Yves here. Please welcome back Satyajit Das, who has graciously published posts on banking, derivatives, centralized clearing houses, and economic issues, is providing a series on energy needs and the implications of energy transition proposals. As he introduces this exposition:

Abundant and cheap power is one of the foundations of modern civilisation and economies. Current changes in energy markets, perhaps the most significant for a long time, have implications for society in the broadest sense. Energy Destinies is a multi-part series examining the role of energy, demand and supply dynamics, the shift to renewables, the transition, its relationship to emissions and possible pathways. The first part looks at the part played by power in the rise of modern societies and patterns of demand and supply over time.

By Satyajit Das, a former banker and author of numerous works on derivatives and several general titles: Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006 and 2010), Extreme Money: The Masters of the Universe and the Cult of Risk (2011), A Banquet of Consequences RELOADED (2021) and Fortune’s Fool: Australia’s Choices (2022)

Energy’s Role In Modern Civilisation and Economies

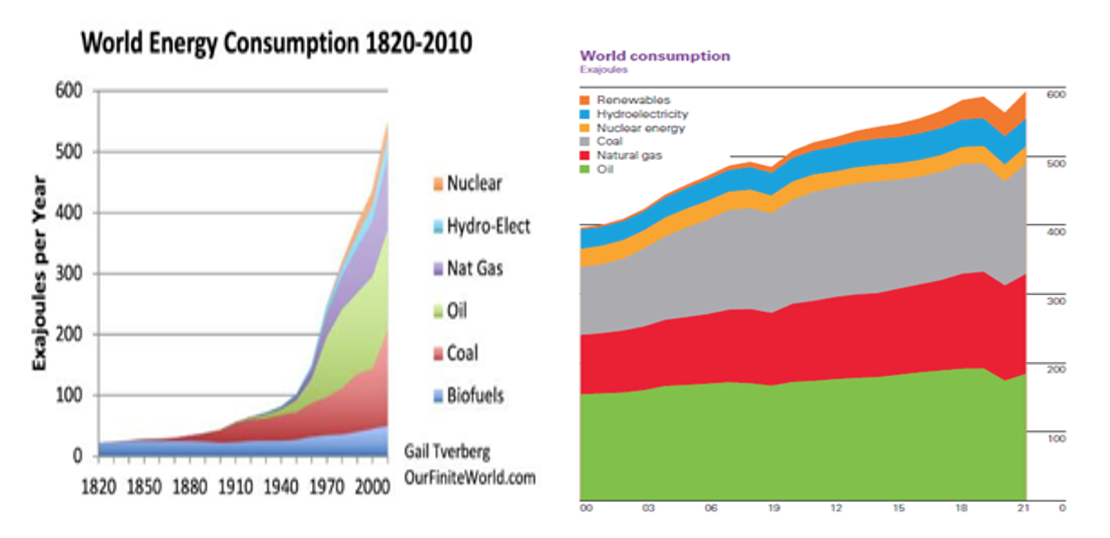

The last two centuries of human history were the ‘age of fossil fuels’. Abundant and cheap energy has revolutionised industry, transportation and lifestyles driving growth and wealth creation. It expanded the scope of human activity to an unparalleled degree. The correlation between oil use, population, growth and living standards is captured in the work of actuary Gail Tverberg and others:

Energy use per capita is increasing. Since 1950, global population has increased by 3.1 times while energy use has increased 6.4 times. The increase in energy use per capita is driven by:

- Increased use by residents of emerging markets who have been traditionally low energy users as incomes rise.

- New uses of energy related to higher living standards, particularly since the second World War.

Uninterrupted supplies of energy on current terms is widely assumed. However, the availability of reasonably priced energy is not assured. In the last half century there have been at least three energy shocks – the oil shocks of 1974 and 1978 and the 2022 Ukraine conflict. All have been relatively short in duration with a rapid reversion to the status quo although the long term repercussions of 2022 is difficult to predict. The more fundamental underlying change under way may not resemble these past shocks in terms of scope and scale.

Sources of Energy Demand

Careful parsing of demand and supply and the underlying physics, chemistry and economics are required to understand the shifts in train.

The major users of energy are households and industry. The industrial sector (mining/ refining, manufacturing, agriculture, and construction) constitutes the major energy consumer —more than 50 percent of end-use. Increasingly, much of industrial sector energy use occurs in non-OECD nations.

Power is needed for:

- Lighting

- Climate control (cooling/ heating)

- Powering appliances and machinery

- Transportation

These uses are common to households and industries. There are differences; industrial application focus on operating industrial motors and machinery as well as heavy transportation. Industrial energy intensity, for example to manufacture steel, aluminium or concrete, is also magnitudes greater than that required for normal household use.

Industry also uses fossil fuels as feedstocks (raw materials) for products such as plastics and chemicals, especially ammonia and bitumen type products. It is essential as the base raw material for items such as lubricants. Coal, crude oil or petroleum, natural gas liquids, and natural gas are the primary sources of basic petrochemicals. Around 9–10 percent of global fossil fuel production is used as feedstock.

Plastics require hydrogen and carbon, with the most common production method being extraction of ethylene, propylene, styrene etc from oil. Petrochemicals such as naphtha and other oils refined from crude oil are used as feedstocks for petrochemical crackers that produce the basic building blocks for plastics. Fossil fuels represent currently represent 99 percent of the plastics raw material base. There is a growing interest in the use of biomass as a feedstock. While data is sparse, it is likely that around 4 percent of the world’s fossil fuel resources are used in plastics production.

Oil is used in the production of ammonia as the nitrogen source in agricultural fertilizers. Global ammonia production currently accounts for around 2 percent of total final energy consumption; around 40 percent as feedstock and 60 percent as process energy, mainly for generating heat.

Energy demand is also changing. Data storage and transmission, as well as crypto mining, now consume 1-2 percent of global energy.

Historical Energy Demand

Global demand has increased over time:

It continues to increase, although the rate has slowed over time to 1-2 percent per year. There have been brief interruptions in the early 1980s, and 2009 as a result of financial crises and the 2020 Covid19 pandemic.

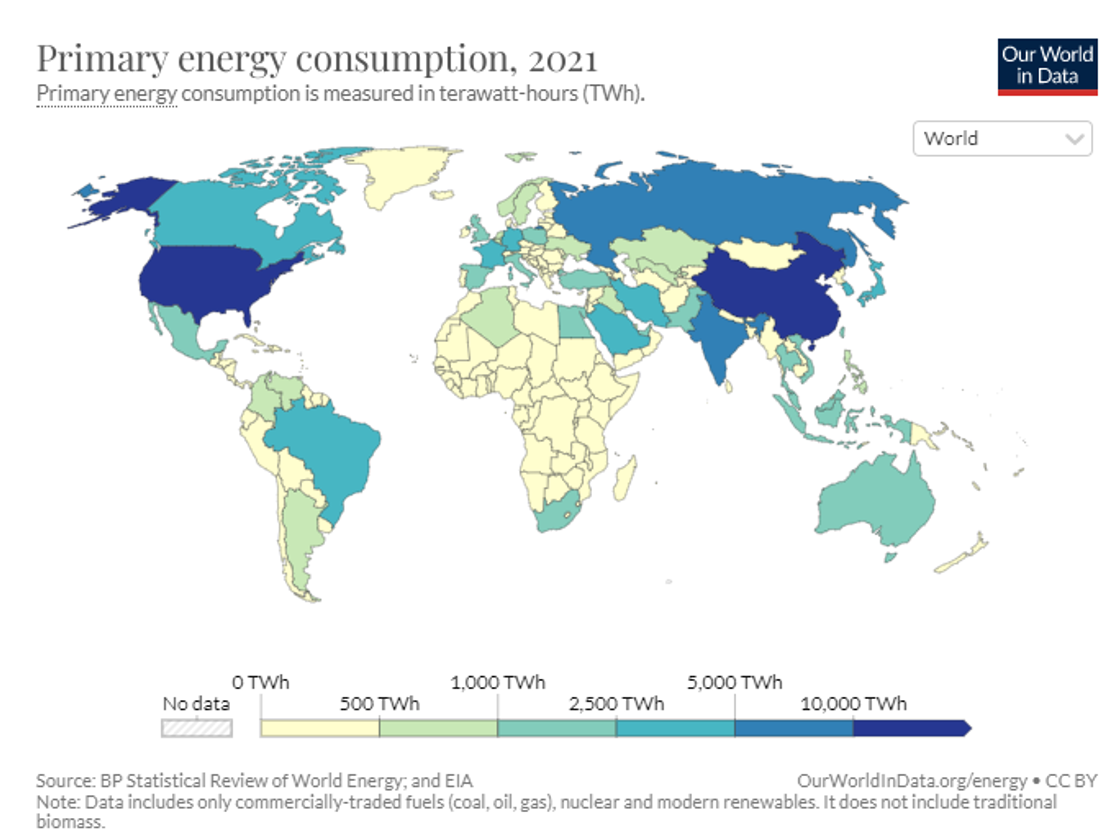

The bulk of energy consumption is in developed countries. Some emerging countries such as China show high levels of consumption driven by advanced economies outsourcing polluting and energy intensive activities to these locations.

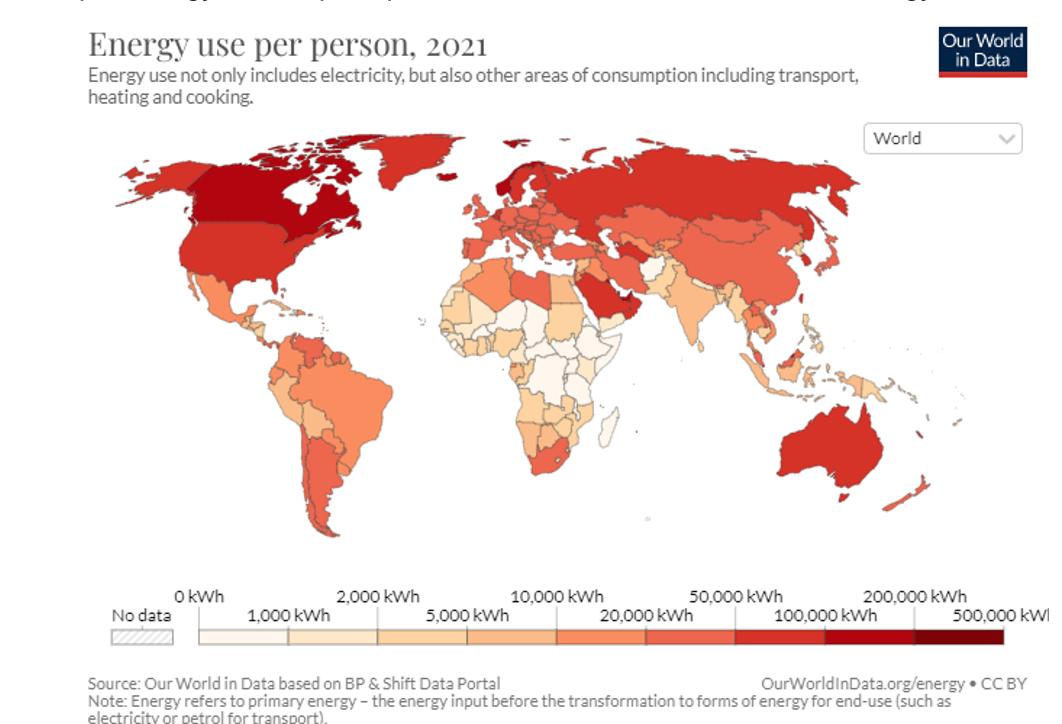

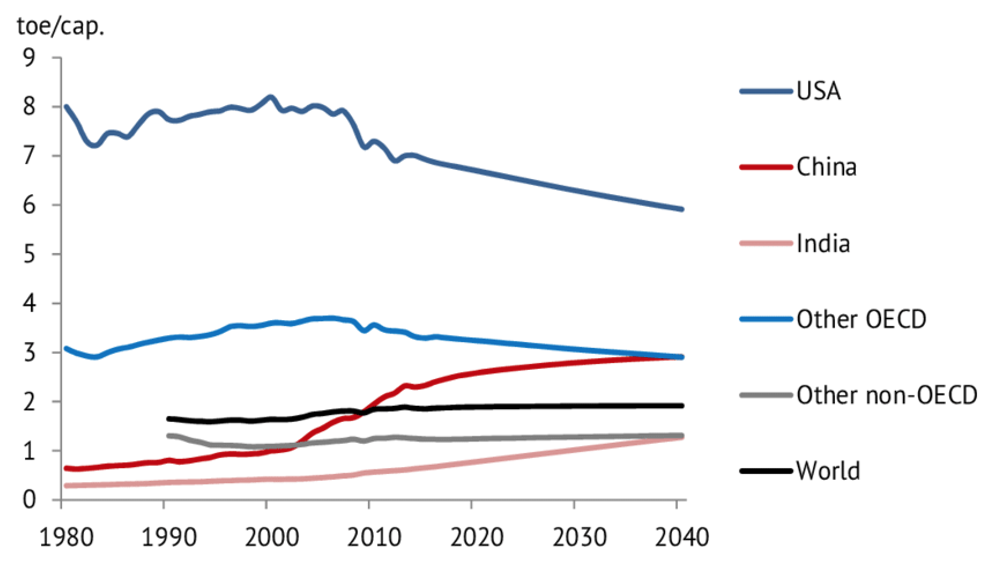

Per capita energy consumption provides a more accurate measure of energy demand.

The largest energy consumers on a per capita include the US, Canada, Iceland, Norway, Australia and Russia as well as Middle East such as Oman, Saudi Arabia and Qatar (in part due to climate and desalination to meet water needs).

The average person in high energy use per capita countries use up to 100 times more than the average person in some of the poorest countries. The true difference is under estimated due to lack of high-quality data for many of the world’s poorest countries. Low income countries use less commercially-traded energy sources instead relying on difficult to quantify traditional biomass – crop residues, wood and other organic matter that is.

Demand has been ameliorated, in part, by increases in energy efficiency. This is uneven with bulk of gains in advanced nations with increases of varying degrees in developing nations.

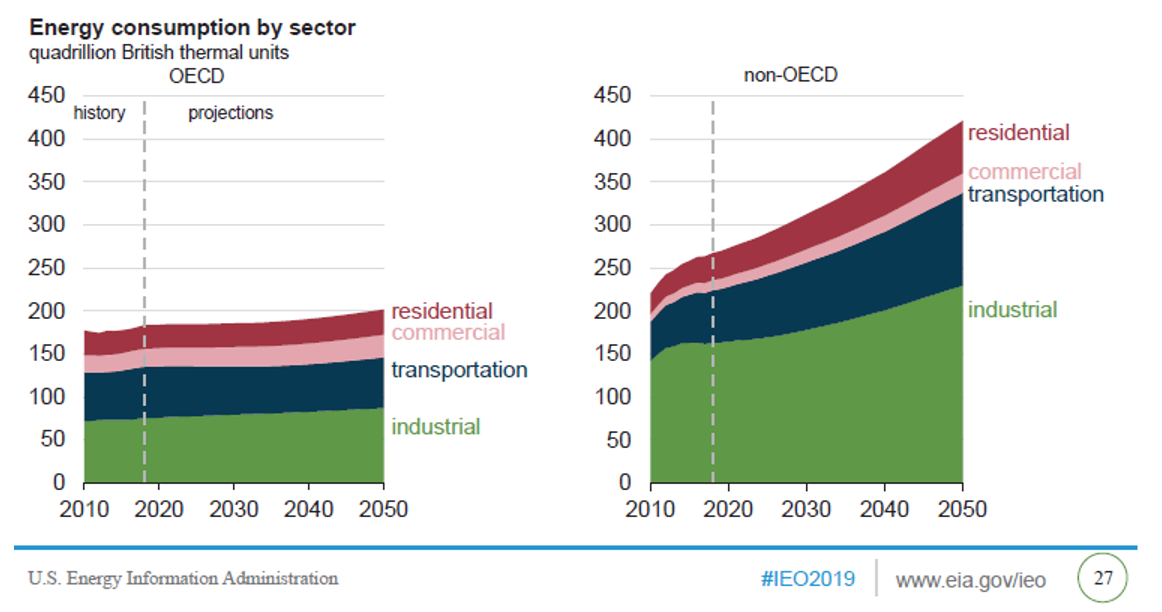

Forecast Energy Demand

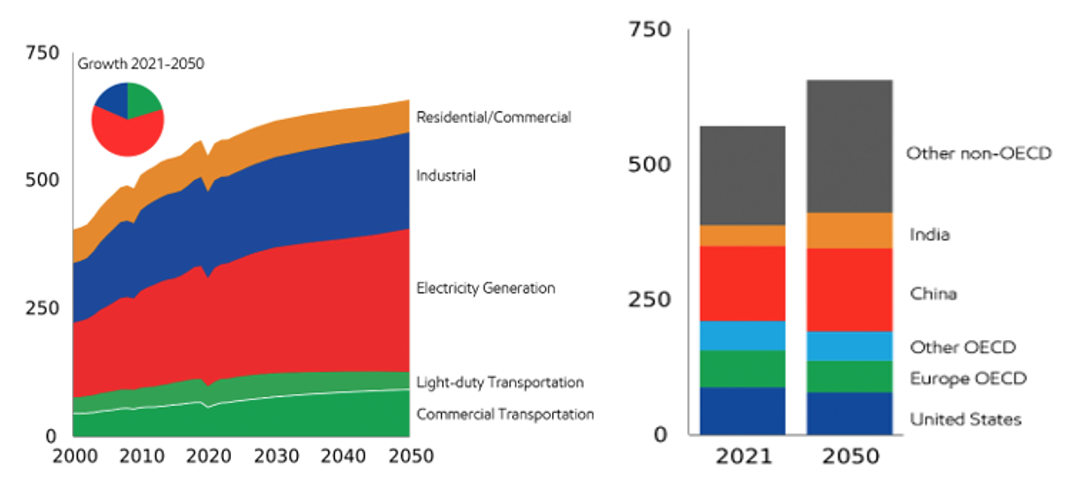

Forecasts of future energy demand vary. S&P forecasts combined residential and commercial energy demand will rise by around 15 percent through to 2050. ExxonMobil projects similar growth.

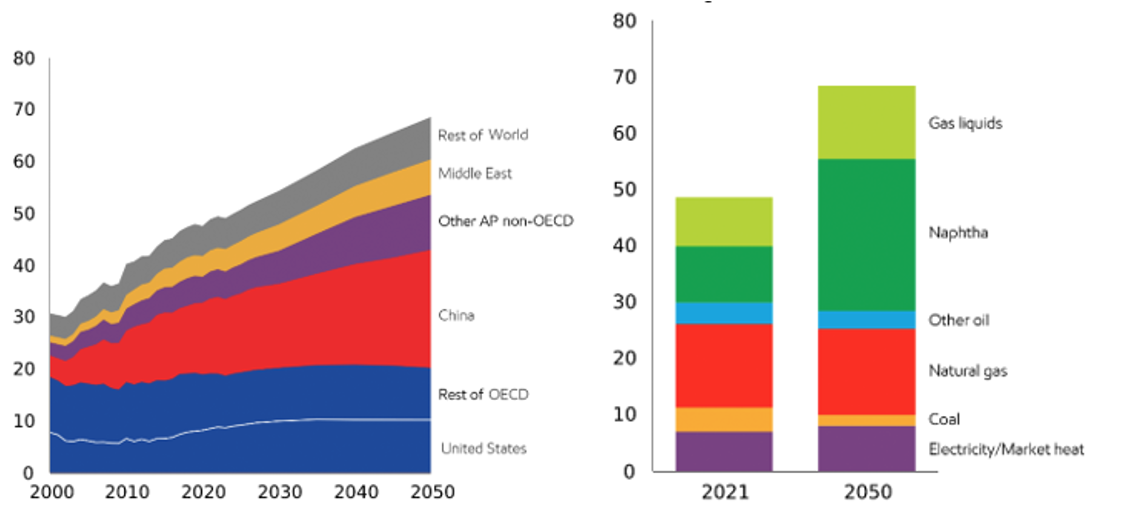

There is broad agreement on the pattern of increasing energy needs. Much of this growth will be in developing nations. Most of the growth comes from industry underpinned by increases in population and living standards. Energy-intensive manufacturing of such products as chemicals, food and iron and steel is forecast to increase. This is led by activity in China and India. Average worldwide household electricity use is expected to rise by about by 2050.

Overall growth in energy demand (in quadrillions of BTUs (British Thermal Units)) is projected to be as follows:

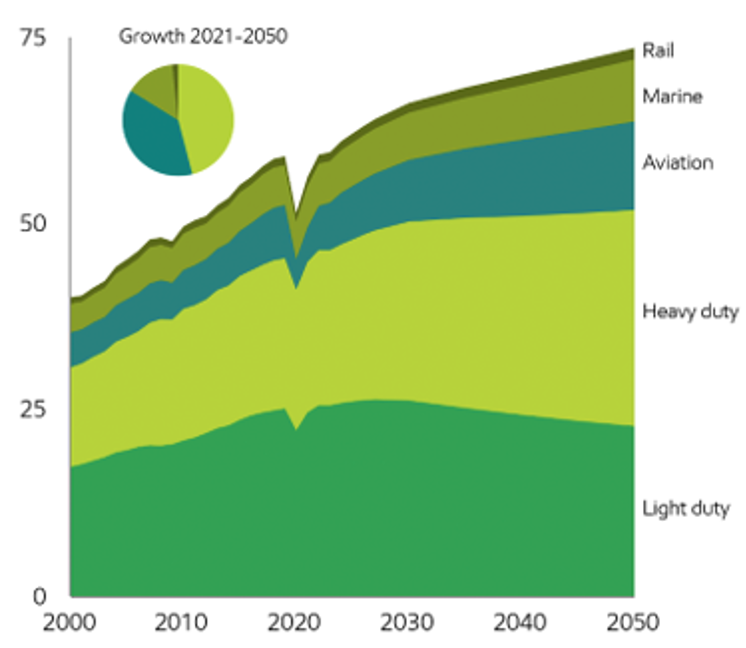

Global transportation demand is expected to grow by 30 percent to 2050. This reflects greater personal vehicle ownership, especially in emerging markets with purchasing power rises, offset in part by higher fuel efficiency and more electric vehicles (“EVs”). Strong commercial transportation (heavy-duty trucking, aviation, marine and rail) energy demand is driven by growth in economic activity and consumption, in particular the increasing middle class consumers in emerging economies.

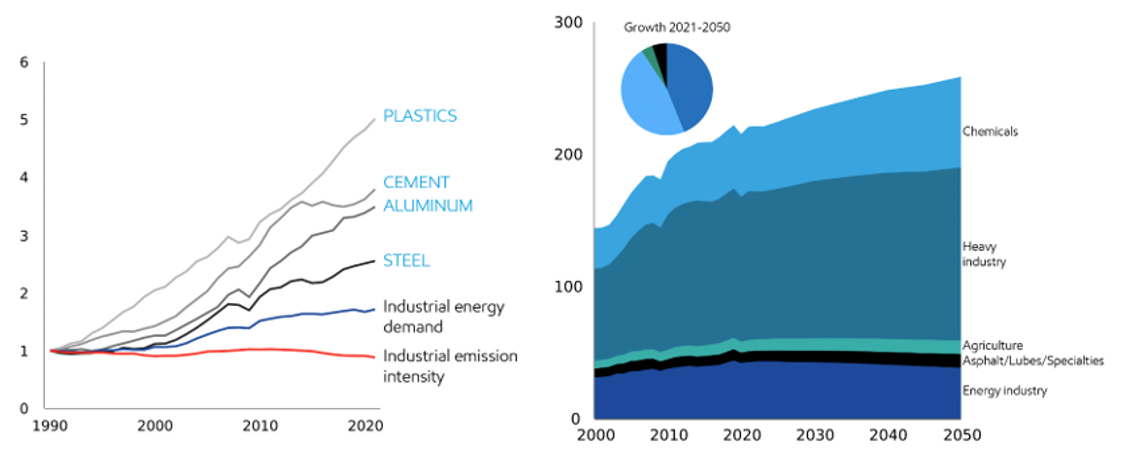

Industrial energy demand will continue its strong rise over recent decades focused around steel (used for large-scale construction, shipping containers, trains and ships), Aluminium (power grids, construction and vehicles), cement (construction) and plastics ( medical supplies, cleaning products, electric vehicles, and household goods).

Demand from heavy industry will, in part, be offset by improvements in energy intensity (the amount of energy used per dollar of overall economic activity). Developed nations will benefit from the shift to service-based economies and predominance of higher-value, energy-efficient industries. Improvments in energy intensity require advances in technology, processes and logistics and their adoption in major manufacturing hubs like China.

There will be strong increases in demand for production of chemicals due to need for fertilizer, cosmetics, textiles and plastics. Much of this will require fossil fuel based feedstocks.

The above focuses on traditional uses. Over time, the requirements of data and computation technologies are likely to increase significantly. Additional demand is likely, ironically, to come from attempts to combat climate change, such as processing additional or new materials for the energy transition as well as carbon capture and sequestration projects. The energy demand from these sources remains unquantified.

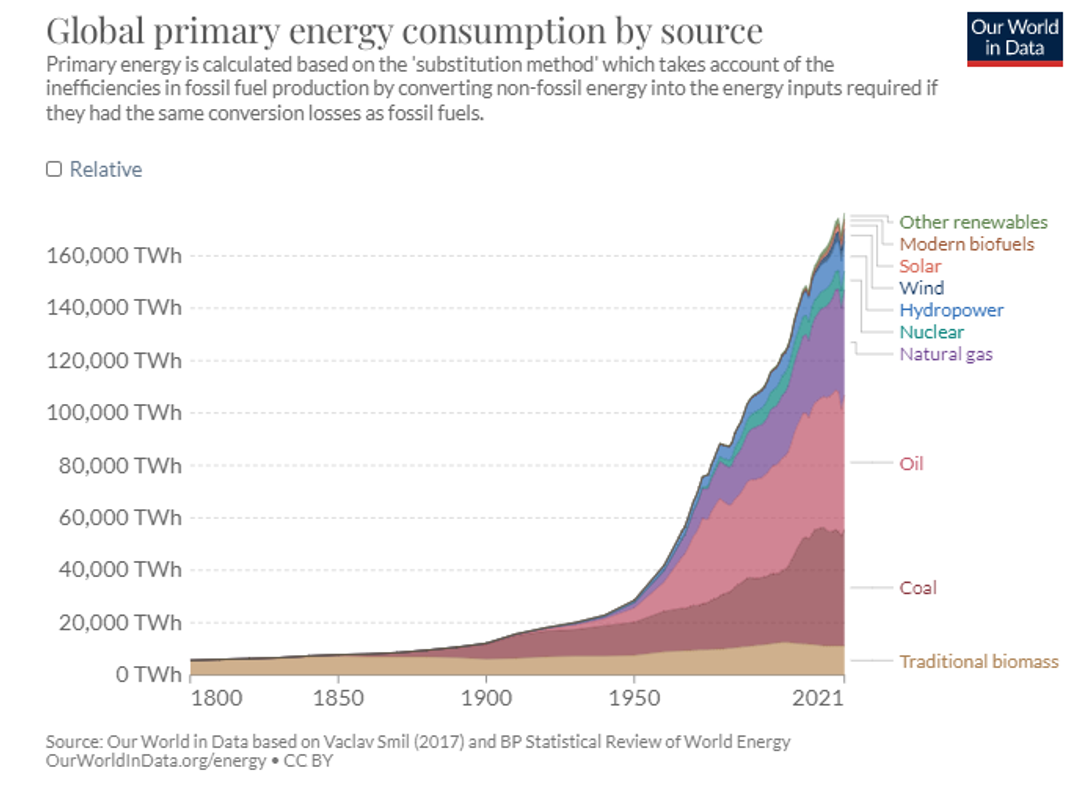

Energy Sources

Global demand is met from a variety of sources.

Several points should be noted:

- Energy demand has historically been met primarily by fossil fuels.

- The mix of fossil fuels has changed over time with oil and more recently gas supplementing coal.

- Over the last few decades, new renewables (primarily solar and wind) have supplemented hydro and biomass power.

- Fossil fuels (which now make up around 80 percent of energy sources) are likely to remain a significant part of energy supply, primarily because of their advantages over alternatives.

- Renewables will increase as a proportion of the energy mix but, based on current technology, it is unlikely to become a dominant source in the foreseeable future.

Fossil Fuel Reserves

Given the importance of fossil fuels as an energy source, an important and frequently ignored question is the long term availability of inherently finite fossil fuels.

Estimated total global oil reserves are around 1,700 billion barrels. Estimated total global natural gas reserves are around 190 trillion cubic metres. Estimated total global coal reserves are around 1,070 billion tonnes. Based on current production and usage, oil will run out in 54 years, natural gas in 49 years, and coal in 139 years, assuming that fossil fuels will constitute 59 percent of the total primary energy demand in 2040.

Several issues should be highlighted:

- There is wide variation in reserve estimates and expected lives of fossil fuel reserves. For example, some oil companies have written down available reserves significantly in recent years.

- New discoveries as well as extending the life of known resources may increase reserves.

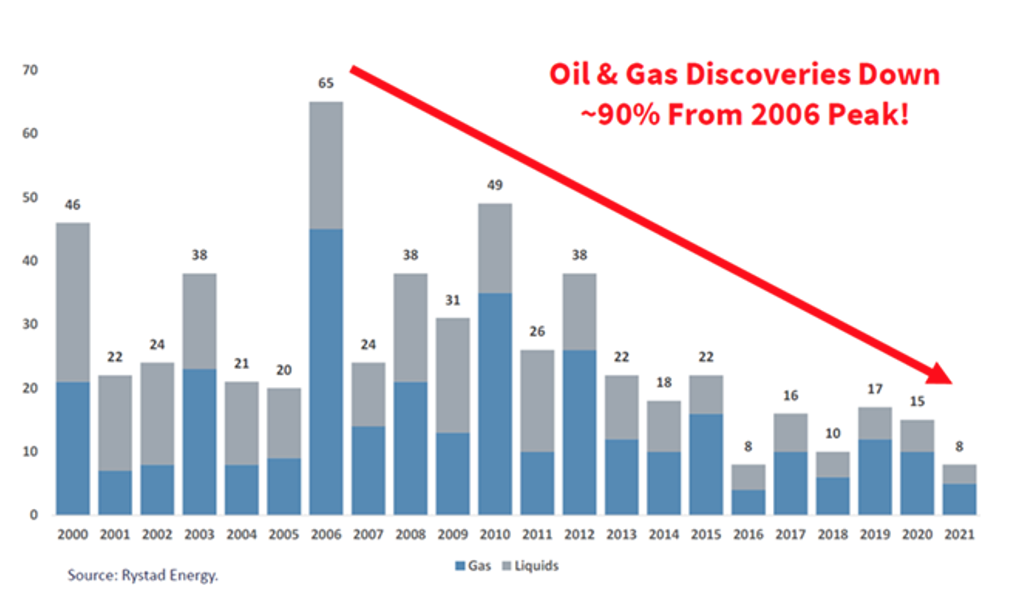

- The number of major oil and gas field discoveries has decreased, in part due to reduced investment in fossil fuels.

- Reserves may not be economically recoverable except at high prices due to technical difficulties in extraction. Many new resources are unconventional oil and gas fields, previously considered inaccessible or uneconomic resources, such as deep oceans or the Arctic. These typically require higher prices to be economic: currently around $80 per barrel for oil obtained using advanced recovery techniques, $90 per barrel for tar sands and extra-heavy oil, $50+ for shale gas, kerogen oils and Arctic oil, and $100+ for coal-to-liquids and gas-to-liquids.

- Reserves may also be difficult to access because of remote locations and politically instability.

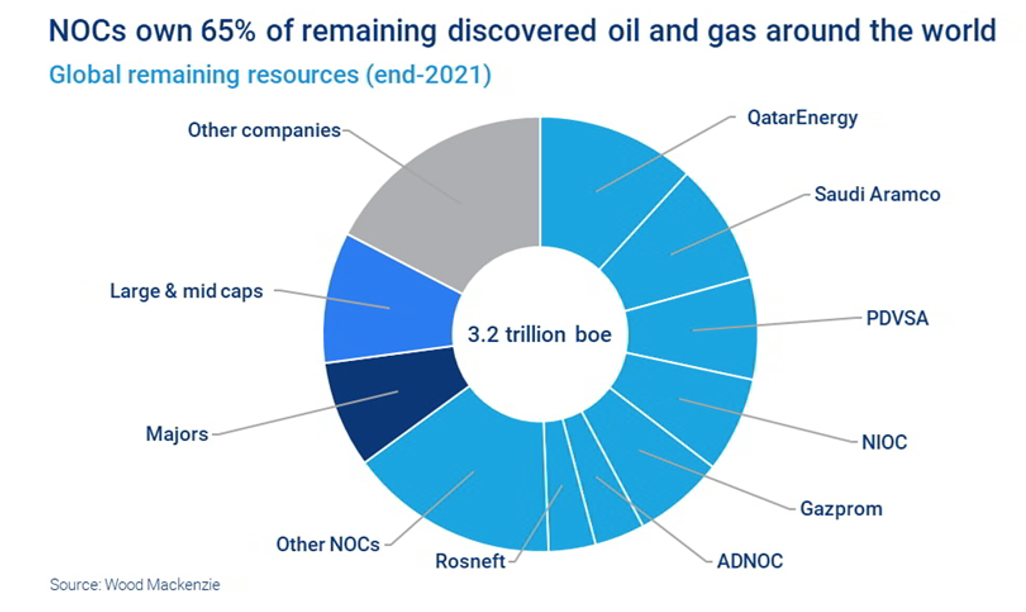

- A high proportion of reserves, especially oil and gas, are state controlled. National oil companies control around 65 percent of oil and gas reserves globally. Increasing resource nationalism means that concerns (ensuring domestic energy sufficiency as well as increasing royalty and tax revenues) and geo-politics may affect accessibility and costs.

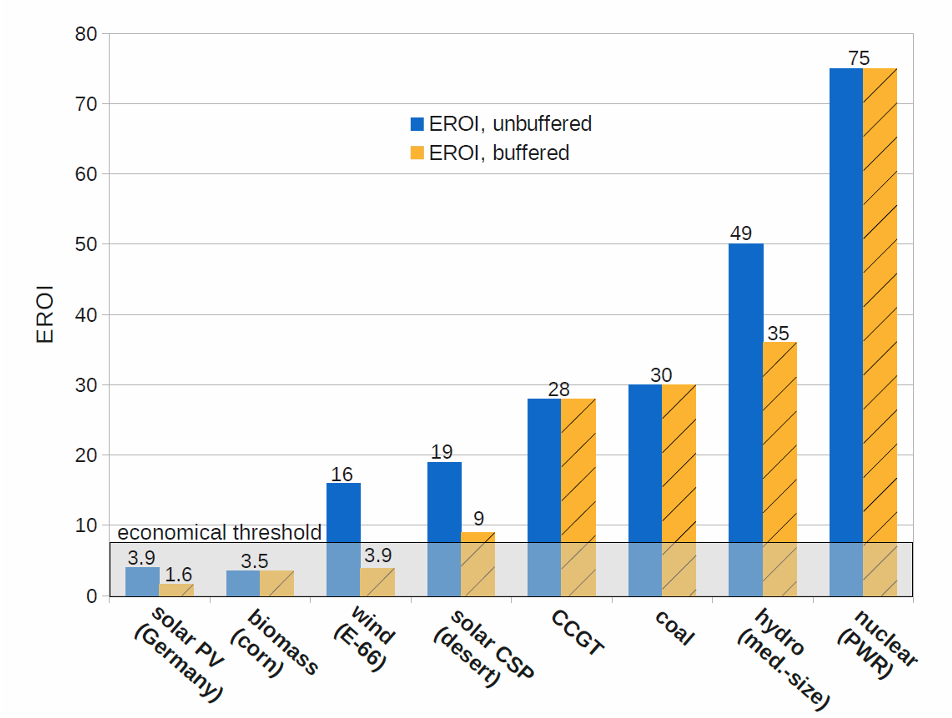

EROEI

A critical element of energy physics is the concept of EROEI (Energy Return On Energy Invested). This is the ratio of the amount of usable energy (the exergy) delivered from a particular energy resource to the amount of exergy used to obtain that energy resource calculated as:

Energy Delivered/ Energy Required to Deliver that Energy

There are two types of EROEI:

- Buffered – which includes storage.

- Unbuffered – which excludes storage.

The differentiation allows capture of the problems of intermittent renewable energy sources. The need for storage will generally lower the buffered EROEI.

Although widely accepted, measurement present problems. While the total energy output is readily measurable, accurate determination of energy input is more difficult. The principal question is capturing the full energy use of the supply chains; for example, the energy input into materials like steel or other materials needs to generate energy. A complete accounting would also necessitate incorporating opportunity costs and comparing total energy expenditures in the presence and absence of this economic activity.

In practice, 3 different EROEI calculations are used:

- Point of Use EROI – which expands the calculation to include the cost of refining and transporting the fuel.

- Extended EROI – which includes point of use and also the cost of creating the infrastructure needed for transportation of the energy or fuel once refined.

- Societal EROI – a sum of all the EROIs of all the fuels used in a society or nation which may be practically impossible due to the number of variables that must be captured.

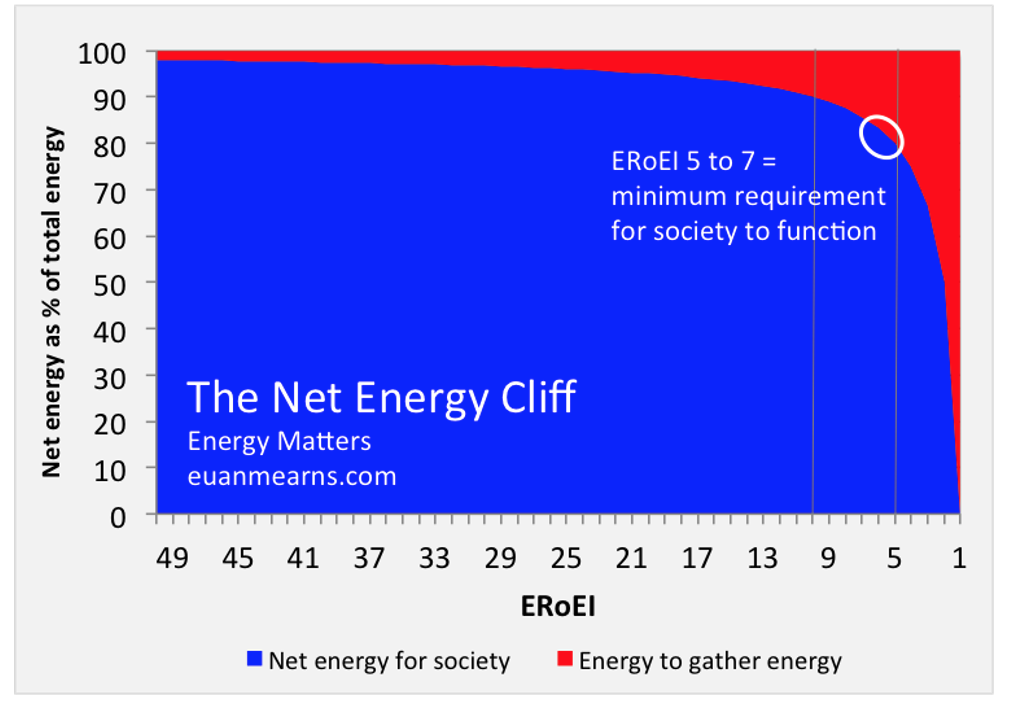

When the EROEI of a source of energy is less than or equal to one, that energy source becomes a net energy sink. While there is considerable debate around the exact number, an EROEI ratio of at least 3:1 (some put it as high as 5 or 7:1) is required for an energy source to be considered a viable fuel or energy source.

Estimates of the EROEI of different energy sources are set out below:

EROEI for a given source is not constant. In the 1930s, the EROEI of oil was probably near 100 reflecting ease of extraction; that is, only 1 percent of the oil being extracted was needed provide the energy necessary to pump and deliver the oil. In the 1950’s the EROEI had decreased to around 30. It is currently around 20, a decline by a factor of five. The EROEI of less accessible sources now being exploited is lower. Offshore drilling has an EROEI of about 5 while Brazil deep-sea Lula resource is lower still and may not be practical to develop. Oil shale has an EROEI of 1.1 to 2.2 but some put it much higher if only purchased energy is counted as input excluding self-energy (internal energy) from the conversion process used to power that operation.

The exhaustion of certain energy sources and the shift to renewables is likely to reduce EROEI of the whole energy system from current 6:1 to between 5:1 to under 3:1 by 2050 depending on the energy mix assumed. The reduction means that in order to satisfy the same level of final net power consumption, the system needs to process more energy and materials to make it available for the society. Currently energy costs around 5 percent of global GDP. As EROEI decreases more of income will need to be directed to energy costs. At 3, this would increase to 15 to 25 percent of GDP.

EROEI analysis highlight a central issue of energy use. Human development has been dependent on the availability coal, oil and gas reserves which can be utilised efficiently due to modest energy or financial investment needs. As the best resources are used up and climate change dictates a shift to less-polluting energy sources, EROEI decreases rapidly (known as the energy cliff). The risk is that EROEI falls below the minimum requirements for modern societies and economies to function.

Energy Pricing

The pricing of energy, especially long term, must be evaluated against a background of rising demand, constraints on supply, especially of traditionally dominant fossil fuels, and declining EROEIs. This does not incorporate important externalities such as the emissions from the use of fossil fuels which are not valued or charged for.

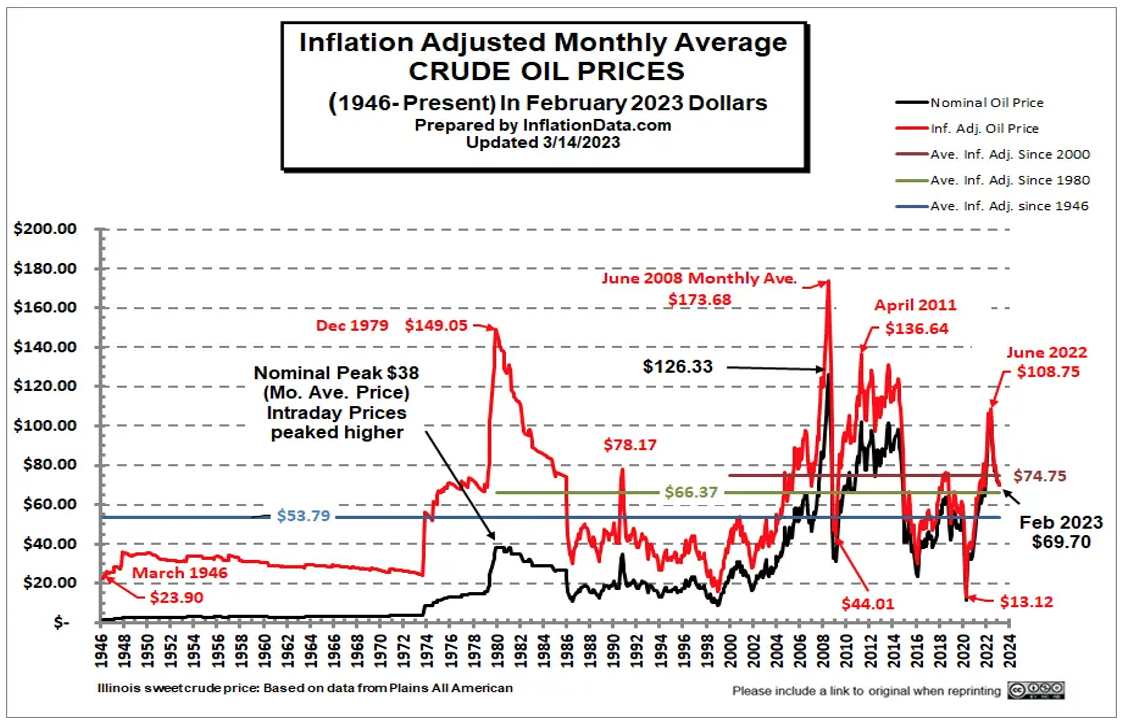

As an example, the real price of oil does not fully reflect the identified factors.

This means that cost of energy will have to increase significantly over the long term. The principal drivers include:

- Inelastic and rising demand, especially from developing economies such as China and India.

- Energy’s essential role in generating global growth and meeting expectations of improving living standards.

- Finite supply of fossil fuels which will remain an essential part of the energy mix due to difficulties of replacing it for some applications.

- Declining EROEI.

- Increasing political instability in energy producing regions.

- Management of energy resources consistent with national objectives and strategic independence.

Short-to-medium run energy prices will remain volatile because of inelasticity of both supply and demand for oil and event risk (a recession in China, or a rapid fall-off in tourism due to terrorist attacks on commercial airliners or pandemics). However, the long-term price dynamics are difficult to overlook.

The supply-demand imbalance may manifest quicker than expected as forward looking markets anticipate the shortfall pushing up prices sharply. For example, Saudi Arabia has warned that, without re-investing in the oil industry to find more deposits, the world could be short 30 million barrels a day within a decade or so. In effect, the price adjustment might take place well before the reserves of fossil fuels are anywhere near exhausted.

Keeping The Lights On

Current and expected demand for energy will progressively outstrip inherently finite fossil fuels. While renewables can bridge some of the deficit, energy physics dictates that less efficient energy sources will replace superior, ignoring emissions, fossil fuels. At a minimum, it will mean more expensive and more limited power. At worst, there might be shortages, especially of fuels needed for specific activities. This will have profound consequences for societies and economies that believe in a birthright of unlimited and cheap energy.

Such shortages are not new. In the mid-nineteenth century, the demand for fuel for lighting exceeded the supply of whale oil leading to higher prices. It also made illumination expensive for ordinary Americans meaning only the affluent could afford to light their homes regularly. Ironically, it was the discovery of oil in Western Pennsylvania that alleviated the shortfall.

The energy assumptions which have underpinned economic models and expectations, with the benefit of hindsight, were unwise. As poet Robert Frost mused in The Road Not Taken “way leads to way”. Choices made over centuries may be difficult to change or, in some case, irreversible. It is unlikely that our civilisation can go back, at least not without a major dislocation.