As the Trump 2.0 administration takes off, it looks like he’s only doubling down on US efforts to plunder Europe despite his campaign talk about getting out of Ukraine and downsizing the US role in NATO.

The monied interests behind Trump would be wholly opposed to a US retreat from Europe because of the simple fact that they’re making a killing off the EU’s dependence on the US for energy, defense, and tech. And the oligarchs at the head of these industries, which largely run Washington, want more instead of any rethink about what is in the US national interest.

Let’s take a look at each of those sectors, what Trump 2.0 is doing to pick up the pace of the pillaging, and examine the exorbitant amount of money US plutocrats are making off Europe — a process which, lest we forget, is the result of Project Ukraine and the walling off of Europe from Russia.

Energy

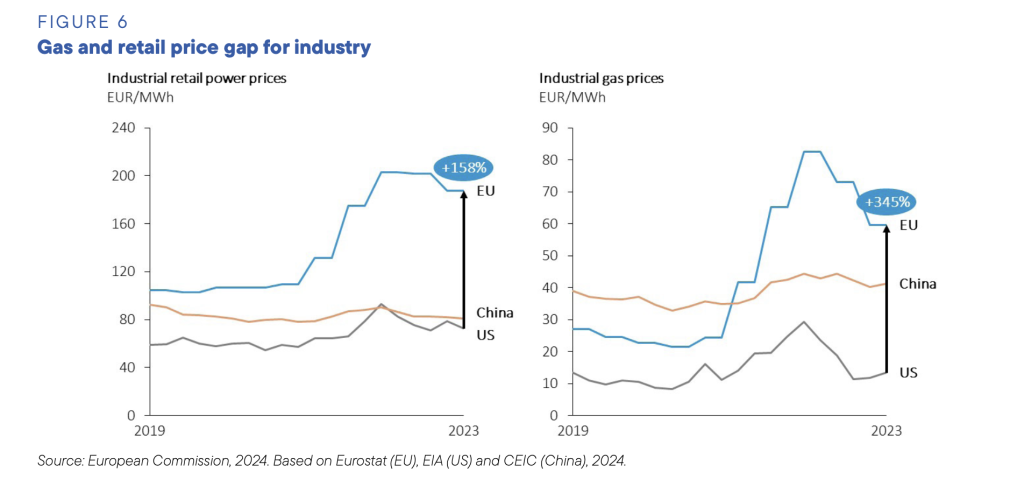

By mid-2023 the fiscal outlay in the EU to help consumers and businesses deal with rising energy costs amounted to 651 billion euros. That’s obviously much higher by now, and doesn’t include billions more to hurriedly get LNG terminals up in running over the past three years.

How much did American energy companies cash in? It’s hard to say for certain, but safe to say it’s a lot. A 2023 report from Global Witness argues that the five Western oil majors (which includes ExxonMobil and Chevron from the US) made $134 billion in 2022 alone off Europe partially severing itself from Russian oil and gas. In 2023, the US supplied 50 percent of total LNG imports to the EU, tripling export volumes from 2021, and Europe also locked itself into dozens of long-term LNG contracts with US companies that will have them buying American gas for two decades or more.

And yet the windfalls aren’t quite what they once for the American energy companies. So many new oil and LNG projects coming online are producing a glut that is expected to lead to lower market prices for the rest of the decade, and the oil and gas majors are expected this week to report sharply lower profits than the 2022 boom year.

The US is still competing with Russia for the Europe LNG and oil market, however, and the Trump administration is pushing for exclusive seller status. The Atlantic Council:

Importantly, a significant return of Russian gas to Europe would severely harm US LNG exporters and Trump’s “America First” agenda…the resumption of significant Russian gas flows to Europe, though seemingly unlikely at present, would put pressure on US LNG exporters.

…Since February 2022, US crude exports to Europe have increased by 800,000 barrels per day, helping to displace Russian production that was cut off as a result of Russia’s invasion of Ukraine. With US liquid fuels consumption projected to decline by 2026 and domestic gasoline demand already peaking, US oil and gas exporters will increasingly rely on external markets, intensifying competition with Russian producers.

What’s the solution?

Strengthening sanctions on Russian oil and gas now will not only benefit US companies. It will also give Trump more negotiating leverage over Russian President Vladimir Putin.

Who knows if they believe the latter nonsense about negotiating leverage, but the first statement certainly seems to be gaining steam as a way to keep the Americans in and well-compensated.

European Commission President Ursula von der Leyen, doing her best to prove her worth, came up with a plan shortly after Trump’s election to buy even more gas from the US, which would increase dependence on the US while simultaneously doing even more to wreck the economies of EU states. From Politico:

Stressing that the EU still buys significant amounts of energy from Russia, von der Leyen asked: “Why not replace it by American LNG, which is cheaper for us and brings down our energy prices? It’s something where we can get into a discussion, also [where] our trade deficit is concerned.”

On Ursula’s contention that US LNG is cheaper, there is of course evidence to the contrary, but no matter. What’s next? Offering to make the US the exclusive supplier and pay above market value to help keep US energy companies profitable during the wild-eyed effort to “crash the price of oil to crush Russia”?

We’ll have to wait and see what comes out of an EU task force is preparing measures to assuage the Trump administration and its backers in the American energy sector. Germany’s Handelsblatt last week reported the proposals include further sanctioning Russian gas exports to tilt the market in favor of American producers.

Hungarian Prime Minister Viktor Orban who was supposed to be part of the new nationalist vanguard in Europe and the US that would pursue state interests instead looks like he’s being hung out to dry in his effort to block more EU sanctions against Russia. As we’ve written, Trump’s interest in European “nationalists” only extends to those like Italian Prime Minister Giorgia Meloni and now the Alternative for Germany, which are willing to use their faux nationalism in the service of the American empire.

Weapons

US arms exports hit a record high in 2024 — up 29 percent to a record $318.7 billion. Consider last year’s sales as a parting gift from the “Big Guy” whose administration promised trillion-dollar-plus investment for social welfare but gave it to weapons companies instead.

But Lockheed Martin, General Dynamics, and Northrop Grumman are all forecasting that their sales will continue to climb under Trump 2.0 — and Europe is a large part of the “global instability” they cite as a reason.

Trump of course wants non-US members of NATO to spend 5 percent of their gross domestic product on defense – a gargantuan increase from the current 2 percent target. That is unlikely, but even smaller hikes up to say 2.5 or 3 percent will mean billions for US weapons companies and untold pain for millions of Europeans who will be forced to suffer through social spending cuts in order to fund the militarization.

From the Stockholm International Peace Institute:

Arms imports by European states were 94 per cent higher in 2019–23 than in 2014–18. Ukraine emerged as the largest European arms importer in 2019–23 and the fourth largest in the world, after at least 30 states supplied major arms as military aid to Ukraine from February 2022.

The 55 per cent of arms imports by European states that were supplied by the USA in 2019–23 was a substantial increase from 35 per cent in 2014–18. The next largest suppliers to the region were Germany and France, which accounted for 6.4 per cent and 4.6 per cent of imports, respectively.

‘With many high-value arms on order—including nearly 800 combat aircraft and combat helicopters—European arms imports are likely to remain at a high level,’ said Pieter Wezeman, Senior Researcher with the SIPRI Arms Transfers Programme. ‘In the past two years we have also seen much greater demand for air defence systems in Europe, spurred on by Russia’s missile campaign against Ukraine.’

In many ways Europe’s bureaucracy has already changed in small but fundamental ways in order to redirect money towards war. From Equal Times:

“In 2023, there was a very significant increase in military spending worldwide, but especially in Europe. In Spain, for example, it grew by 24 per cent and in Finland by 36 per cent. If we compare it with 2013, the European countries in Nato are spending 30 per cent more,” says Pere Ortega, a researcher at the Barcelona-based Centre Delàs for Peace Studies, which is critical of measures adopted by the European Commission to promote military spending, such as the VAT exemption for the purchase of armaments or the change in the regulations of the European Investment Bank (EIB) to allow it to finance industrial projects in the military sphere.

And according to the European Council on Foreign Relations, the number of countries meeting the two percent target has risen from 3 to 23 since 2014 (the following is from July; an updated version would show even steeper inclines):

Many European states are running into budgetary constraints and therefore cutting to the bone elsewhere, including education, healthcare, and energy subsidies intended to soften the blow of cutting itself off from Russian pipeline gas.

While such social austerity is a crisis for some, it’s an opportunity for others.

European Elites Sell Out Their Countries

US Secretary of State Antony Blinken calls the United States’ allies and partners “force multipliers” and “a unique asset.”

Assets, indeed. As more European companies struggle due to high energy costs and long-stagnant economies driven in large part by the EU’s obsession with austerity, they’re increasingly becoming the focus of merger and acquisition specialists from the US. CDI Global reports the following:

In recent years, a marked increase in cross-border mergers and acquisitions (M&A) by US companies in Europe has emerged as a notable trend. This surge in transatlantic investment signifies a strategic shift by American firms, grounded in the USA, aiming to harness the diverse advantages and lucrative opportunities presented by European markets. From established corporate giants seeking expansion to agile start-ups on the lookout for innovative growth pathways, numerous compelling factors drive US businesses to explore European bargain-hunting ventures…

A significant allure for US companies investing in Europe is the potential for acquiring assets at bargain prices. Economic uncertainties, geopolitical fluctuations, and evolving market dynamics have led to decreased valuations of European companies in recent years. This creates a favorable environment for US investors, allowing them to purchase valuable assets at more attractive prices than those typically found in the US market.

In addition to favorable valuations, Europe offers relatively lower costs associated with labor, research and development (R&D), and operational expenses. European countries often provide substantial subsidies, tax incentives, and grants aimed at fostering innovation and business development, reducing the financial burden on US firms.

US private equity giant Clayton Dubilier & Rice destroyed the UK’s fourth largest supermarket chain in a few short years. Warburg Pincus joined a consortium to snatch up T-Mobile Netherlands a couple years ago. US-based Parker Hannifin is taking private the UK aerospace and defence group Meggitt. Gores Guggenheim grabbed Swedish electric carmaker Polestar.

The private equity behemoth KKR, which includes former CIA director David Petraeus as a partner, took home the fixed-line network of TIM, Italy’s largest telecommunications provider.

The government in Rome is also contemplating handing over public sector security services like encryption services to Elon Musk’s SpaceX. Elsewhere “Italy Is For Sale.” Why? So the Meloni government can give more tax cuts to the wealthy and because Rome is already short on cash due to the billions of euros it has burned through in order to address the loss of pipeline gas from Russia.

German energy service provider Techem was just sold off to the US asset manager TPG, and Germany’s awful economy is increasingly making its companies more likely targets for takeovers. The spooky Silicon Valley company Palantir is already making itself at home in the UK National Health Services, and it’s knocking on the door in Italy. Meera Shah, a senior corporate finance manager at Buzzacott and member of the Corporate Finance Faculty’s board, explains:

“Selling assets into the US has always been a fairly chunky part of what we do, but even with that track record, we’ve seen a significant increase in inbound interest from the US. There have been months where up to one third of the businesses we’ve sold have gone to US buyers.”

Guarding against China and Russia while the US strip-mines Europe is apparently a good thing because letting the US take over Europe means a successful “de-risk” from China and Russia.

NC reader Chuck Roast provided some more detail recently:

US Capital’s bust-out operation in Europe may be gaining momentum due to the increasing value of the dollar and the general weakness of Euro businesses and corporations. Invest Europe publishes economic info “…on fundraising, investment and divestment from more than 1,750 private equity and venture capital firms in Europe.” According to their data Euro PE activity is down appreciably since 2022.

The FT reported last week that the “total value of large private equity deals in Europe increased at twice the rate of the rest of world in 2024.” While they mentioned a huge deal by Chicago PE firm Thoma Bravo they didn’t break down the total. However, in an accompanying chart the buyout total from ’23 to ’24 increased from $75B to around $135B…most of this was clearly not Euro PE firms. The piece merely says that it was US PE targeting Euro firms.

That Financial Times report alluded to how US private equity firms are taking advantage of the continent’s economic downturn to purchase big companies at lower valuations. And according to PitchBook, deal value with US participation rose 51.9% last year—almost 1 in 5 deals involved US investors—and they also took part in seven out of the top 10 deals in 2024.

Trump, Mario Draghi, the Tech Oligarchy, and the Atlantic Council

Thierry Breton, the former Commissioner for Internal Market of the European Union used to say that “a radical change needs to be achieved quickly to manage… the digital transition and to avoid external dependencies in the new geopolitical context.”

It’s unclear if Breton still feels the same after recently taking up his new role at Bank of America. But his journey is illustrative.

The EU is already dominated by US IT companies that supply software, processors, computers, and cloud technologies and we can expect more of that as Europe falls further behind due to its non competitive energy market and inability to keep up with US and Chinese investments.

EU officials talk a lot about solutions, but unless I’m missing something, none of them deal with the elephant in the room:

Former EU Central Banker, Goldman Sachs exec, and supposedly serious economist Mario Draghi is one of the worst offenders. He released his big report last year, which quickly glossed over the primary issue dooming European competitiveness: its loss of pipeline Russia gas, which has caused its energy costs to skyrocket.

Instead Dragi goes on for hundreds of pages about the need for more centralized authority in the EU, the need for more concentration, less labor law, etc. It’s typical of the genre — basically, a realization of the long held neoliberal-authoritarian dream for the bloc.

It’s worth briefly examining how this process is unfolding through the triangle of the US oligarchy, its think tank lackeys, and the point people in Europe: Mario Draghi and Ursula von der Leyen.

Two of the biggest fans of the Draghi report are von der Leyen’s Commission, which requested the Draghi report and just adopted its shoddy methodology for its upcoming “Single Market Report,” and US think tanks, which are some of its biggest proponents of the Draghi prescriptions.

Now why are American think tanks, funded by US plutocrats, so concerned with helping the EU compete? The Dragi report is, after all, titled The future of European competitiveness.

Let’s take a look at a recent piece from the Atlantic Council touting Draghi’s recommendations:

Importantly, the goal of increasing EU competitiveness as outlined in the report is not at odds with the need to strengthen transatlantic economic cooperation.

Of course not! The tech oligarchs are eyeing billions from the EU in tech investments for military and surveillance purposes. They want the EU to pony up like the US:

When it comes to supporting new technologies, for example, the European Innovation Council’s Pathfinder instrument has a budget of only €256 million for 2024, compared to more than fifteen times that amount for the US Defense Advanced Research Projects Agency, known as DARPA. As a result of this investment shortfall, the return on EU investments is lower, diverting the bulk of venture capital and private equity funds away from the bloc.

What does Atlantic like about Draghi’s report? A lot of items, especially tidbits like the following:

…the report recommends that the EU accelerate the creation of the Capital Markets Union, which would create a pan-European space for the financing of high-tech investments that typically require equity rather than credit as a source of funding.

And:

the Draghi report argues that the EU needs to adapt competition rules to help foster the scaling up of firms in strategic industries, such as advanced manufacturing and robotics.

What are those competition rules and other laws that need overhauling? We wrote about back in October after the release of Draghi’s report, but to briefly recap:

- Less labor law for “innovative” companies.

- Free rein for AI and tech start ups.

- Less sovereignty.

- More “disruption.”

- Learn from hyper-globalization which decimated labor by embracing AI which will decimate labor.

- Overhaul education “skills investment” with a focus on training workers to become more productive tools for capital.

- And more public money supporting all this “innovation.”

We can see what the Atlantic Council is angling for:

All of those proposals would open up opportunities for US private investments in the nascent European digital market. At the same time, transatlantic cooperation in science and research and development—for example, through joint US-EU initiatives in sectors such as artificial intelligence, semiconductors, biotechnology, and aerospace—would enhance both economic resilience and security.

It’s no wonder that the Atlantic Council’s benefactors are licking their chops though. There’s plenty of untapped wealth to get to if the EU makes the right adjustments. As Ursula put it while speaking at Davos:

European household savings reach almost €1.4 trillion, compared with just over €800 billion in the United States.

Will all this wealth invested help the EU overcome its structural dependence on foreign companies for raw materials and components or will it simply funnel money to US giants?

In particular, harmonizing transatlantic regulatory frameworks for carbon pricing, emissions standards, and renewable energy integration would be essential for companies to operate on both sides of the Atlantic and infuse much-needed investment into the market.

…Harmonizing investment rules between the EU and the United States, improving regulatory frameworks, eliminating nontariff barriers, and increasing mutual access to services, procurement opportunities, and digital markets, would thus be a great source of economic growth for both the US and EU economies.

The EU-US Trade and Technology Council is already hard at work getting EU regulations in line with American interests. It’s highly questionable whether all this would benefit EU economies or help cement their dependence on the US. It’s never addressed how the EU is supposed to catch up on AI, chips, and other energy intensive tech while dealing with an energy crisis with no end in sight. In addition to the disadvantages the EU is already experiencing with energy, subsidies and a lack of coordination among members, the increased military spending that the US is pushing and Europe acquiescing to will likely divert money away from investments in any homegrown technological development.

Throwing more money at tech development without dealing with the bloc’s energy, security, and economic dependence on the US will mean that said investments are more than likely directed toward strengthening US grip over Europe.

Why focus on a relatively run-of-the-mill piece from the Atlantic Council?

Well, it, like all the Washington think tanks, is funded by and synthesizes the wishes of the American oligarchs into refined, smart-sounding policy prescriptions. Boil it down, though, and it’s just more plunder of the social commons.

And who are some of the Atlantic Council’s biggest backers?

You could catch a glimpse of them sitting and grinning in “Billionaires Row” at Trump’s inauguration: Mark Zuckerberg, Jeff Bezos, Sundar Pichai of Google, and Tim Cook of Apple.

No wonder Trump beamed into Davos to lambast the EU for trying to regulate US tech firms operating in Europe. Colonies don’t get to write the rules.