It’s too easy to be a victim of confirmation bias. And your humble blogger generally steers clear of forecasting since the pros aren’t very good at it. But it nevertheless is noteworthy that Bloomberg is now warning a recession could hit as early as the fourth quarter, and one of the warning signs is one we’ve been calling out, too much complacency.

That bias particularly afflicts the Fed. In the US, as we pointed out early in the current tightening cycle, the Fed has assigned itself the job of tackling this inflation using the blunt instrument of interest rates to kill wage growth. We and others pointed out that this inflation was not created by excessive demand but by supply side issues, some caused by Covid (such as new car production due to chip shortages), then an energy crunch due to sanctions blowback, then labor shortages. The tight labor market has persisted, but headline inflation got a break due to energy prices falling…which has now gone into reverse, with oil analysts debating whether they will breach $100 a barrel.

We had warned that the Fed would have to kill the economy in order to increase unemployment, which is how the Fed thinks it regulates overall prices. It seems difficult to accept the widely-touted claim that the boomers retiring is the reason for the low unemployment rate give that prime-age labor force participation is still low-ish by historical norm. You would expect retiring boomers to be offset as much as possible by high emplooyment rates among the prime-aged cohort, but we aren’t seeing that. From the Wall Street Journal:

At a minimum, this pattern suggests that Long Covid has at least something to do with the conundrum of prime age workers not take up the supposed opportunities presented by strong demand for labor. I’ve heard other claim that some two-earner households learned how to get by with one during Covid and decided they want to continue. That is even harder to verify.

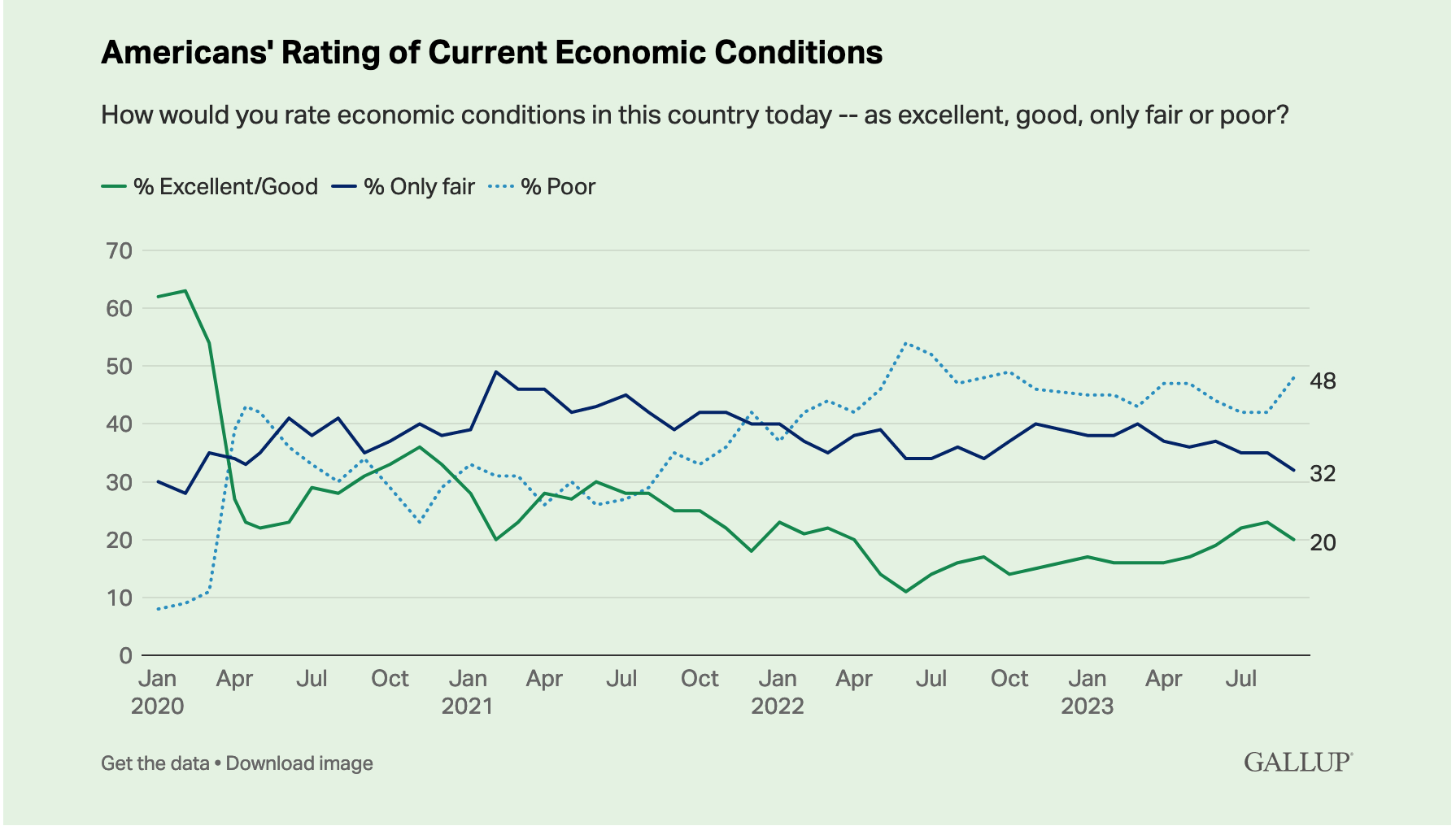

But on the other side of the equation, there is a lot of anecdata confirming the idea that consumers see their personal inflation rate as way higher than what the Fed believes, particularly with recent sightings of big increases in auto and other types of insurance. And this comes after all sorts of surveys show how cash-strapped most Americans are, and that that situation has gotten generally worse since all the Covid special relief programs were phased out. Mind you, most of you have an idea of this general picture, that few Americans are happy with economic conditions in the US:

Even with Team Dem pulling out all stops to stop Trump, that slide does not bode well for Biden’s and Democratic Congresscritters’ prospects for 2024. And that’s before getting to the fact that the US could see bona fide stagflation if growth falters. Bloomberg has a new piece that argues that a recession is pretty probable. I have been saying for a while that econpundits have already been unconsciously signaling that they expect things to go pear shaped. The last time I heard so much talk of a Goldilocks economy was 2007.

And the Bloomberg piece starts with a similar observation:

When everyone expects a soft landing, brace for impact….

A last-minute deal to avoid a government shutdown kicks one immediate risk a little further into the future. But a major auto strike, the resumption of student-loan repayments, and a shutdown that may yet come back after the stop-gap spending deal lapses, could easily shave a percentage point off GDP growth in the fourth quarter.

Soft Landing Calls Always Precede Recessions…

…And Fed Hikes Are About to Bite Hard…

For the parts of the economy that matter for making the recession call — above all the labor market — lags are longer, typically 18 to 24 months.

That means the full force of the Fed’s hikes…won’t be felt until the end of this year or early 2024….

A Downturn Is Hiding in Plain Sight in the Forecasts…

…And That’s Before These Shocks Hit

That assessment is mostly based on forecasts delivered over the past few weeks — which might not capture some new threats that are threatening to knock the economy off course. Among them:

- Auto Strike: …. The industry’s long supply chains means stoppages can have an outsize impact. In 1998, a 54-day strike of 9,200 workers at GM triggered a 150,000 drop in employment.

- Student Bills: Millions of Americans will start getting student-loan bills again this month, after the 3 1/2-year pandemic freeze expired. The resumption of payments could shave off another 0.2-0.3% from annualized growth in the fourth quarter.

- Oil Spike: A surge in crude prices — hitting every household in the pocket book — is one of the handful of truly reliable indicators that a downturn is coming. Oil prices have climbed nearly $25 from their summer lows, pushing above $95 a barrel.

- Yield Curve: A September selloff pushed the yield on 10-year Treasuries to a 16-year high of 4.6%. Higher-for-longer borrowing costs have already tipped equity markets into decline. They could also put the housing recovery at risk and deter companies from investing.

- Global Slump: The rest of the world could drag the US down. The second-biggest economy, China, is mired in a real-estate crisis. In the euro area, lending is contracting at a faster pace than in the nadir of the sovereign debt crisis — a sign that already-stagnant growth is set to move lower.

- Government Shutdown: A 45-day deal to keep the government open has kicked one risk from October into November – a point where it could end up doing more damage….

…And the Credit Squeeze Is Just Getting Started

On the bank side, a lot of shoes could drop. The Bloomberg describes how banks are getting more stringent about commercial and industrial lending. We also have a world of hurt in many sectors of commercial real estate, starting with big city office space. In fairness, many of those loans wound up held by investors, either directly by buying commercial real estate securitizations or investing in private equity credit that hold commercial real estate debt, typically along with private equity debt. But if a few not-small bank were hit with enough losses on commercial real estate loans, it could generate deposit flight and/or counterparties for short term loans limiting exposures.

More generally, it’s an open secret that regulators are engaging in a lot of forbearance by not forcing bank to do much in the way of recognizing the impact of mark to market losses by letting them treat the loans as “hold to maturity.” And that is not crazy if the banks really can leave these holdings be until the Fed decides to ease in a meaningful way. But the longer the central bank stays bloodyminded, the more the odds increase that bank will need to offload some of these holdings at a loss because liquidity needs.

Bloomberg points out that China’s growth weakening is part of the picture. Keep in mind, as we explained long form in Emerging Economies Face Prospect of Worse Than 1970s-1980s Wave of Financial Crises, that there is a ticking debt bomb there that looks set to go off. Developing economies wind up suffering in Fed tightening cycles because they see a hot money exodus, a domestic credit drought, and currency weakness if they don’t increase interest rates. But the higher rates choke domestic activity.

Remember that a emerging economy debt crisis will impair advanced economy lenders too. Lehman almost failed in the 1997 Asian crisis, and the collapse of LTCM threatened to kick off a bigger conflagration.

So the China slowdown matters, not just in and of itself but also for its knock-on effects to developing economies, particularly its neighbors in Southeast Asia. China hawks may be a bit too chuffed that US sanctions and Collective West decoupling/derisking might have something to do with that. From the Financial Times Asia faces one of worst economic outlooks in half a century, World Bank warns:

China’s policymakers have already set one of the lowest growth targets in decades for 2023, of about 5 per cent.

Citing a string of weak indicators for the world’s second-biggest economy, the World Bank said it now expected China’s economic output would grow 4.4 per cent in 2024, down from the 4.8 per cent it expected in April.

It also downgraded its 2024 forecast for gross domestic product growth for developing economies in east Asia and the Pacific, which includes China, to 4.5 per cent, from a prediction in April of 4.8 per cent and trailing the 5 per cent rate expected this year….

Softer global demand is taking its toll. Goods exports are down more than 20 per cent in Indonesia and Malaysia, and more than 10 per cent in China and Vietnam compared with the second quarter of 2022. Rising household, corporate and government debt has further dented growth prospects.

The worsening forecasts also reflect that much of the region — not just China — is starting to be hit by new US industrial and trade policies under the Inflation Reduction Act and the Chips and Science Act.

For years, US-China trade tensions and tariffs imposed on Beijing by Washington benefited south-east Asia, driving demand for imports towards other countries in the region, especially Vietnam.

But the introduction of the IRA and Chips laws in 2022 — policies designed to boost US manufacturing and cut American dependence on China — has hit south-east Asian countries. Their exports of affected products to the US have fallen.

China fans try to put this in context:

Interesting: despite all the talk about China’s economy, the latest World Bank report on East Asia and the Pacific clearly shows that since the beginning of the Covid crisis, China has remained the fastest growing economy in the region, with a GDP 20% higher than before Covid. pic.twitter.com/1tBVYmyyZu

— Arnaud Bertrand (@RnaudBertrand) October 2, 2023

But even so, it is China that cut its growth estimate. And it looks as if China getting a cold might lead to pneumonia in some of its key trade partners.

Mind you, none of the things under discussion are more than negative tendencies. But they bear watching, particularly given too many still over-inflated asset prices and dysfunctional elites.