Wall Street’s in an unusually bullish mood Tuesday morning.

Tim Holland, chief investment officer at Orion Advisor Solutions, argues the market has just notched two peaks. Last week, the Labor Department finally reported an ever-so-slight decline in inflation, as a measure of individual investor sentiment showed the greatest percent of individual investors that were bearish since 2009.

“If we have seen peak inflation and peak investor pessimism the path forward for the market should be much more constructive,” said Holland.

Not everyone’s convinced. Credit Suisse’s London-based global strategy team have been cautious on stocks since February — and they still are. They say recession risk remains very high and there isn’t upside on their fair value models. Importantly, the risk to corporate earnings remains high.

“Earnings revisions have started to fall and 71% of the time when this happens, markets fall over the next quarter. Current PMIs imply significant further downside to revisions. We see clear risk of negative EPS in 2023,” said strategists led by Andrew Garthwaite.

Sure, markets have bottomed after a roughly 19.5% drop from their peak — the intraday low on the S&P 500 SPX, -0.39% that was reached last Thursday — but on three of those four occasions, the Fed was easing.

For the Credit Suisse team to turn bullish, it would take, more or less, clear signs that Fed hikes are restraining the economy.

“What do we need to see to be more constructive? Clear signs of U.S. wage growth slowing, U.S. lead indicators falling sharply indicating that the Fed needs to do less to get unemployment rising above full employment, signs of a new paradigm showing that margins can stay high even as nominal GDP slows by [8 percentage points], clear cut undervaluation on [equity risk premium] model, or credit spreads discounting a recession,” Garthwaite and the team said.

The buzz

Hong Kong-listed stocks including JD.com JD, -0.04%, Alibaba BABA, -1.72% and NetEase NTES, +0.85% surged as Shanghai set plans to reopen from its strict lockdown, including a full reopening by June 1. JPMorgan also upgraded a bunch of U.S.-listed China tech stocks on Monday.

Elon Musk — over Twitter, of course — said that his offer for the social-media service TWTR, -8.18% cannot move forward until the company provides more details on the proportion of spam accounts. CEO Parag Agrawal says he’s confident that spam accounts represent less than 5% of the user base, and the company said it was ‘committed to completing’ the $54.20-a-share deal in a proxy statement. Separately, Musk may be selling shares in SpaceX to help fund the bid, the New York Post reported.

It’s a big day on the retail front, as Home Depot HD, -0.01% reported a surprise rise in same-store sales growth, but Walmart WMT, +0.11% shares are getting hit by an earnings miss and outlook cut. The April retail sales report is expected to show an acceleration in spending, driven by auto sales. Industrial production and a homebuilder sentiment report also are due for release.

Federal Reserve Chair Jerome Powell is due at 2 p.m. Eastern to appear at The Wall Street Journal’s Future of Everything Festival. A slew of regional Fed presidents, from the hawkish James Bullard to the dovish Neel Kashkari, also are due to speak.

See interviews with Powell, the CEOs of companies including Wells Fargo, Moderna and FanDuel. Register for virtual access to The Wall Street Journal’s Future of Everything Festival, May 17-19. (Select virtual pass for complimentary access.)

A wave of 13-F reports from top shareholders were filed at the Securities and Exchange Commission. Berkshire Hathaway revealed new stakes in Citigroup C, -0.38%, Paramount Global PARA, -1.16% and Celanese CE, +1.52%, among others. Chase Coleman’s Tiger Global Management, which has struggled this year, boosted stakes in several tech plays including CrowdStrike Holdings CRWD, -6.33%, Sea SE, -6.72%, Snowflake SNOW, -8.75%, ServiceNow NOW, -4.36% and Carvana CVNA, +0.23%.

The markets

Markets seem to be flying higher, as U.S. stock futures ES00, +1.55% NQ00, +1.89% rose and the dollar DXY, -0.63% fell. Treasury yields TY00, -0.34% TMUBMUSD02Y, 2.632% are also climbing.

Top tickers

Here were the most active stock-market tickers as of 6 a.m. Eastern.

| Ticker | Security name |

| TSLA, -5.88% | Tesla |

| GME, -6.70% | GameStop |

| AMC, -0.85% | AMC Entertainment |

| TWTR, -8.18% | |

| NIO, +1.68% | Nio |

| AAPL, -1.07% | Apple |

| MULN, +18.28% | Mullen Automotive |

| AMZN, -1.99% | Amazon.com |

| BABA, -1.72% | Alibaba |

| NVDA, -2.50% | Nvidia |

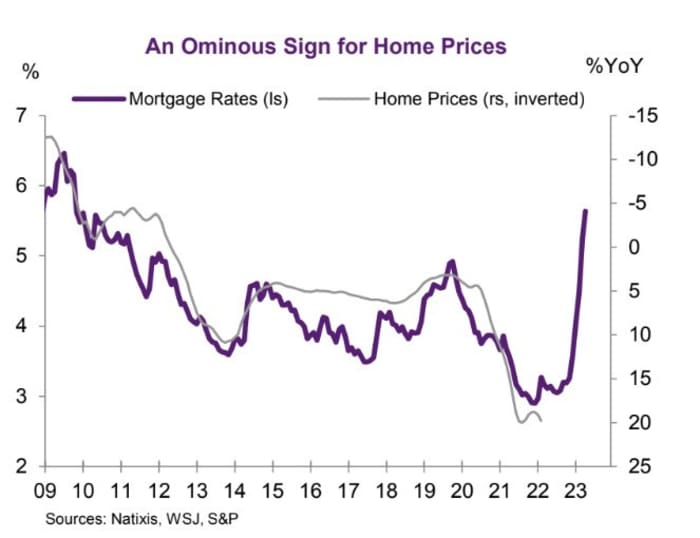

The chart

Correlation doesn’t mean causation, and dual Y-axis charts can be manipulated to show closer correlations. So with all those caveats in mind, U.S. economists at Natixis point the close correlation between mortgage rates and house prices, which points to a perhaps sharp wealth effect risk.

They do point out, however, that the steepness of the home price slowdown might not be as sharp as the chart would suggest, owing to the national housing deficit of both the pandeic housing boom and ongoing supply chain issues. A mid single digit correction in house prices over the next year “is entirely reasonable.”

Random reads

The U.S. military is throwing around $50,000 bonuses to recruits, because of the pay at companies like Target and Starbucks.

How Shanghai residents have employed Excel to navigate the lockdown.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.