Yves here. John Helmer looks at the interesting question of which Russian power players are getting first dibs on assets and businesses abandoned or otherwise exited by Western multinationals as a result of sanctions.

Helmer is focusing on big operations, but there are bargains up and down the chain. For instance, international index fund investors and retail investors who didn’t have the presence of mind to exit Russian ETFs when the sanctions were imposed, or used them to make a “blood in the streets” play (at least one reader reported taking such a flier; the ETFs traded a bit after the Moscow stock index trading was halted) have had their positions frozen. You can be sure fund managers like BlackRock, who do deserve the label “unfriendly” will get full fees while the investors, some of whom might have stayed in by virtue of not being hostile, are getting shorn. From Interfax on December 30:

A subcommission of Russia’s Government Commission on Monitoring Foreign Investment has decided to take into account a number of conditions, including a discount of at least 50% of the market value of such assets when issuing permits for the sale of shares, stakes (participation) in the authorized capital of Russian assets by foreign persons from “unfriendly” states. This is according to information in an excerpt from the minutes of the meeting of the subcommission of December 22, published on the Russian Finance Ministry’s website.

By John Helmer, the longest continuously serving foreign correspondent in Russia, and the only western journalist to direct his own bureau independent of single national or commercial ties. Helmer has also been a professor of political science, and an advisor to government heads in Greece, the United States, and Asia. He is the first and only member of a US presidential administration (Jimmy Carter) to establish himself in Russia. Originally published at Dances with Bears

As democracy goes in states at war, in Russia there is more of it — faction fighting, public criticism, media debate — about battlefield operations, wins and losses, than there is on the NATO side, in the US, Canada, Germany, France or England.

By contrast, on the conduct of domestic economic policy, in Russia there is much less open argument than there is on the other side.

This is surprising because the sanctions war has forced the US-controlled and NATO-allied banks and corporations to abandon their Russian business, halt production plants, close offices, cancel supply and marketing agreements, write down the value of their Russian assets, and withdraw from Russia if they can. The outcome is an opportunity, a revolutionary one, for Russia’s businessmen to take over the foreign assets and operate them for domestic profit for the first time in many years.

In theory, there has been active debate in Moscow about how this re-nationalization should be managed, and to whose profit. On one side, there has been Sergei Glazyev and his Anti-Crisis Expert Council which includes the public economist Mikhail Khazin and Duma deputy Mikhail Delyagin. On the other side, the oligarch lobby known as the Russian Union of Industrialists and Entrepreneurs (RUIE), led by Alexander Shokhin.

In practice, Glazyev has kept his government job as minister for integration and macroeconomics of the Eurasian Economic Commission (EEC, aka EAEU ), the bloc of former Soviet states coordinating customs, central banking, trade and fiscal management policies together. However, Glazyev has lost the fights he has waged for change in Central Bank policy and in the priorities of the government’s war economy. Like Glazyev, Khazin and Delyagin have kept their tribunes, but their message has proved unsuccessful.

At the same time, Elvira Nabiullina – Glazyev’s attack target as Governor of the Central Bank – has kept her Kremlin mandate and her policies. Her former patron, Alexei Kudrin, has lost his post at the head of the Accounting Chamber but received Kremlin promotion instead to run the new presidential campaign fund created around the Yandex group of companies, owned by Arkady Volozh.

How much then of the opportunity to convert the foreign-owned assets to new purpose in the Russian economy is being seized by the well-known oligarch faction? What evidence is there for the political defeat of the Glazyev faction? What is the current balance-sheet of foreign assets lost to Russia and Russian assets gained by the US side?

The first attempt to answer these questions was published in May 2022.

Since then, for reasons of war, President Vladimir Putin has stopped serving the Kremlin’s annual Christmas dinner for the oligarchs. Instead, the format was changed and combined with his annual appearance before the RUIE, the meeting with the president was held on February 24; this was just hours after special military operation had begun.

Putin offered reassurance for the oligarchs. He declared his continuing support for “extending the most popular support tools and mechanisms, including corporate programmes for enhancing competitiveness, investment tax deduction and regional investment projects…[and] to provide you with good conditions and ensure more freedom. There may be only one response – to ensure greater freedom of entrepreneurship, naturally, within a certain framework so that, as our colleagues put it, there is a certain amount of predictability from the Government but we expect predictability from businesses as well.”

The RUIE meeting with President Putin, February 24, 2022; source: http://en.kremlin.ru/

For a discussion of the particulars of Putin’s reassurance, Shokhin then met the president in the Kremlin on March 2. The official communiqué said no more than they “spoke at length about ways to minimize the impact of sanctions on major Russian companies.”

Also for reasons of war, this website has suspended publishing the results of its regular investigations of Russians under sanctions.

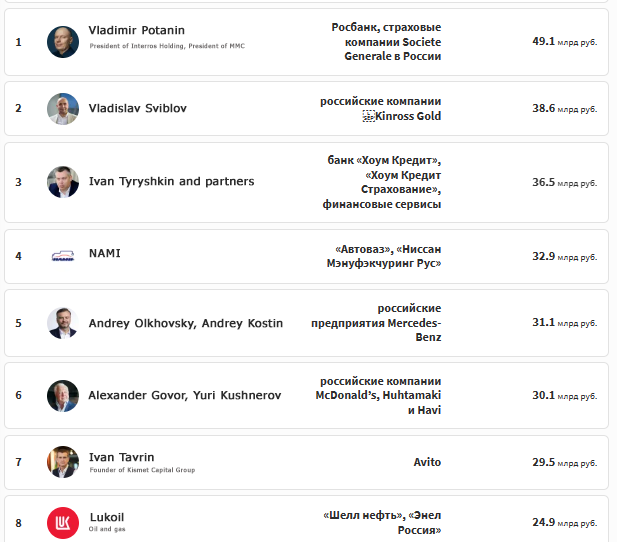

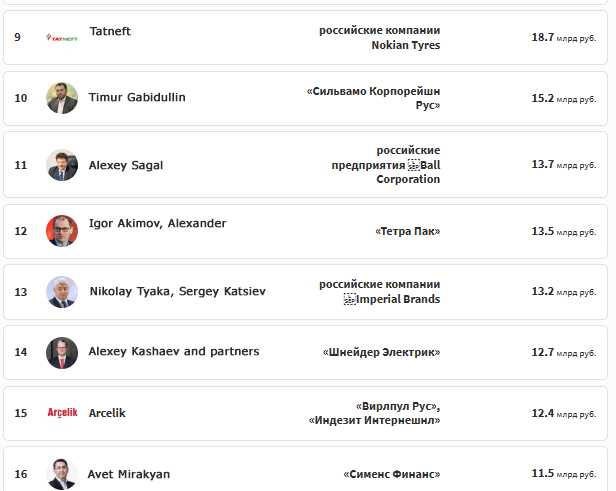

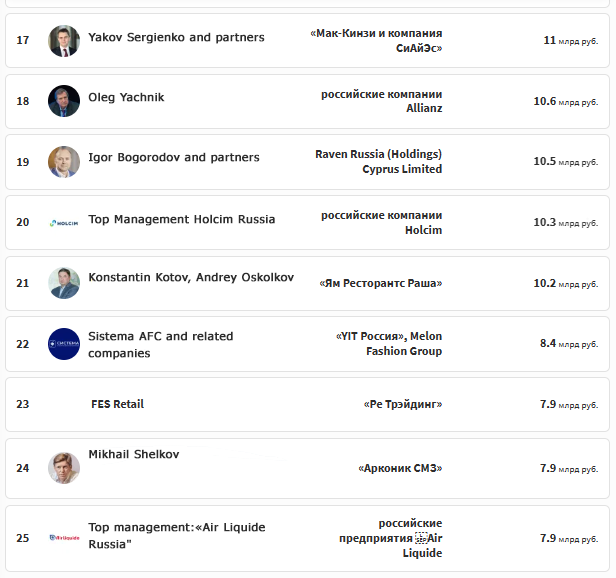

Last month Forbes Russia broke the silence by publishing a list of the beneficiaries and transaction values of the most significant transfers of assets from foreign to domestic ownership at the year’s end. The new list repeats several of the banking and oil asset deals published in the May report.

THE FORBES RUSSIA RATING OF THE TOP 25 NEW OWNERS OF FOREIGN ASSETS AS OF DECEMBER 2021

Source: https://www.forbes.ru/Total value Rb468.3 billion ($6.8 billion).

The tabulation is the first of its kind to appear in public; it is not definitive and may not be comprehensive.

It is noteworthy because just three pre-war oligarchs or their groups are listed — Vladimir Potanin at Number 1; the LUKoil group controlled by Vagit Alekperov at number 8; and the Sistema group of Vladimir Yevtushenkov at Number 22.

A name by name search through the sanctions listings of the US Office of Foreign Assets Control (OFAC) reveals that 22 of the 25 listings have not been sanctioned by the US. No attempt has been made by the Forbes Russia reporters to investigate what links may exist between the unsanctioned 22 and those Russian names and companies which have been sanctioned. The reason is obvious, as a senior state company chief executive comments: “At the point of sale I doubt there was a way for the [foreign] sellers to accept money from sanctioned sources. So the new names are not in the same spotlight.” He acknowledges that camouflage is required. The sanctioned oligarchs he knows “are overloaded with the [war] risks connected with the arrangements and agreements they have done with the managers of their assets.”

In defence of the foreign banks and the Anglo-American law firms advising them, the Financial Times, a propaganda outlet owned by the Nikkei group in Tokyo, reported last week that the Russian oligarchs whose assets have been seized abroad are retaliating by trying to take over foreign assets which remain in Russia. “Advisers to western banks trying to exit Russia say a law introduced by Vladimir Putin is disrupting sales and allowing deals to be hijacked by businesspeople close to the Kremlin. Almost a year into the invasion of Ukraine, only a handful of western banks have managed to leave Russia, albeit at steep cost, while others have made the choice to hold on to their businesses in the country. For the majority trying to sell their Russian assets, however, hopes for a swift exit were shattered when Putin last year said foreign owners from “unfriendly” countries could not complete deals without his approval. The list of affected companies includes 45 banks with subsidiaries in Russia. Advisers working on deals expect the Russian president’s intervention to thwart some sales already under discussion, while fundamentally altering the terms of others. They predict already agreed sale prices to fall by up to half as the Kremlin exerts more influence on deals. And they say would-be buyers who were originally beaten to deals have gained presidential approval and are attempting to hijack sales from rivals who lack the Kremlin’s favour. ‘There are some very powerful Russians with close links to the Kremlin who are trying to use their influence to grab these entities from fleeing foreigners,’ said a person involved in negotiations, one of several people who spoke to the Financial Times on condition of anonymity because of the sensitive nature of talks with the Russian government.”

The newspaper has pursued Russian-owned yachts when they have been arrested or confiscated. To date, it has not attempted to quantify the tit-for-tat – the value of Russian oligarch assets held abroad versus the value of foreign assets held in Russia. Instead, it has reported this tabulation of foreign bank assets in Russia, totaling Rb4.3 trillion ($63 billion).

Source: https://www.ft.com/

According to this US propaganda source, reporting the US Government calculation of Russian oligarch assets seized at the end of June 2022, the total value came to $30 billion. This is less than half the foreign bank asset valuation.

Glazyev, Khazin, Delyagin and the Communist Party parliamentary faction in Moscow were asked how they assess the Forbes Russia list. In the redistribution of the foreign assets, they were given three questions — do they see evidence that the pre-war oligarchs have not been gaining the advantage which might have been predicted? Do they recognize the interests represented by the new names on the list? What does the list indicate about the way in which the government is planning for the future direction of asset control in the economy?

All four refused to answer by telephone or by email.

In a lengthy lecture he published on January 13, Glazyev was sharply critical of what he called the Russian military strategy in the Ukraine, but he directed his blame at the Central Bank, its encouragement of continuing capital export by the oligarchs, and the government’s failure to replace oligarch profit schemes with state mobilization methods.

“The whole uncertainty of the coming year lies in the lack of strategy in Russia. Our leadership tried to seize the strategic initiative from the United States by accepting the LDNR [Lugansk and Donetsk People’s Republics], Zaporozhye and Kherson regions as part of the Russian Federation. But it is impossible to keep it without a clear ultimate goal, a clear ideology and a full-scale mobilization of resources to win the hybrid war with the collective West.”

“The first condition is the mobilization of all available resources to provide the army and the population with everything necessary. The most dangerous thing in military affairs, as you know, is the underestimation of the enemy. Having run into the fierce resistance of the neo-fascists, we continue to fight the collective West half-heartedly, if not to say carelessly. Following the seizure of more than $300 billion in reserves, the leadership of the Bank of Russia continued to condone the export of capital, the volume of which exceeded $200 billion last year [2020]. Of this total, $150 billion were payments abroad authorized by the monetary authorities on the credit obligations of Russian enterprises. Basically, in the jurisdiction of unfriendly countries which have begun to confiscate our foreign exchange reserves in order to use them to pay off military loans to Ukraine. Is it possible to win a war against an enemy that is many times superior in financial power by supplying him with money received from the export of raw materials to his own address? “

“We agree that the transition to a Soviet-style mobilization economy in a market economy is impossible. But the mobilization of resources through the targeted use of the same market mechanisms is absolutely necessary. From the capricious arguments of some official commentators of the Ministry of Defense that the supply of foreign equipment does not fundamentally change anything on the battlefield, it is necessary to move on to a sober assessment of the enemy’s potential. The military spending of the NATO bloc countries is an order of magnitude higher than ours. The USSR found itself in the same position by the end of 1941, when the economic potential of Europe united by the Nazis was an order of magnitude higher than ours. But we persevered because we used our potential to more than 100%, while in Germany the holidays were kept and the production of consumer goods continued. The slogan ‘Everything for the Front, everything for the Victory” is relevant again. The impediment by the leadership of the Bank of Russia to the full utilization of production capacities and connivance with the export of capital is incompatible with the achievement of Victory.”