Target on Wednesday reported a 52% drop in profit for the first quarter, missing Wall Street’s forecasts and triggering a broad market selloff.

Joe Raedle/Getty Images

Worse-than-expected earnings reports from the biggest publicly traded U.S. companies are set to become yet another “shock” for investors struggling to overcome stagflation fears.

That’s the view of Capital Economics’ Thomas Mathews, who says the S&P 500 index Index can easily hit a trough of 3,750, and probably lower, on more bad earnings news. As of Thursday afternoon, the S&P 500 SPX, -0.28% was up less than 0.1% at 3,927, a day after posting its biggest one-day decline since June 11, 2020. A finish below 3,837.25 would mark the technical definition of a bear market, according to Dow Jones Market Data.

Read: Despite bounce, S&P 500 hovers close to bear market. Here’s the number that counts

Wednesday’s brutal stocks selloff seemed to mark a turnabout of thinking in the markets, as cracks appeared in the earnings results of big-name retailer Target Corp. TGT, -4.80% following a profit miss by Walmart Inc. WMT, -2.46% the prior day —- a sign that higher inflation is seeping into just about every corner of the U.S. economy. For the past year, investors, traders and professional forecasters have all stayed optimistic that inflation will eventually subside. Markets have yet to price in a worst-case scenario for the economy, in which inflation fails to come down and/or the U.S. falls into recession, analysts said.

“The whole economy is being affected through this robust inflation we’re seeing and I don’t see any type of resolution until equity prices start reflecting lower GDP and lower earning growth,’’ said Tom di Galoma, a Treasurys trader at Seaport Global Holdings in Greenwich, Connecticut.

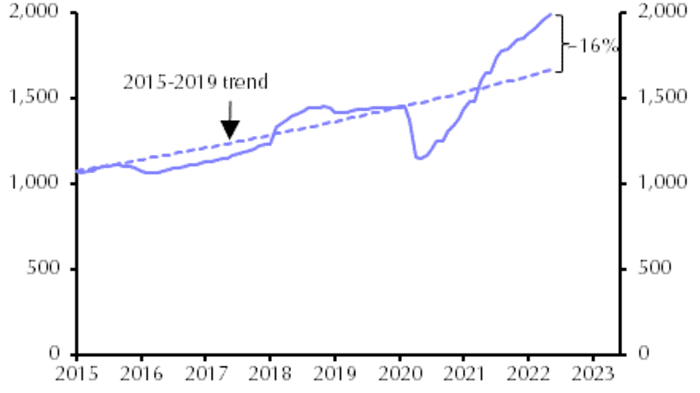

Though the S&P 500 is on the verge of entering a bear market, earnings expectations remain positive, Capital Economics’ Mathews wrote in a note on Thursday. Analysts have been expecting almost double-digit earnings growth for companies in the index, on average, over the next couple of years, he said. And 12-month forward earnings expectations for S&P 500 companies remain around 16% higher than their prepandemic trend, according to the markets economist.

Source: Refinitiv, Capital Economics

With the index having fallen 4% in a single day on Wednesday, “earnings are definitely a shock facing the S&P 500,” Mathews wrote in an email to MarketWatch. “And earnings expectations still seem really upbeat, which suggests there’s potential for a lot more to come on that front.”

Further bad earnings news could push the S&P 500 to as low as 3,750, but even that might be too optimistic, according to Mathews. In the event of a recession, it “wouldn’t be out of the question” for the index to fall 20% from here, based on historical experience.

Refinitiv’s S&P 500 Earnings Scorecard, released last Friday, shows that there have been 55 negative earnings-per-share preannouncements issued by S&P 500 corporations for the second quarter. That compares with 28 which have been positive.

Below is a rundown of risks facing markets:

Inflation

Inflation sits at the top of the list of shocks percolating through the financial system right now.

One big reason is that the U.S. —- which saw an 8.3% annual headline rate in April’s consumer-price index report, still near a 40-year high — may not be past the peak of price gains. Disruptions from China’s zero-tolerance policy on COVID-19 and Russia’s war on Ukraine have yet to fully show up in the data, and traders are expecting five more months of 8%-plus readings.

Read: Next big shoe to drop in financial markets: Inflation that fails to respond to Fed rate hikes

‘Growth Scare’

Wednesday’s brutal selloff in equities —- which sent Dow the industrials down by 1,164.52 points and left the Dow, like the S&P 500, nursing its worst daily drop in almost two years —- had a distinctly different flavor than past selloffs.

The latest leg down “had all the hallmarks of a growth scare,” Mathews wrote in his note. Bonds rallied as investors unwound bets for rate hikes, safe-haven currencies strengthened, and stocks sold off across the board.

By comparison, the factors behind most of this year’s fall in equity prices were mostly tied to rising “safe” asset yields as investors absorbed the Fed’s hawkish pivot, he said.

As of this week, U.S. and euro-area stock markets appeared to be pricing in around a 70% chance of a near-term recession, based on an estimate from JPMorgan Chase & Co.’s Marko Kolanovic and others. In their view, that’s “too much recession risk.”

Still, one underappreciated risk is how swiftly financial and economic conditions could deteriorate in the current environment. Seaport’s di Galoma expects the U.S. to fall into recession by early 2023, though the arrival time is “accelerating and going to come a lot quicker than people think.” “It’s right on our doorsteps and I think this recession will be quite deep,’’ di Galoma said via phone on Thursday.

Higher interest rates

The Federal Reserve is still poised to keep tightening financial conditions, with a reduction of its almost $9 trillion balance sheet starting next month and policy makers set to deliver two more 50 basis point rate hikes in June and July. Monetary policy alone is another “key shock,” albeit one that’s been going on for a while, and weighs on earnings multiples, said Mathews of Capital Economics.

Investors have even tried to overlook the impact of rising rates, such as on May 4 when Fed Chairman Jerome Powell told reporters that a 75 basis point rate hike wasn’t actively being considered. Stock market investors cheered the remark, but lost enthusiasm the very next day —- with a more than 1,000-point drop in the Dow Jones Industrial Average DJIA, -0.51% on May 5.

Russia, Ukraine and China

Russia’s war on Ukraine, which continues to rage after almost three months, “still has the potential to cause significant commodity price volatility, which could affect the outlook both for earnings and for monetary policy (by boosting or cooling inflation),” Mathews said.

Moreover, China’s COVID-19 lockdowns are rippling around the world, putting a damper on global-growth prospects, and aggravating inflation pressures because of the Asian country’s role as a manufacturing powerhouse and source of many of the world’s goods.

“The confluence of events (inflation and the impact of policy responses to address it, the war, China’s zero-COVID policy and broader supply concerns) may mean volatility persists in the near term as we get more information on progress made on each,” Andrew Patterson, a senior international economist at The Vanguard Group, said in an email to MarketWatch.

Cryptocurrency

Last week’s crash of the stablecoin TerraUSD is raising concern in a few corners of the market that stablecoins as a whole could destabilize and trigger a systemic risk.

That’s the case even though Treasury Secretary Janet Yellen has tried to dispel the notion of a threat to financial stability, though she’s also acknowledged the risks. Still, regulators are worried and, at the very least, market participants may question whether more idiosyncratic runs on stablecoins are in store, if there’s contagion risks, and what the implications might be on broader money markets.