by confoundedinterest17

The Federal Reserve has been signaling a tightening of its loose monetary policy (essentially loose since the housing bubble burst of 2008 and the ensuing financial crisis). It is still loose as The Fed hasn’t really trimmed its massive balance sheet yet and has just raised it target rate to 1%.

So, potential home owners have to pay 5.10% for a 30-year fixed-rate mortgage while the effective Fed Funds rate, the rate at which banks lend to each other, is a measly 0.83%. This puts consumers at a relative disadvantage to large Wall Street firms that are gobbling up houses at an accelerated rate.

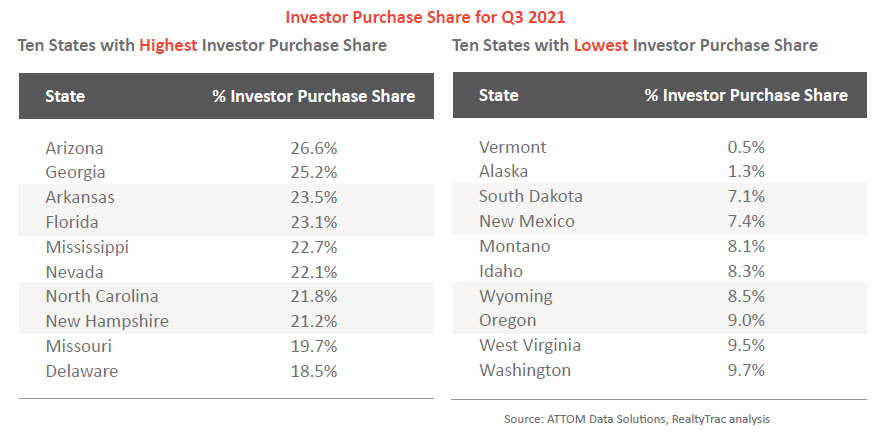

RealtyTrac has a Attom-sourced table of investor purchases of housing from Q3 2021, before The Fed started helping to crank-up mortgage rates for consumers.

With the US housing market slowing (thanks to The Fed’s signaling of monetary tightening), the question now is how far will The Fed go in its “War on Inflation!”?

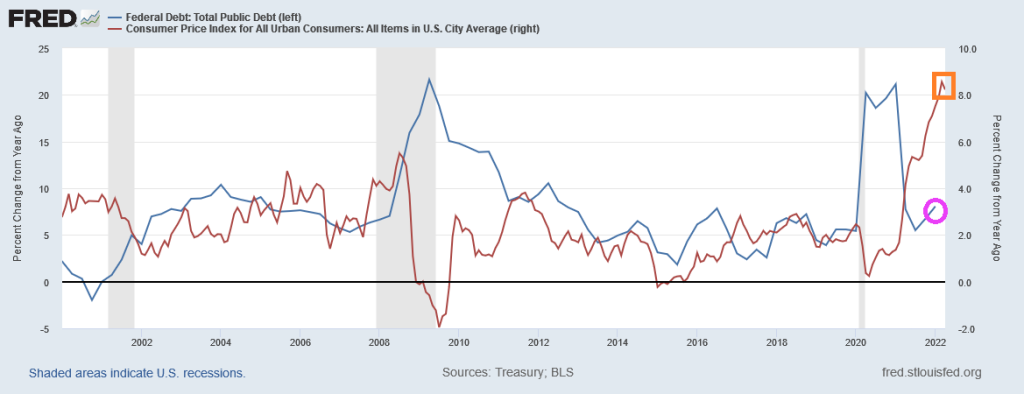

You can see a major cause of inflation in the US since 2000: Federal spending and Federal (public) debt. During The Great Recession of 2008-2009, we saw inflation (CPI YoY) collapse into negative territory as Federal spending and debt soared. But the mini-recession of 2020 caused by the Covid governments shutdowns led to TWO surges in Federal spending and debt: Covid relief followed by the infrastructure spending bill. Combined with Biden’s anti-fossil fuel executive orders and massive splash of Federal spending in to the economy, we have inflation soaring.

If surges in Federal spending (requiring surges in Federal debt) have gone away (except for $40 billion in Ukrainian relief and Biden’s possible student loan cancellation of $10,000 that will cost an estimated $321 billion … and help drive up college tuitions even further), we may be over the “twin gorgings” of the Covid spending spree. This alone may result is a decline in the inflation rate.

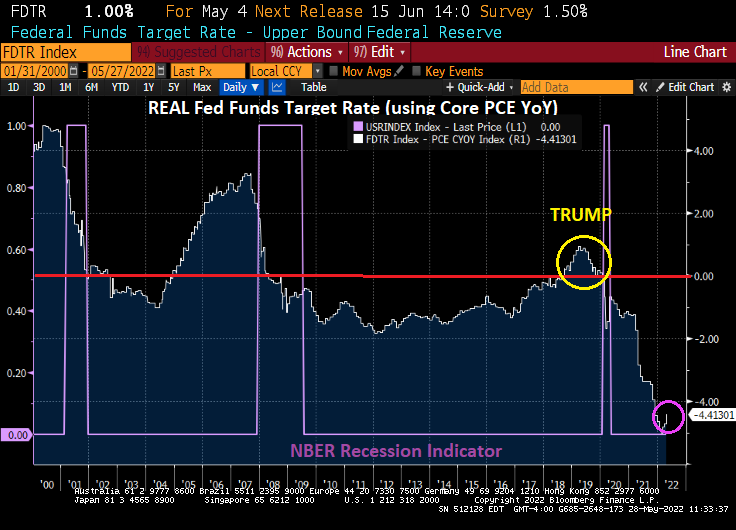

Where do we sit today with the REAL neutral rate? The REAL Fed Funds Target Rate (upper bound) is -4.41%. It was in positive territory during the Trump years. But then Covid struck.

So, we sit here today with Fed Monetary policy “loose as a goose.” And Wall Street investors “drunk as a skunk” on Fed Stimulus.

No wonder Wall Streeters like to go

Trending:

Views: 5