Commodities have been on a tear this year, but they’ve been cooling off of late.

The S&P GSCI SPGSCI, +0.71%, a broad-based commodity index, has surged 31% this year but has stumbled 7% over the last five days. Oil futures CL.1, -4.34% have been trading below $105, compared to the peak of over $130 in March.

The Australian bank Macquarie has been bearish on commodities since March. They’ve been arguing that strong supply growth is being incentivized, which will dovetail with the negative impact of inflation on demand.

In a new strategy note, the Macquarie team concede they did not anticipate the speed at which many markets would correct in the second quarter. “To a certain extent this reflects an unwind of risk premium in those markets where Russian supply has neither yet been heavily disrupted (e.g. palladium and aluminium amongst the largest losers) nor is it expected to be in the near future – note that outperformers thermal coal and crude both face export sanctions, whereas TTF gas had been the largest faller before the past week’s supply disruptions,” they said.

Also making its mark is the downturn in the stock market in most countries as well as the severe COVID-19 lockdowns in China.

So what does the firm expect now? They say commodity prices will be steady in the third quarter and get stronger in the fourth, but that should be as good as it gets. China will fail to sustain a strong economic growth cycle, and developed markets will fall into a technical recession by the summer of 2023. They say there are growing examples of physical demand weakness, such as in falling physical aluminum premiums and collapsing scrap steel prices.

Their least preferred commodities over the next 12 months are oil and industrial metals. On oil, they warn, demand headwinds should emerge just as U.S. production ramps up and Russian export losses miss expectations.

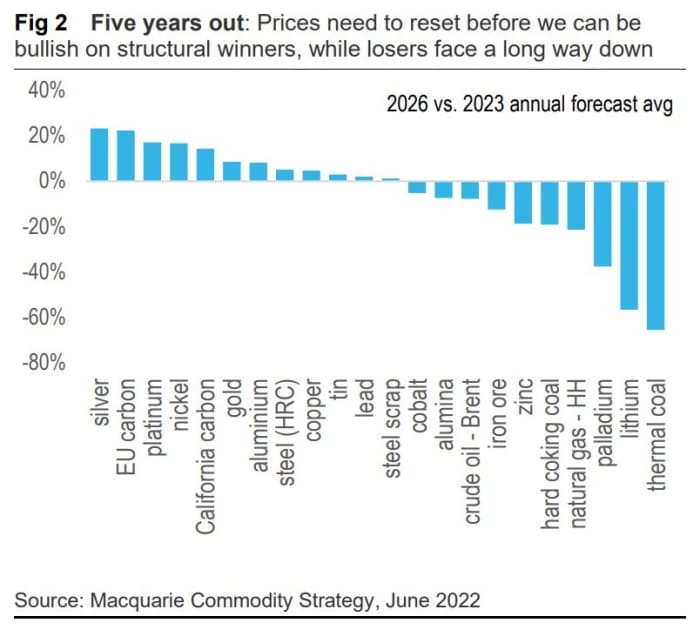

Over the next five years, they identify carbon and electrification metals as winners, and palladium, zinc and fossil fuels as strugglers.