Yves here. This post addresses the question of what all of the European political realignments-in-progress might mean for fiscal policy, as in the level of deficit spending, and the composition of that spending. There’s been a lot of handwaving about populists, for instance, yet oddly less discussion of what their budget priorities might be This post considers various policy priorities and how interest payments will put pressures on what can be done. Strangely, or perhaps positively, I don’t see increased military expenditures being treated as a significant potential commitment.

By Carlo D’Ippoliti, Professor of Economics, Sapienza University of Rome and Editor, PSL Quarterly Review. Originally published at the Institute for New Economic Thinking website

The most crucial issue in European policy, and one on which no big party campaigned and no important public discussion took place, was the fiscal policy stance for the next few years.

Many observers think that the snap elections in France are the most important consequence of the recent European Parliament elections.[1] This conclusion is drawn from the projections that an alliance of the Christian-democrat conservatives (European People’s Party, EPP), the free-market liberals (Renew), and the Socialists and Democrats (SD) would amass 400 seats in a 720-strong European Parliament, enjoying a majority of 45 representatives (MEPs). Apparently, despite the big gains for the far-right parties,[2] the same parties that have governed Europe over the last decades will continue to do so.

At the national level, the ‘black wave’ has delivered a crushing defeat for the parties of Germany’s Chancellor Scholz and France’s President Macron. The latter immediately called for national elections, which in all likelihood will lead to a collapse of his centrist political movement. This will indeed be a major political event, but a difficult ‘cohabitation’ between a centrist president and a yet unclear majority of different color(s) will probability lead more to immobility than to dramatic policy shifts. And as the Italian example shows, even a radical party once in power in a large EU country faces formidable barriers and checks to Hungary-style authoritarian developments. Meanwhile, in Germany, Scholz has refused to subject himself to a confidence vote in parliament, and though his governing alliance has diametrically different views on the budget for the new year (and the next ones), all its parties lost big at the EU elections and are not looking forward to fresh ones.

If both France’s and Germany’s (after Italy’s) governments should come to be led by far-right parties, it could have relevant consequences. But we are far from there yet, and in the meantime, there is a case to be made that many observers are probably obsessing too much about the national consequences of the European vote and not enough about the EU-wide consequences.

A majority of 45 MEPs could possibly be enough to (re)elect the new European Commission, the executive branch of the EU, but it would not be sufficient to pass new acts of consequence, because MEPs tend to cast their votes according to national interest as much as political affiliation. Despite common manifestos and election platforms, groups in the European Parliament are less cohesive and influential than political parties at the national level, and a scenario in which the three main parties would have to craft variable alliances in each vote, depending on the issue at hand, is not unlikely. That is, if they do not choose (and manage) to coopt a fourth party in the EU governing coalition in the first place.

Observers are reading the tea leaves of the far-right parties’ political-economic preferences, looking for clues on what could be their position in case some of their votes should be needed in Parliament. But it is more useful to understand the points of internal division within and between the mainstream parties, and where they could find support from the other parties on the main issues. This is possibly a bigger source of uncertainty about Europe’s future policies than the extravagance of racist and nationalist parties that share little in terms of European policy and are even divided into different groups in the EU Parliament.[3]

During the European parliamentary campaign, national themes took center stage as usual. But this time, a number of European topics came to prominence too: at least migration and refugees, and the green transition. On these topics, the big European political families distributed themselves on a typical left-right dimension. For example on climate change, the far right advocated that there must be no costs for families and businesses (ignoring climate change deniers here); the conservatives proposed that the green transition should respect the timing and requirements of European industries (blink blink); the social democrats argued for beefing up the Green New Deal, and the Greens signaled that they are ready to reelect Ursula von der Leyen as president of the Commission if she does not backpedal on Europe’s climate commitments. The green transition is so divisive that the three mainstream parties will likely decide not to ask for the public support of either the greens or the far right and will try to go alone possibly with a ‘little help’ like five years ago (the election of the Commission president in the EU Parliament happens by secret ballot).[4] It will be informative, in this sense, to see who the European Council appoints as candidates for the top jobs, and how well they will do in their confirmation hearings.

However, possibly the most crucial issue in terms of European policy, and one on which no big party really campaigned and no important public discussion took place, was the fiscal policy stance for the next few years.[5] This topic is crucial for Europe’s ability to preserve the welfare state, implement the green transition, and catch up with the other main economic areas in terms of innovation, employment, and competitiveness. Suffice to cite one number: according to estimates, the EU member states might have to embark on four years of fiscal consolidation for up to 1% of GDP every year, or for seven years for up to 0.6% every year (depending on the country).

This in a high interest rate environment, in which just rolling over debt will be more costly and challenging than in the past decade. Clearly, if this is the way the fiscal rules will be enforced, there will be little space for industrial policy, the green transition, or the management of migration flows. And there is an issue of timing too: on July 16 the Economic and Financial Affairs Council (Ecofin, the board of finance ministers of the EU) will debate which countries do not conform to the new fiscal rules and should be put under an Excessive Deficit Procedure (read: more austerity);[6] in the same week, the European Parliament is expected to vote in the new Commission.

But fiscal policy is also interesting because the main political families are more internally divided and not easily located along a left-right line. For the single member states, the direction of movement was foreshadowed by last winter’s reform of the Stability and Growth Pact (that too moved through without significant debate), which reintroduces the specter of austerity after the COVID crisis-induced break for public finances. This movement could be slow or fast, and how much belt-tightening will be required is on the table.[7]

Some flexibility exists at the EU level, where the 2020 joint response to the COVID-crisis in terms of collective debt issuance for the sake of investments and recovery (the “Next Generation EU”) broke with a previously untouchable taboo. Today there is a clear need for investments – from energy to defense and Ukraine, to innovation and healthcare, not to speak of the remote but not impossible event of EU enlargement to cash-needy countries such as Ukraine and Moldova. And there is a growing understanding that at some point joint debt and expenditure instruments will be ineluctable. This too, however, comes with different proposals: from new EU-level taxes to the repurposing of legacy instruments such as the European Stability Mechanism, created during the previous euro crisis, or the Recovery and Resilience Facility and the other funds created during the COVID-crisis, which have substantial dry powder; to the issuance of new collective debt instruments.

In Europe, one must always consider both redistribution among individuals and among countries. Concerning interpersonal redistribution, let us consider two dimensions: parties’ positions on taxes (and social contributions, and other revenues in general, both national and pan-European), and on expenditures, with a focus on the welfare state.[8]One can then locate the main European families as in the table below.

The conservatives – the largest group in Parliament – will likely try to appeal to the liberals by proposing not to increase any spending program, and to woo the far right (and liberals) by opposing new taxes. Why this kind of agreement should appeal at all to the social democrats is a good question, but unfortunately many will embrace it, not just accept it. In the previous legislature, social democrats and the greens exacted a “Green New Deal” in exchange of this sort of agreement, trying to use (insufficient) EU resources to boost employment creation in new green industries. But the numbers in Parliament (and in the EU Council) were different then, and anyway, they were only successful after COVID produced the worst crisis in a century.

The positions set out in the table basically mirror those on the overall fiscal stance, because there is a wide, though not unanimous, agreement that taxation is very high in Europe, and the only concrete proposals to increase public revenues concern quantitatively small items such as international digital and financial transactions taxes, minimum taxes on multinationals, carbon taxes or import duties, and in some countries, property or inheritance taxes. While crucial elements of equity and fairness, all these are unlikely to raise sufficient revenue to meet the expenditure requirements of the day. Concerning expenditures, there is even less flexibility: debt service is going to increase; defense spending will have to increase regardless of the outcome of the US elections; and when Next Generation EU elapses in 2026, national funds will have to at least partly compensate for these vanishing EU investments. There will hardly be scraps for aid to Ukraine (except for what can be squeezed from frozen Russian assets) and investments for the green transition or innovation.

We thus have two fronts: on the main diagonal, between the conservatives and liberals for a small government, and the left and greens for big government; and on the antidiagonal, between the so-called populists for bigger deficits and liberals and (alas) some social democrats for lower deficits.

The first question will possibly be decided on an issue-by-issue basis, sometimes thanks to a convergence of the left and the far right in an attempt to preserve social expenditure and protect the welfare state. But levels of public deficits and debts are a macroeconomic issue and must be decided once, at least for a whole year. Here there is less scope for improvisation and flexibility, except in moving between the national and the EU levels.

As shown in the table below, we can expect some fiscal austerity at the national level and possibly some fiscal stimulus (probably not too soon nor too much) at the EU level – but probably not before a lot of social and economic pain and a good deal of soul-searching, EU-style. On the EU-level budget, the traditional political families are even more divided along ideological and national lines than on most other topics.

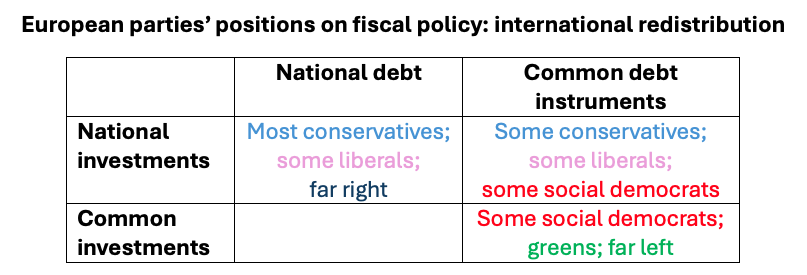

The conservatives traditionally oppose common debt because of fear of moral hazard, but over time a myriad of proposals have been put forward, of joint bonds that do not necessarily imply risk-sharing; and some conservatives are starting to accept the idea, e.g. if debt can be sold to their voters as an investment in security and defense. The liberals are traditionally even more opposed to debt (public debt, that is), but with Macron steering in the opposite direction in the name of Europe, it will have to be seen what happens now that he is seriously weakened.

The far right, as mentioned, has a menu of new expenditures and lower taxes and should therefore favor any easing of the financing constraint for member states.[9] However, they mostly end up rejecting common debt, due to their nationalist and anti-European stance. Finally, Eurobonds and common investments are the backbone of left economic platforms in Europe, but not all social democrats happily jump on board. So unless (or until) a new crisis hits, despite all the talk about existential crisis and a “mortal” European Union, the most likely scenario remains more of the same: that is, tight controls on national finances, and mild and insufficient expansion at the EU level. Among other things, this implies that the EU continues at least for a while to not compete seriously with the USA and China, not investing in industrial policy or the green transition.

On this front, the far right could be a main risk factor, but in both directions. A strong confirmation of Le Pen in France and a favorable deal with Italy’s Meloni could shift several votes in Parliament in favor of common debt issuance, but a government crisis in Germany could lead to a new government even more to the right and more opposed to Eurobonds than the current one. Ultimately, since most problems on the road to Eurobonds have emerged in the EU Council, where national interests are more strongly defended than in Parliament, and since the French elections will not likely shift Macron’s position on this point in the direction of more opposition to the idea, it still seems that the mainstream parties’ positions remain the biggest factor to consider here.

In conclusion, it is crucial to understand what far right parties and especially their voters want, as the recent elections look very much like a vote for a change and something radically different from the status quo. But to predict the course of policy, it is more useful to look at the realignments within and between the mainstream parties.

Notes

[1] This conclusion is possibly inspired by a typical undervaluation of the scope, reach, and importance of the European Union, as well as of the percentage of new regulations and norms that its member states enact directly as a consequence of, or implementing, EU rules. The Union is effectively on a slow but steady path toward becoming a fully-fledged federal entity, and after the euro and Brexit, this path is probably irreversible.

[2] Split into two different groups: the euro-skeptic Conservatives and Reformists, ECR, led by Italy’s Meloni, and the super-euro-skeptic Identity and Democracy, ID, dominated by France’s Le Pen.

[3] Indeed, the focus on the far right is leading both markets and policymakers to overreact. The Bank of France governor’s words, “it will be important that, whatever the outcome of the vote, France can quickly clarify its economic strategy and in particular its budgetary strategy” are very ambiguous in a democracy. But they were clearly prompted by the market’s nervous reaction to the announcement of snap elections. Incidentally, markets’ overreaction is a feature of the European economy, which by design lacks an effective central government and likes to tie the hands of its central bank as much as possible.

[4] In the European Council, which proposes the President for confirmation by Parliament, the greens and far left are not represented, while the far right has one vote or more, depending on how one defines it. Even in case of a far-right win in France, Mr. Macron as President of the Republic would still represent France within the Council.

[5] Knowing that the European Central Bank will then take the opposite stance: continuing to reduce interest rates if governments cut their deficits, and holding or even raising them if they don’t.

[6] The Commission just established that seven countries (Belgium, France, Italy, Hungary, Malta, Poland, and Slovakia) have an excessive deficit. The Ecofin will vote on which of these should be subject to the excessive deficit procedure. Among other considerations, some of the operational criteria of the new fiscal rules have not yet been finalized (e.g. the path of “net expenditure”) providing yet some more flexibility in this transitory phase.

[7] The new rules allow for a minimum degree of flexibility – though less so for the most indebted countries, which happen to be large Eurozone countries with economies that are more driven by internal demand than the others.

[8] The welfare state, that is, for EU citizens. The welfare chauvinism of far right and red-brown parties that propose to cut entitlements for immigrants is a serious matter of identity and racism but of little consequence for the public purse.

[9] Italy’s and France’s far right even more so, given the weight on their countries’ national public finances.