth inequality grows, and industry continues to leave the country.

Meanwhile, Berlin recently approved a 2024 subsidy plan worth 5.5 billion euros to help soften the blow of rising electricity prices. The government can’t do much more without continuing to take away from other German social spending. Germany’s Finance Minister Christian Lindner is opposed to any suspension of the country’s debt brake and instead wants to slash corporate tax rates, which would be financed with expenditure cuts.

Germany’s corporate tax rate is higher than global competitors, but there’s reason to believe lowering them while cutting public spending would not lead to economic growth and would likely make Germany’s economic situation even worse.

Economist Philip Heimberger, author of a 2022 study that shows there is little empirical evidence for positive growth effects from corporate tax cuts, believes Lindner’s plan is misguided:

Especially if government spending is cut elsewhere at the time of the corporate tax cut, weaker growth effects are to be expected. In view of the problems associated with complying with the debt brake and the resulting prospect of government spending cuts, caution is therefore required, especially as a corporate tax cut would lead to a (continued) decline in government revenue.

A loss of tax revenue in turn reduces the provision of public goods such as infrastructure and education. However, the quality of the location for companies and their business prospects are dependent on high-quality public goods.

For German companies to invest more again and for the economy to grow more strongly, the business case for investment must be right. The government would have to make it easier for decision-makers in companies to plan by combining a clear industrial policy strategy with public investment in order to attract further private investment. The turbulence within the federal government surrounding compliance with the debt brake and uncertainties as to whether even long-announced fiscal policy measures in favor of companies can be financed are counterproductive.

Germany’s corporate taxation is no longer competitive internationally, it is claimed. Positive effects from across-the-board profit tax cuts are mainly achieved, if at all, by companies relocating to Germany at the expense of other countries. Despite its current weak growth, Germany is Europe’s most powerful country both politically and economically. As such, its government should not promote a race-to-the-bottom in corporate taxation that does little for growth.

What does all this mean for Germans? For one, this year’s budget, which includes the highest military expenditure since the end of WWII (much of it for Ukraine) and massive cuts in the areas of healthcare, education, and social welfare, could be just a preview of what’s to come.

And it’s a model that is being forced on the rest of Europe.

Making a Bad Situation Worse

Germany also continues to insist on stricter fiscal rules for Europe, which will likely only worsen the economic pain already being felt by millions across the bloc largely due to the economic war against Russia.

In February, a last-minute agreement between the European Commission and Parliament will force EU member states to slash debt ratios and deficits while maintaining investment in “strategic areas such as digital, green, social or defense.”

At the same time, according to Bloomberg, EU officials and investors are using the fiscal rules to push for an EU-wide bond program that would bring the investors bigtime profits while allowing the bloc to ramp up military spending without individual nations incurring more debt.

After years of using the escape clause in order to deal with the economic fallout of the pandemic, the return of fiscal rules in the form of the new “economic governance” framework might help the EU get its coveted war bonds, it will also mean more austerity. – especially for those nations with high public debt ratios, such as Italy, Spain and France.

Let’s not forget that the EU is pushing this despite its own polling of bloc citizens showing that nearly 80 percent favor stronger social policies and more social spending.

The Potential Consequences

The piling of crisis upon crisis – all of which reduce the standard of living of the majority of Europeans – has predictable consequences. A paper last year titled The Political Costs of Austerity details what’s already happening:

Fiscal consolidations lead to a significant increase in extreme parties’ vote share, lower voter turnout, and a rise in political fragmentation. We highlight the close relationship between detrimental economic developments and voters’ support for extreme parties by showing that austerity induces severe economic costs through lowering GDP, employment, private investment, and wages. Austerity-driven recessions amplify the political costs of economic downturns considerably by increasing distrust in the political environment.

Brussels has managed to keep a lid on anti-EU parties across the bloc despite their increasing vote share. The Chega Party in Portugal is just the latest “far-right” winner from voters’ disgruntlement with the erosion of their economic standing and democracy. Case in point, plans were immediately implemented to freeze Chega out of any coalition.

In Europe’s second-largest economy, the presidential election isn’t until 2027, but Marine Le Pen is already making herself more acceptable to the transatlantic permanent state:

The Melonisation — i.e., self-domestication — of Le Pen proceeds apace. After giving up on her anti-euro platform, she’s now appeasing NATO and Washington. She’s almost ripe for being allowed to govern. pic.twitter.com/efTTROq3wp

— Thomas Fazi (@battleforeurope) March 14, 2024

While this tweet refers to Italian Prime Minister Giorgia Meloni’s abandonment of her and her party’s past positions on NATO and the EU, the case of Europe’s second largest industrial economy, Italy, is instructive in many other ways, as it is a harbinger of what’s to come for other EU nations like Germany. Three points there:

1. Italy is reeling from the energy crisis, but it has been reeling for more than two decades with declining living standards since its joining of the single currency:

Annual net income of the Italian household, which was €27,499 (at constant 2010 prices) in 1991, declined to €23,277 in 2016—a drop in median living standards of 15%. Mean net household income fell by €3,108 between 1991 and 2016 or by about 10%. Italy is the only major Eurozone country that, in the past 27 years, suffered not stagnation but decline.

2. Then the economic war against Russia made things worse as energy prices surged more than 50 percent in 2022 and have yet to decline. Inflation, real wages, and industrial activity are all heading in the wrong direction.

In January, an Italian court allowed energy companies to cut off gas supplies to steel company Acciaierie d’Italia (ADI), majority owned by multinational steel giant ArcelorMittal, over mounting debts.This is the company’s main plant, which is in the southern Italian city of Taranto and is one of the largest in Europe. It employs about 8,200 people and many other jobs depend on the plant.

The response from Italian and Brussels elites is always the same: more wage suppressions, more market-friendly reforms, more social spending cuts, and more privatization. It was only a few months ago that the New York-based private equity firm KKR, which includes former CIA director David Petraeus as a partner, reached a controversial agreement to buy the fixed-line network of Telecom Italia. Now the Italian daily La Repubblica is declaring that “Italy Is For Sale,” in which it describes plans for 20 billion euros worth of privatizations, including more of the state rail company Ferrovie dello Stato, Poste Italiane, Monte dei Paschi bank and energy giant Eni. The plan is reportedly necessitated by the country’s tax cuts. The roughly 100 billion euros Rome has burned through in order to address the energy crisis surely hasn’t helped either. And this was happening with the suspension of the EU debt brake.

3. Now, according to Breugel, the new EU fiscal rules will for Italy translate into a structural primary balance requirement of over 4 percent of GDP. That will mean ongoing public service cuts and the privatization of just about whatever hasn’t been strip mined yet. And it will mean that Brussels’ neoliberal austerity policies will continue to increase the gap between rich and poor.

How does all the economic carnage translate at the political level? At the end of 2022, voters already went with the candidate (Meloni) who fashioned herself as an EU- and NATO-skeptic. She turned out to be neither.

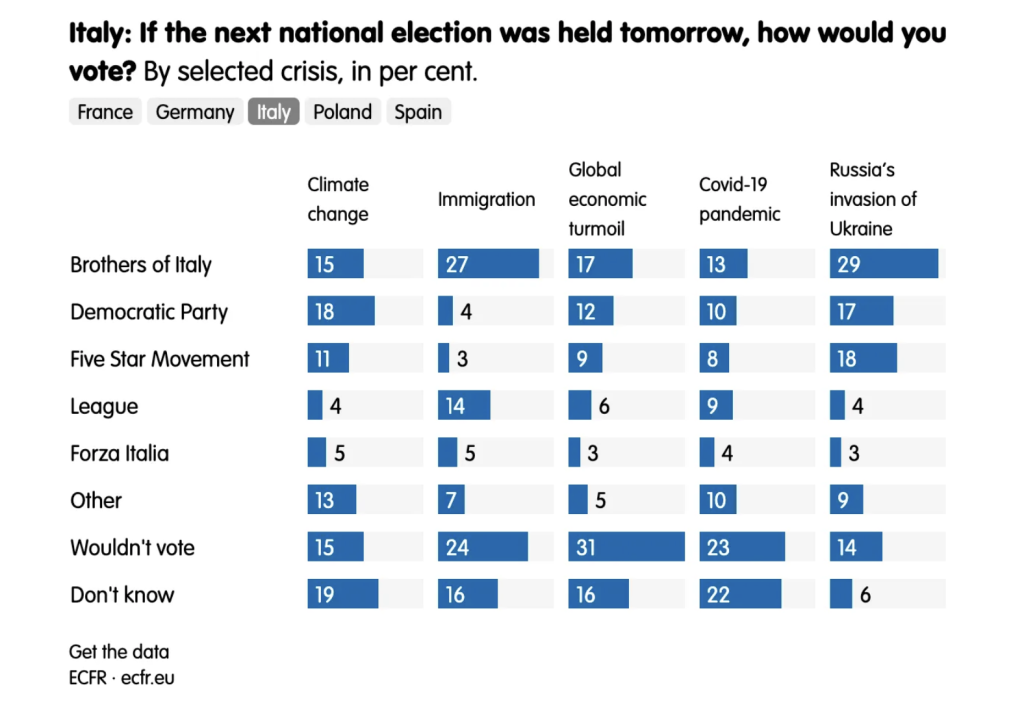

Where do voters turn to now? As of now, one third of Italian voters rate the economy as their top concern, and most have nowhere to go:

This helps explain why the turnout in Italy’s 2022 election was the lowest since WWII. Similar low levels are being seen in France, Germany, and elsewhere. This is probably the way Ursula von der Leyen and the European Commission like it, but for how long can it last?

Working class Europeans are increasingly waking up to the fact that the EU is a project of class warfare on labor. Trust in EU institutions continues to decline while 66 percent of the EU working class feel their quality of life is getting worse. In short, Brussels’ policies are creating a groundswell of opposition to the EU.

As is the case across much of Europe, support for the EU in Italy is already largely divided along class lines:

Recent survey evidence suggests that support for the euro has a clear income and class bias. The perception of having benefited from the euro grows with income and is highest among self-employed professionals and large employers, technical (semi-)professionals, and associate managers, while production and service workers and small business owners are much less likely to report that they have benefited from the euro. In brief, in Italy support for the euro is concentrated among the economically better off and, with regard to partisan choice, among voters of the centre-left. In turn, the more a person has benefited from the euro, the more likely she/he is to report that she/he would vote to remain in the euro in a hypothetical referendum. Importantly, the majority of Italian voters report that they have not benefited from the euro, which makes support for the single currency rather fragile.

While there is ongoing escalation against Russia and China abroad, so too we’re seeing escalation at home. While the likes of von der Leyen lecture countries on the dangers of electing anyone they consider a threat to what they call the “liberal consensus,” they increasingly use warnings of “tools,” threats to ban parties, crackdowns on speech to arrive at that consensus.

There is more pushback – whether farmers’ protests, political parties calling for new direction, or simply individuals or groups airing unwanted viewpoints. As of now, they are smeared as far right or as personifications of Russian propaganda, but at what point does the number of those being smeared reach critical mass?

Or to put it another way: As capital continues to gobble up the European welfare states and living standards decline, citizens are asked to sacrifice even more for the wealthy’s economic wars, which they are told are fights over democratic values. Meanwhile, those values are increasingly trampled at home in order to silence opposition to said economic wars. That does not seem like a sustainable model.