Yves here. The Trump executive order of March 26, mandating a near-total end of the use of checks by the Treasury Department, including for receipt of tax payments by September 30, has gotten little attention in the flurry of other Trump actions.

This is yet another example of the saying attributed to that great American philosopher, Yogi Berra: “In theory, there is no difference between theory and practice. In practice, there is.”

In theory, it’s a good idea to get rid of checks, at least if you are in the habit of processing a lot of them. There’s an arguable secondary benefit to consumers, since check fraud has allegedly increased in recent years.

However, an article in PMTS describes in gory detail that no way, no how can Treasury achieve this goal by September 30. In fact, given the intractability of the underlying payment processor systems, one wonders how many years it will take for the Feds to realize any net savings from this initiative. $650 million to process checks across all Treasury expenditures and receipts is couch lint.

And this change-over is going to be made more difficult given the DOGE obsession with firing Federal employees.

We’ll later turn to the question of the potential for more costs to consumers for payment processing.

I wish I could embed the 18 minute video from the PMTS site. Its writeup does not fully capture the bemused dismissiveness of Ingo Payments CEO Drew Edward, who has apparently spoken directly to the IRS from time to time about these issues. From PMTS:

As Ingo Payments CEO Drew Edwards pointed out in conversation with Karen Webster recently, the bigger problem runs deeper than the paper check’s stubborn persistence. Edwards contended the real issue is that the treasury simply does not have the digital data required to make instant, accurate electronic payments to millions of Americans by the Sept. 30 mandated end of paper checks….

The executive order’s goal of modernizing the system is hindered by a data deficit. Edwards cited the Internal Revenue Service (IRS) as one of many federal agencies working from outdated frameworks that lean on physical addresses rather than digital identifiers…

Traditionally, Edwards noted, the treasury has either mailed out paper checks or processed direct deposits via Automated Clearing House (ACH) files — both reliant on data the IRS gathers through tax returns. While some taxpayers opt to enter routing and account numbers for direct deposit, large swaths of recipients continue to receive treasury checks by mail. And if the government aims to eliminate checks entirely, it must update everything from how it collects consumer information to how it verifies recipients’ identities.

“The biggest challenge is how do they get contact information from everybody that’s receiving money from the federal government other than that name and address,” Edwards explained. “Then how do you make sure the contact you have is actually the person you think it is?”

Authentication Issues

Even if authorities identify a viable digital payment system, Edwards warned that the next obstacle lies in ensuring secure, authenticated transactions. In other sectors — such as insurance, where Ingo Money works with firms to shift from checks to digital payments — companies often tap into non-public data to confirm an individual’s identity. With government agencies disbursing everything from tax refunds to veterans’ benefits, the verification puzzle becomes even more complex.

Additionally, many Americans neither have established relationships with traditional financial institutions nor keep a standard checking account. Others use digital-first services — PayPal, Cash App, Chime — as their primary “banking” relationship. That lack of uniformity makes a one-size-fits-all approach unworkable. Edwards stressed the government should recognize consumer preferences and extend multiple digital payment options….

But fraud isn’t limited to paper. Transitioning to digital payment rails, especially those promising faster or real-time transfers, poses its own risks, he said. A direct deposit can be instantly final, leaving the government with fewer levers to pull if the payment was made in error or under fraudulent pretenses.

For my corporate tax deposits, the IRS makes what I believe is an ACH debit at no charge to me. This is not the case for retail customers who use debit or credit cards:

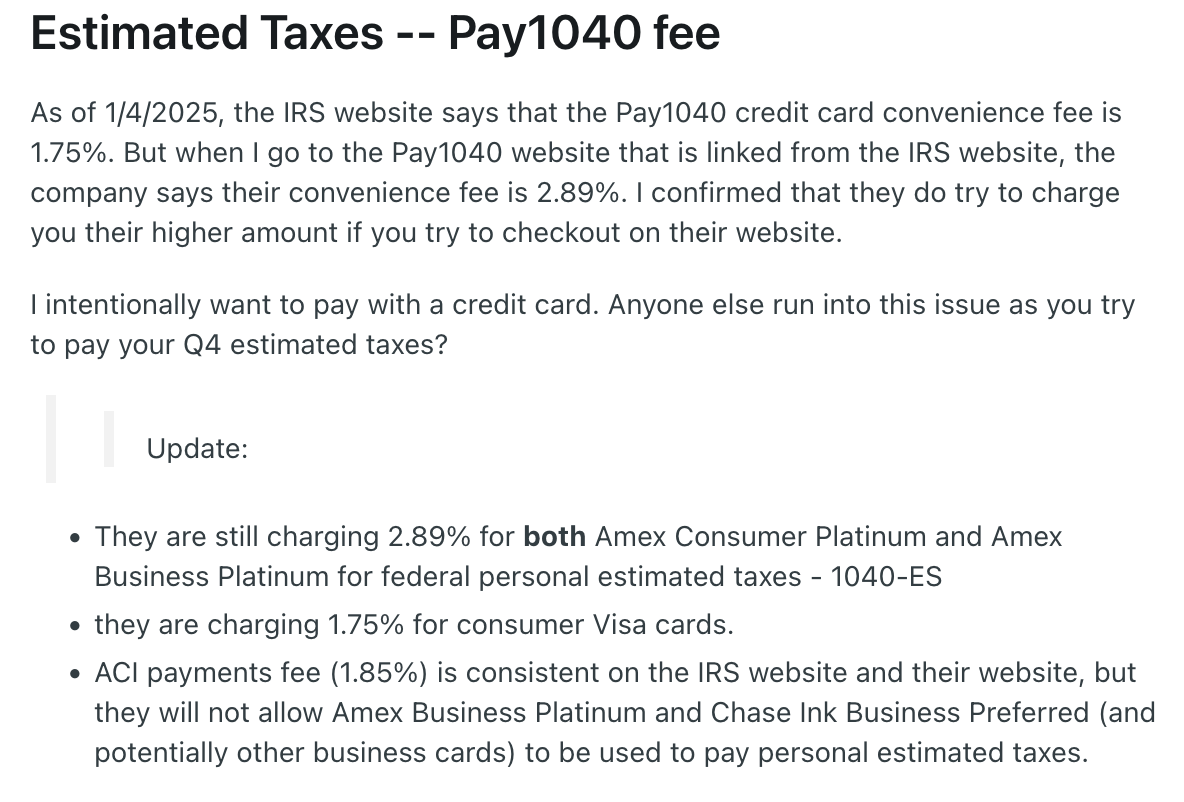

A recent complaint on Reddit confirms the “convenience fees” are not chump change:

Needless to say, this will be more of a moving target than Team Trump pretends. Stay tuned.

_________

Text of Executive Order, Modernizing Payments To and From America’s Bank Account. Attentive reader may notice that it includes vague language that could include accepting crypto: “digital wallets and real-time payment systems,” and “other modern electronic payment options.”

Perhaps “digital wallets” stands for PayPal and “real-time payment systems,” “Zelle”. But if “other modern electronic payment options” means crypto, good luck with that. Treasury is going to find it very hard to get rid of checks. Pray tell, how will it value all these crypto, let alone connect to every more idiosyncratic wallet providers?

By the authority vested in me as President by the Constitution and the laws of the United States of America, it is hereby ordered:

Section 1. Purpose. The continued use of paper-based payments by the Federal Government, including checks and money orders, flowing into and out of the United States General Fund, which might be thought of as America’s bank account, imposes unnecessary costs; delays; and risks of fraud, lost payments, theft, and inefficiencies. Mail theft complaints have increased substantially since the COVID-19 pandemic. Historically, Department of the Treasury checks are 16 times more likely to be reported lost or stolen, returned undeliverable, or altered than an electronic funds transfer (EFT). Maintaining the physical infrastructure and specialized technology for digitizing paper records cost the American taxpayer over $657 million in Fiscal Year 2024 alone.

This order promotes operational efficiency by mandating the transition to electronic payments for all Federal disbursements and receipts by digitizing payments to the extent permissible under applicable law (but not, for avoidance of doubt, to establish a Central Bank Digital Currency).

Sec. 2. Policy. It is the policy of the United States to defend against financial fraud and improper payments, increase efficiency, reduce costs, and enhance the security of Federal payments.

Sec. 3. Phase Out of Paper Check Disbursements and Receipts. (a) Effective September 30, 2025, and to the extent permitted by law, the Secretary of the Treasury shall cease issuing paper checks for all Federal disbursements inclusive of intragovernmental payments, benefits payments, vendor payments, and tax refunds, except as specified in section 4 of this order.

(b) All executive departments and agencies (agencies) shall comply with this directive by transitioning to EFT methods, including direct deposit, prepaid card accounts, and other digital payment options, and take all steps necessary to enroll recipients in EFT payments, except as specified in section 4 of this order.

(c) As soon as practicable, and to the extent permitted by law, all payments made to the Federal Government shall be processed electronically, except as specified in section 4 of this order.

(d) The Secretary of State, the Secretary of the Treasury, the Secretary of Health and Human Services, the Secretary of Education, the Secretary of Veterans Affairs, and the Secretary of Homeland Security shall take appropriate action to eliminate the need for the Department of the Treasury’s physical lockbox services and expedite requirements to receive the payment of Federal receipts, including fees, fines, loans, and taxes, through electronic means except as specified in section 4 of this order.

(e) The Secretary of the Treasury shall support agencies’ transition to digital payment methods, including by providing access through the Department of the Treasury’s centralized payment systems to:

(i) direct deposits;

(ii) debit and credit card payments;

(iii) digital wallets and real-time payment systems; and

(iv) other modern electronic payment options.

Sec. 4. Exceptions and Accommodations for the Phase Out of Paper Check Disbursements and Receipts. (a) The Secretary of the Treasury, shall review and, as appropriate, revise procedures for granting limited exceptions where electronic payment and collection methods are not feasible, including exceptions for:

(i) individuals who do not have access to banking services or electronic payment systems;

(ii) certain emergency payments where electronic disbursement would cause undue hardship, as contemplated in 31 C.F.R. Part 208;

(iii) national security- or law enforcement-related activities where non-EFT transactions are necessary or desirable; and

(iv) other circumstances as determined by the Secretary of the Treasury, as reflected in regulations or other guidance.

(b) Individuals or entities qualifying for an exception under this section or other applicable law shall be provided alternative payment options.

Sec. 5. Implementation and Compliance of Electronic Transactions. (a) The Secretary of the Treasury, in coordination with the heads of agencies, shall develop and implement a comprehensive public awareness campaign to inform Federal payment recipients of the transition to electronic payments, including guidance on accessing and setting up digital payment options.

(b) Agencies shall coordinate with the Department of the Treasury to facilitate a smooth transition to digital payments, ensuring that affected individuals and entities receive adequate support.

(c) The Secretary of the Treasury shall work with financial institutions, consumer groups, and other stakeholders to address financial access for unbanked and underbanked populations.

(d) The Secretary of the Treasury and the heads of agencies shall take all necessary steps to protect classified information and systems, as well as personally identifiable information and tax return information, through the implementation of this order.

Sec. 6. Reporting Requirements. (a) The heads of agencies shall submit a compliance plan to the Director of the Office of Management and Budget within 90 days of the date of this order detailing their strategy for eliminating paper-based transactions.

(b) The Secretary of the Treasury shall submit an implementation report to the President through the Assistant to the President for Economic Policy within 180 days of the date of this order detailing progress on the matters set forth in this order.

Sec. 7. General Provisions. (a) Nothing in this order shall be construed to impair or otherwise affect:

(i) the authority granted by law to an executive department or agency, or the head thereof; or

(ii) the functions of the Director of the Office of Management and Budget relating to budgetary, administrative, or legislative proposals.

(b) This order shall be implemented consistent with applicable law and subject to the availability of appropriations.

(c) This order is not intended to, and does not, create any right or benefit, substantive or procedural, enforceable at law or in equity by any party against the United States, its departments, agencies, or entities, its officers, employees, or agents, or any other person.