Yves here. Rob Urie takes a step back to place the murder of the UnitedHealth CEO Brian Thompson in a broader political/economic context. It’s not news that the US health care industry prioritizes profit over care. But most choose to avert their eyes to the fact that the government enables this exploitation of ordinary citizens.

One quibble with Urie’s post. He suggests that employer plans could have even worse claims denial rates than Obamacare, Medicare, and Medicaid, where private insurers must provide the data on their handling of individual claims. As many business articles have suggested, the reverse is likely to be true. Employer plans have more members and employers have bargaining leverage, in terms of being able to switch insurers or even self insure. IRS rules also make it hard for employers to offer better terms to executives (see here for an idea of the rules). Mind you, that may not wind up being much leverage given the general crapified level of US health insurance, but no one has less leverage than individual consumers.

And an observation now that Luigi Mangione has been charged in Thompson’s murder, and due to his family wealth, seems able to hire the caliber of lawyers that can defend him well: his case is very unlikely to go to trial. The last thing the government and people in power want is a potentially messy trial. They will try hard to get him to cop a plea. And if the pain from his not-very-successful back surgery is ongoing, you can be sure it will be made difficult for him to get his meds to make him more cooperative.

By Rob Urie, author of Zen Economics, artist, and musician who publishes The Journal of Belligerent Pontification on Substack

The assassination of United Health Care executive Brian Thompson has some not-insignificant aggregation of the American public musing that Thompson reaped what he had sown. Without the assassin revealing his motive for the shooting, no motive is attributed here. But there is enough in the public domain regarding insurance companies and insurance claim denial rates by individual companies to organize a political argument around what may have motivated the shooter.

From this dark celebration, a sense is emerging that the assassin was addressing the problems of the age that the American political system is incapable of addressing. American elections operate under the fallacy that the results reflect the will of the people. Ideologues and paid pleaders even attribute ideological motives to the corrupt opportunists who ascend in the American form of political economy. And every story of imminent redemption is soon revealed to be just one more step in the process of imperial decline.

Having rebegun writing publicly soon after the ACA (Obamacare) was passed, my warning at the time was that the keys to the American healthcare kingdom were being handed to a corporate form— the health insurance industry, that would never stop using its economic power to benefit its executives alone. Further, corporate control over our lives is a form of political control. Markets didn’t form the ACA. It was structured as a bribe paid for by the American people to keep Mr. Obama’s party in power.

One of Joe Biden’s key selling points to Democrats in 2020 was his promise to shovel more of the people’s money into the ACA even as Americans were dying at levels associated with societal collapse (details below). And while, this being America, his PMC constituents had little understanding that the society that their ‘lessors’ inhabited had collapsed around them, public expenditures in the name of the ‘little people’ led many of them to believe that they had been absolved for perpetuating this system.

A paradox of capitalism is that public expenditures funneled through corporations act against their alleged intent. Through the benign (liberal) view of the intersection of commerce and government, ‘partners’ in the public and private sectors work together to solve social problems while making bank doing so. The less benign view is that this coalition represents the class interests of our ‘betters’ against us. The role of government in this latter view is to keep us prostrate and powerless so that we can be most effectively preyed upon by ‘private’ interests.

In 2022, the last year that data is currently available for, Andrew Witty, the head of United Health, the parent company of Mr. Thompson’s United Health Care, was the fourth best paid health insurance executive in the US, earning a tad over $22 million. As the data below suggests, the special talent of both Mr. Witty and Mr. Thompson is taking in insurance premiums without paying claims. Using color coding or some such, a chimpanzee could be trained to deny insurance claims. However, America is set up to reward this type of behavior.

The accounting formula P = R – C; where P = Profit, R = Revenue, and C = Cost; explains a lot about the US. With respect to both generating environmental ‘externalities’ and denying insurance claims, costs aren’t being borne by the corporations they belong to. Doing this raises their profits. Profitability in turn boosts the company’s stock price, and with it, executive compensation. Executives then use the gains ‘earned’ from robbing their customers to control political outcomes via political donations; through the Federal revolving door of legislators becoming corporate executives; and through large-scale grifts like the ACA.

In 2009, a de-privatized Medicare for All would have been the rational and just solution to insurer control of the health care system. In contrast to the ideological view that corporate health insurance is more efficient because it is private, Medicare has consistently delivered (and here) better health care at a lower cost than private insurance. The logic that remains tells us that the continuing effort to privatize the American health care system is therefore to loot it.

To the issue of causality, the ACA and declining life expectancy have moved together in time through a decade of changing circumstances. The common root is the political – economic backdrop which features the virtual abandonment of the public health roll historically played by the Federal government. After chiding the first Trump administration for its reluctant response to the Covid-19 pandemic, the Biden administration oversaw the effective dismantling of the very idea of public health in the US. This being America, Biden’s low bar will represent the new high bar.

This story has additional resonance with yours truly because both of my parents had to hire lawyers to get their pensions. Neither had been accused of wrongdoing and both were in good standing with their employers when they retired. Suffice it to say that the situation wouldn’t have ended well for anyone involved had the lawyers not been able to resolve it. The time to tell someone they will not receive their pension is before they labor for 25 – 35 years to earn it. But in my parent’s case, the lawyers worked it out.

The scuttlebutt (internet chatter) is that Brian Thompson had net worth of $43 million dollars when he met his maker. While average household net worth in the US in 2023 was a touch over $1,000,000, median net worth was about one-fifth of this amount, at $193,000. Interpretation is that wealth distribution in the US is radically skewed by a small group of very rich. They are so rich compared to the rest of us that the scale dwarfs what most Americans imagine rich to be.

(Income and wealth in the US are exponentially distributed, meaning that statistical interpretation must be undertaken with awareness of what this entails. An average that is greater than the median is skewed, meaning that the average is unrepresentative of the experience of most people. This makes most averages of income and wealth either intended to overstate the experience of most people, meaning deceptive, or ignorant of economic statistics).

ProPublica revealed in an article from June 2023 that private insurers in the US have no legal obligation to publish their claim denial rates. The exception is insurers in the ACA, Obamacare. And while no authoritative source on the matter was readily found, estimates have it that claim denial rates above 5 – 10%, or 10% by another forum, are signals of possible financial distress and / or fraudulent business practices. With respect to the ACA data, the average claim denial rate has hovered around 18% since 2014, the year the ACA was implemented.

Graphic: with dates relevant for assessing the effects of the ACA, in 2021, 67.3% of ACA insurers had claim denial rates above 11%. The threshold for legitimacy is 10%. While this is better than the 78.4% of 2015, the year after the ACA was implemented, the difference is mainly attributable to a few outliers, one with a 92.5% claim denial rate. All of the largest insurers in the ACA have claim denial rates that are several multiples of the rate deemed by the industry to be legitimate. Source: kff.org.

In 2021, the last year for which data is available, 67% of Obamacare (ACA) plans had claim denial rates above 11%. Many were in the high thirties – low forties. The highest claim denial rates are concentrated amongst the larger insurers, those insuring the most customers. These tend to feature well-paid executives who have large personal and career incentives to line their own pockets by denying legitimate claims.

Part of the logic of forcing ACA insurers to disclose claim denial rates is that Americans are legally mandated to either have health insurance through their workplace or to buy it through the ACA exchanges. I had to search for the data and perform statistical analyses to understand these claim denial rates. Most people will not do this. The difference between the ten highest and ten lowest claim denial rates amongst ACA providers in 2021 is 41%. Interpretation is that the top ten insurers deny 41% more claims than the bottom ten insurers.

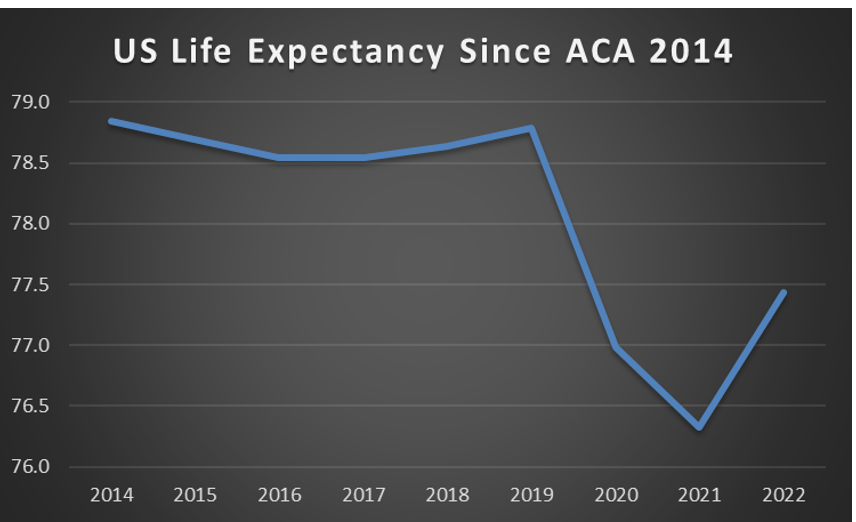

Graph: discussion of health insurance that isn’t informed by outcomes is of limited value. Since 2014, the year that the ACA was implemented, Life Expectancy at Birth has declined dramatically in the US. The largest decline illustrated is from the Covid-19 pandemic. As horrifying as the absolute number is, the relative number— against peer countries, is even worse. What this indicates is that the American healthcare system is failing, irrespective of the ACA. Source: worldbank.org.

Given that health insurers that sell policies through ACA exchanges know that they will have to disclose their claim denial rates, it seems reasonable to infer that the health insurers who sell policies directly to employers have even higher claim denial rates. According to ProPublica, this is because there is no legal requirement that health insurers outside of the ACA disclose their denial rates. And continuing, it is common practice for insurers to keep claims denial data hidden.

Question: who would willingly buy insurance from a company that denies one-third of the claims it receives? By the health insurance industry’s own metrics, this level of denials is wildly abusive. And it’s a permanent game of Russian Roulette for insurance ‘customers.’ If fortune is with you, the healthcare that you have already paid will be funded. If it isn’t, the rest of your life will be spent bagging groceries to pay for $300 aspirins as excess medical debt renders you unemployable.

Soon after the ACA was passed, Democrats started calling it ‘universal healthcare.’ If it weren’t for the 30% – 40% of claims that don’t get paid because there is no entity with the power to make insurance companies do so, they might have an argument. What is particularly galling about the effort is that the long history of predatory behavior by the insurance industry was available to anyone who cared to look. The idea that ‘market forces’ would discipline the industry had already been disproved by history. This makes its subsequent adoption in the ACA ideological.

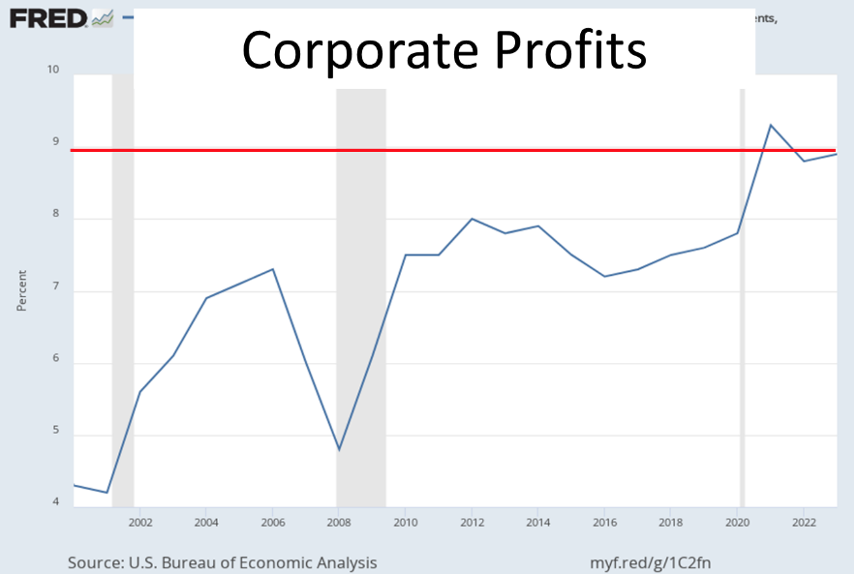

Graph: corporate profits as a percentage of GDP in the US are currently near record levels. This is further evidence of a power imbalance between capital and we, the people. One of the sources of these record profits is health insurers that collect premiums and then refuse to pay claims. Compare this graph with the one immediately above it and it becomes clear that rising corporate profits are correlated with the rapid decline in life expectancy in the US. Source: St. Louis Federal Reserve.

To return to the question of causality for a moment, correlation, or the co-movement of data across time, doesn’t prove causality. The correlation of corporate profits with declining life expectancy is a product of Federal efforts to protect the wealth of the rich when the Covid-19 pandemic arrived. This is phrased the way that it is to convey the point that pandemic funds could in theory have been paid directly to those who were economically displaced by the pandemic. But much of the money went into goosing the stock market instead.

In terms of options, the American powers-that-be offer only self-defeating choices. If all of the large ACA insurers have claim denial rates of 30% – 40% (they do), capitalist ‘choice’ is a fraud. As with Biden v Trump, were a real choice to be offered, the uniparty exists to neuter it. The Democrats could have crafted a system that works. Functioning healthcare systems do exist in other countries. But what they created instead is a system built for looting.

The employees at American corporations who haven’t yet been trained in what not to say sometimes give the game away. The representative of my internet service provider stated openly that his company had colluded with the other providers in the state to eliminate price competition. A former home insurance agent offered that once a claim is paid, the company divides the payout across future premium payments until the company has recouped the payout. This is a description of a payday loan, not insurance. Actual insurance is a risk sharing scheme.

We’re human, runs the logic, therefore we will all face medical emergencies that 1) we cannot predict the timing of and 2) which we cannot afford to pay for individually. By pooling resources, we pay in when we don’t need health care expecting that when we do need it, it will be there. But this isn’t what capitalist corporations are structured to do. They hire MBAs whose job it is to imagine ways to not pay the company’s bills. Straight up screwing their most vulnerable customers is the easiest power play.

The role of capitalism in this American healthcare debacle is important to understand. The ideological argument in favor of the private provision of healthcare is that capitalist enterprises are more ‘efficient’ than government programs because of the profit motive. Missing from this logic is that refusing to deliver purchased goods is a way to cut costs, and thereby increase profits. Changing the terms after the purchase has been made is one way of achieving this end.

On personal experience, through a series of large and small purchases over the last year, every purchase featured the delivery of different terms after the purchase was made than before it was made. I would have decided against making three-quarters of the purchases had the final terms been provided before the purchase was made. Companies know this, hence the deception. One such purchase of musical software will require days of work to remove from my system. This was revealed to me only after the (nonrefundable) purchase had been made.

The point is that this is the capitalist profit motive in action. Before she went full-Hiawatha, Elizabeth Warren called these gotchas ‘tricks and traps,’ The claim / promise that came with the ACA was that the tricks and traps had been eliminated in exchange for the Federal government delivering 45 million new customers to the health insurance industry. But the enforcement mechanism— market discipline, is a fantasy. Health insurers wouldn’t deny 30% – 40% of their claims if they thought that doing so would sink their businesses.

A confusion that plagues capitalist economics lies between the large and intrusive state that is needed to keep capitalism functioning under Neoclassical theory, and the blanket support for existing power that defines neoliberalism. The tendency of capitalist enterprises to behave badly has long been understood by economists. The term used to describe this bad behavior is ‘moral hazard.’ What this means is that when given the opportunity, corporations take it. The purpose of the large and intrusive state then is to assure that these opportunities to behave badly don’t arise.

Beginning in the Jimmy Carter – Ronald Reagan era, the theory was popularized that ‘free markets,’ or markets unencumbered by regulations, would regulate themselves. The theory had it that customers wouldn’t do business with nefarious actors because the are nefarious. To solve this problem, nefarious actors use government to hide their activities. Anti-terrorism laws were passed to protect factory farms from exposure of slaughterhouse conditions. Industrial agriculture was able to get disclosure laws repealed that would have alerted customers that GMO crops are present in their food. And insurance companies are allowed to hide claim denial rates from their customers.

The rationales for doing so were / are paper thin. Slaughterhouse conditions are relevant information for those who eat meat. If cruelty is part of the process, that impacts both the quality of the product and the moral calculus of whether or not to partake in it. And the seed producers unleashed GMO crops outside of sterilized conditions. The first GMO test that I saw (1998) featured GMO corn planted next to non-GMO corn. Cross pollination was the obvious plan.

Soon thereafter the seed companies began suing non-GMO farmers for patent infringement for the cross-pollination that the seed producers had intentionally engineered. Not infecting non-GMO crops via pollination should rightfully have been the burden of the seed company that was introducing the GMO crop. But they are large corporations and the victim-farmers are small enterprises. This is the same type of power relationship that United Health Care has with its ‘customers.’

In contrast to the ideological complaint that government regulations impinge on the ability of corporations and oligarchs to earn profits, the history of the US government has been to support business against the interests of the people since neoliberalism first gained credence beginning in the 1970s. The insurance industry in particular has been given special dispensations that render it immune to market forces. Not only does the ACA force people to buy insurance that is illegitimate on its face because of excessive claim denial rates, but there is no recourse against these fraudulent denials outside of company-run ‘tribunals,’

To the issue of capitalist efficiency, my favorite example is the automated checkout counters installed in stores. Amongst the dozen or so people I’ve spoken with about the matter, all believe that ‘we all’ benefit from this type of innovation. What the machines actually accomplish is to shift the cost of checking out away from the stores and onto its customers. No labor is saved through this practice. It was shifted from the cashiers who were paid to do it onto the customers who aren’t paid to do it. There is nothing ‘efficient’ about the practice.

The regular call amidst the recurring crises of capitalism is for reform. Through the liberal lens, ‘we’re all in this economy together.’ Through a Marxist lens, the use of government by the rich against the rest of us reflects asymmetrical class power. And the shifting of costs from capital and the oligarchs to ‘the little people’ has defined class relations across the current age. The rich and corporations today pay a tiny fraction of costs of their social support. Despite having never voted on the matter, the rest of us have been tasked with making up the difference.

I’ve been wondering when the shooting would start since 2009 or thereabouts. That was when the contours of Barack Obama’s consequence-free bailouts of the bankers who caused the Great Recession was matched against the ‘freeing’ of their victims (from their employment, homes, families, and broader society) to crawl into a ditch and die. But ‘the system’ was saved, right? Since then, finance capitalism gone wild has brought ‘us’ two pointless and murderous wars, a society that is dysfunctional to the point of full-on collapse, and the threat of nuclear annihilation.

Few among us wish for violence, particularly those of us who have seen it manifested. That is why it would have been socially beneficial had Brian Thompson been hauled out of his office in handcuffs in front of television cameras for his company’s business practices. The problem is that they were / are probably legal. In the American iconography, Thompson is a hero and his killer is a goat. But Thompson likely killed a lot more people than his shooter has. And he appears to have done so without compunction.

The bet here is that the social / government response to the shooting will be increased political repression. Greater efforts will be made to hide corporate malfeasance under the theory that doing so will reduce the risk of further executive assassinations. The result-to-date of this practice has been an explosion in corporate malfeasance that may not be reported in the news, but is being felt in the streets. I personally won’t ever do business again with companies once I have been burnt. But I have fewer needs than most and otherwise just don’t care about consumer culture.

While it’s socially endearing in some circles to argue that the wrecking crew has just arrived, American capitalism has always been run by gangsters. From 2016 – today, American Democrats have defended the American state and its institutions by arguing that any and all criticism comes from nefarious foreign actors and homegrown malcontents. But what they were ultimately defending was Brian Thompson’s right to line his own pockets by refusing to pay insurance claims.