This is Naked Capitalism fundraising week. 615 donors have already invested in our efforts to combat corruption and predatory conduct, particularly in the financial realm. Please join us and participate via our donation page, which shows how to give via check, credit card, debit card or PayPal or our new payment processor, Clover. Read about why we’re doing this fundraiser, what we’ve accomplished in the last year,, and our current goal, continuing our expanded news coverage.

By Wolf Richter, editor of Wolf Street. Originally published at Wolf Street.

“Unrealized losses” are paper losses on securities that banks hold, but via a quirk in bank regulations, they don’t have to mark them to market value, but can carry them at purchase price.

On one level, it makes sense.

The closer the bonds get to the maturity date, the closer the market value gets to face value, and the unrealized losses vanish, and on the day the bonds mature, the banks get paid face value, and there are no losses, and everyone smiles.

On another level, the bank collapses.

During a bank run, when scared uninsured depositors yank their money out, banks have to sell assets to cover their cash outflows from the run. But now the banks only get market value for those securities – if that, during a fire sale – and not their original purchase price, and they have huge losses on those sales that vaporize their capital. No cash, no capital, no problem? Big problem.

That’s why we now have to pay attention to unrealized losses in the banking system.

Banks can hedge against rising interest rates, but some banks prefer to collapse.

Hedges against the risk of rising interest rates, such as interest-rate swaps, can be costly, and some banks don’t hedge, or don’t hedge enough, because executives prefer to show a little extra income to prop up the banks falling stock price and to fatten up their compensation.

SVB terminated or let expire nearly all its remaining interest-rate hedges in 2022, to where by the end of 2022, they were nearly all gone, and three months later it collapsed.

Where are banks now? Unrealized losses rise by 8% to $558 billion.

The balance of unrealized losses on securities – mostly Treasury securities and government-guaranteed mortgage-backed securities – at FDIC-insured commercial banks rose by $43 billion, or by 8%, to $558 billion in Q2, after two months of declines, according to the FDIC’s bank data on Thursday.

This $558 billion is the cumulative loss balance over time on all securities. The balance rose because longer-term yields rose in Q2: The 10-year Treasury yield rose to 3.84% on June 30, from 3.47% on March 31, and so bond prices fell over the period.

In the free-money periods, when yields fell and bond prices rose, banks had “unrealized gains” (green). And in the periods when yields rose and prices fell, banks had “unrealized losses” (red).

These unrealized losses of $558 billion were spread over two categories of bank accounting treatments:

- Unrealized losses on held-to-maturity (HTM) securities: $309.6 billion

- Unrealized losses on available-for-sale (AFS) securities: $248.9 billion.

The balance of unrealized losses is down by $131 billion from the peak in Q3 2022, in part because three banks with big unrealized losses collapsed, and their balance sheets vanished from the system, with losses getting transferred to the FDIC.

Already gotten worse in Q3 so far.

Thing is, today, the 10-year yield closed at 4.27%, and if it’s still at 4.27% at the end of September, it would be another 43 basis points higher than at the end of Q2, and the balance of unrealized losses will be higher yet again.

Bad-case scenarios: How big can the losses be on specific bonds?

A bank that bought $1 million of 10-year T-notes at the Treasury auction on August 12, 2020, at the very tippy-top of the 40-year bond bull market, ended up with a security that paid a coupon interest rate of 0.625% per year. Today, this security has seven more years to run before maturity, and so trades like a 7-year Treasury security, and the 7-year yield today in the market is 4.35%.

So how much is a security worth today with a coupon of 0.625% per year and with seven years to maturity, when the equivalent market yield is 4.35%?

Roughly, that $1,000,000 in 10-year T-notes might be worth $778,000 in the market today – thank you, bond-price calculator. Results may vary.

The bank that purchased this security at auction and carries it under HTM accounting rules on its books would show no loss on its income statement, and its earnings-per-share would be just fine, and it would pay its executives big-fat bonuses.

But on its balance sheet way down somewhere in the footnotes, it would show an “unrealized loss” of roughly $222,000, or roughly 22.2% of the purchase price.

And that $1,000,000 in 30-year T-bonds that a hapless bank bought at auction in August 2022, with a coupon of 1.375% might sell for about $529,000 today, for a loss of about $471,000, or 47%. That’s about the worst-case scenario, the punishment for buying at the peak of the 40-year bond bull market.

Uninsured depositors figured out where to look.

SVB, in its final quarterly report as a living bank for Q4 2022, in a footnote on page 125, disclosed unrealized losses of $15.2 billion on its HTM securities and unrealized losses of $2.5 billion on its AFS securities, for a total of $17.7 billion in unrealized losses.

The $15.2 billion in unrealized losses on its HTM bonds amounted to 16.7% of the carrying value of $91 billion of its HTM bonds.

Once uninsured depositors, some with billions on deposit at the bank, figured out where to look, they started yanking their money out, and SVB collapsed.

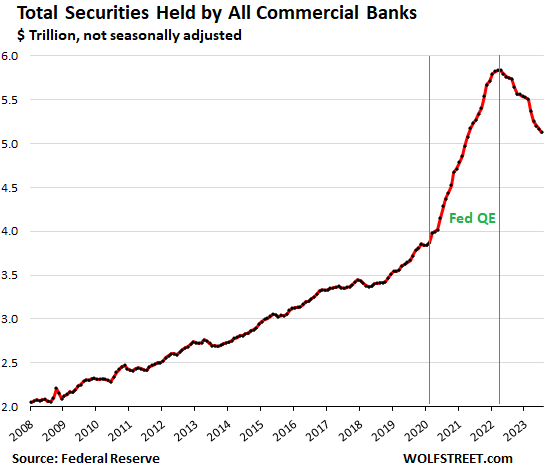

The declining pile of securities held by commercial banks.

The total balance of securities held by all commercial banks has been declining for 16 months in a row to $5.13 trillion in July, down by 10% or by $705 billion, from the peak in March 2022 ($5.84 trillion) when the Fed’s rate hikes began.

Several factors make up the $705 billion decline:

- Securities of the collapsed banks that the FDIC sold to the market (not to other banks) are no longer part of this.

- Banks have written down AFS securities to market value.

- Banks may have sold some securities.

The $558 billion in unrealized losses amount to about 11% of the total securities held by banks.

The chart also shows how banks gorged on these low-yielding securities at the worst possible time just before, during, and after the peak of the 40-year bond bull market – on the ancient strategy of buying high and selling low – as a result of the reckless money-printing by the Fed starting in March 2020 through early 2022. “Free money is a virus that turns investors’ brains to mush” is a well-documented and generally undisputed scientific fact I have been pointing out for a while now.