Perhaps lost in the shuffle this week amid an aborted coup in South Korea, Syria, genocide, the collapse of the French government, elections annulled in Romania over TikTok videos, and Biden’s pardons was the step taken by Beijing in the trade war that Washington is determined to keep escalating. And should China go further, it could ultimately force the US to begin scaling back its military operations and support for proxies across the globe.

That’s because the US — and its and its vassals’ militaries — are dependent on China for a range of minerals which China is increasingly restricting access to in response to US economic warfare. In this case it was Washington’s latest effort to cripple China’s chip industry.

Beijing responded with what amounts to another warning shot. It banned exports to the US of the critical minerals gallium, germanium and antimony and requires stricter review of end use for graphite items. Announced on Tuesday, they strengthen enforcement of existing restrictions on critical minerals exports to the US that Beijing began rolling out last year.

Chinese antimony restrictions were already put in place back in August and have since dropped 97 percent. And unwrought germanium or gallium was already under unofficial restrictions as none had been sent to the US for a year. Formalizing the curbs is another step up and intended to send a message — one US officials seem unwilling or incapable of receiving.

America’s plutocrat-funded think tanks expect the US to continue pushing ahead with more tariffs and technology restrictions. And the Chinese could counter with tighter controls on more strategic minerals.

Beijing has plenty of other options, and its updated framework will also reportedly allow it to quickly and effectively implement new export bans on other strategic minerals on the list. According to the AP, it is believed that next on the list of potential bans are tungsten, magnesium and aluminum alloys. All Beijing needs to do to really put the squeeze on the US is start moving its way up the following chart. If it gets to the 16 critical minerals under the rare hearts umbrella, Washington could be in big trouble.

As Al Jazeera reports, gallium and germanium are used in semiconductors while germanium is also used in infrared technology, fibre optic cables and solar cells. Antimony is used in bullets and other weaponry while graphite is the largest component by volume of electric vehicle batteries. Here’s a brief breakdown on what a wider range of minerals are primarily used for:

And all the US proxy wars, already facing shortages from the “arsenal of democracy,” could be ground to a halt due to mineral disruptions. Here’s the Modern War Institute at West Point sounding the alarm on the problem while simultaneously (and hilariously) calling for preparations for conflict with China:

The US military is attempting to quickly replenish diminished weapons stocks in its largest production ramp-up in decades. With an eye on its pacing threats and the risk of major conflict—with China, in particular—it is transitioning to modern platforms, including attack submarines, heavy bombers, and air defense systems, as well as new approaches to electric vehicles. Given its security assistance to Ukraine and recent military support to Israel, and conflict risks with China, it is simultaneously rearming with legacy munitions—155-millimeter artillery, Javelin antitank missiles, and surface-to-air Stinger missiles. Because of the quantity of minerals required to meet these dual demands, for replenishment of munitions and construction of new platforms, both endeavors could be put at risk. Specifically, the mineral supply chains that the US military depends on could face overwhelming demand and possible supply disruption.

The Modern War Institute goes on to call for stockpiling, domestic mines, and mineral recycling.

Yet while Beijing continues to make advances in producing its own advanced chips — a process jumpstarted by US efforts to deprive them of such tech — the US is not making the same progress breaking China’s hold on strategic minerals.

In 2022, the US designated 50 minerals as critical to the economy and national security, including many used in military equipment. According to TD Economics, China dominates the global production of more than half of the critical minerals outlined by the U.S. government

China continues full steam ahead on its own enormous effort to secure mineral supplies for its industry and dominate the global supply chain:

Source: The Oregon Group

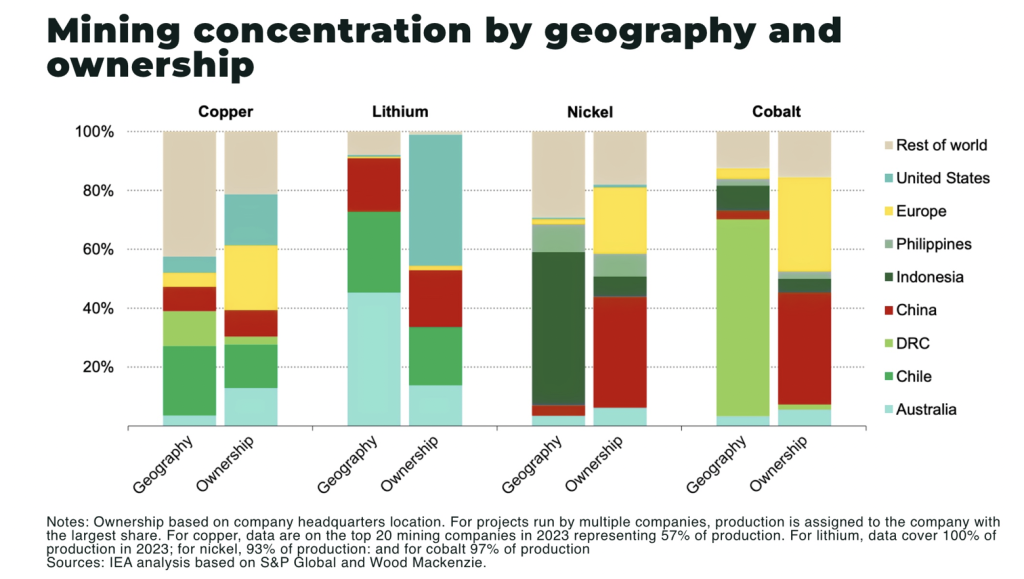

As we can see, however, the ownership of mines is still quite diverse:

Source: The Oregon Group

Where China really exerts its influence is on the refining, which it dominates. From The Oregon Group:

China accounts for approximately 85% of global critical mineral processing capacity. For example,

-

China dominates almost the entire graphite anode supply chain end-to-end

-

China processes nearly 90% of the world’s rare earths

-

over 60% of global processing for lithium and cobalt occurs in China

-

over 40% of copper refining is done in China, an increase from under 40% last year, and expected to increase to over 50% from 2030

Breaking that stranglehold is not easy nor fast. It can take five to ten years to get refining operations up and running. And yet there seems to be a belief among the policy makers and think tankers that the US will simply shift supply chains away from China, increase domestic production, and find new import sources.

The International Energy Agency is not among the believers in the US strategy. Its estimates show that almost half of the market value from refining will come from China by 2030 and continue to increase over the next decade from there. More from The Oregon Group:

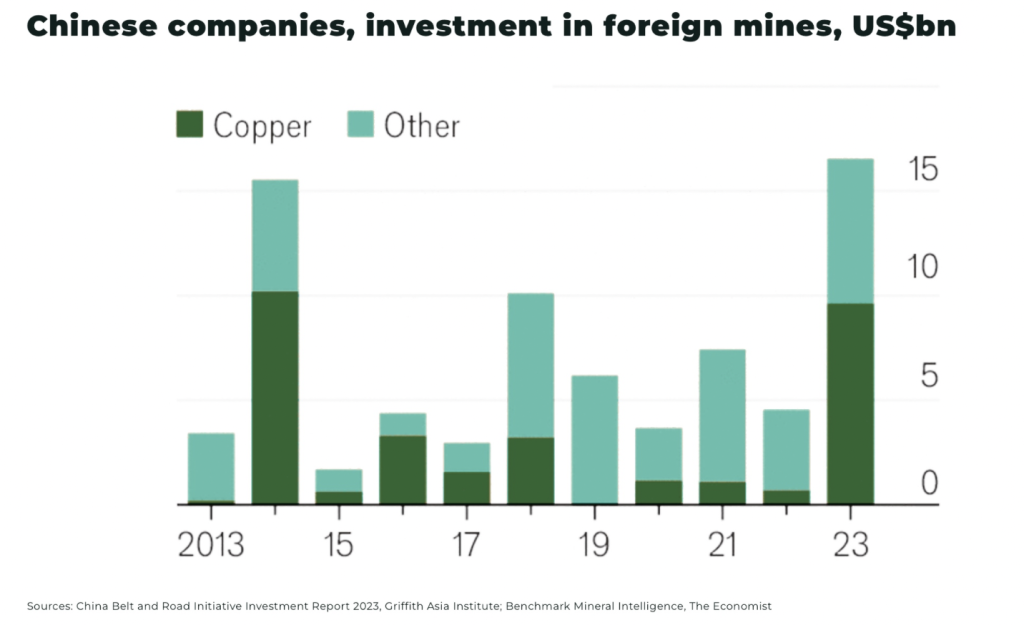

Spending by China on developing and acquisition of overseas mines hit a record US$10 billion in the first half of 2023, focusing on lithium, nickel and cobalt.

According to GlobalData, the number of planned mines owned by Chinese companies, under development or exploration, is set to double.

In many cases, the US and European companies helped China get to where it is now. From the Wall Street Journal:

For more than a decade, Chinese companies have spent billions of dollars buying out U.S. and European miners in Congo, which produces nearly 75% of the world’s cobalt supply. That has put China in a dominant position in both the production and processing of the mineral.

The Biden administration has pledged billions of dollars in investments in infrastructure projects across Africa, including a railroad intended to carry Congolese minerals such as copper and cobalt across Angola to the Atlantic Ocean port of Lobito. But it has been difficult for the U.S. government to interest American investors in any sector in Congo because the country’s poor infrastructure, limited skilled labor, resource nationalism, and reputation for government corruption.

The amusing fact that the US is incapable of building infrastructure because of a lack of existing infrastructure highlights a very real problem that makes it virtually impossible for Washington to overcome China’s dominance in refining. As Ian Welsh succinctly puts it, You Can’t Run Industrial Policy OR A War Economy Under Neoliberalism.

And so if we go back to the US trying to secure minerals from Africa, we see what one of the biggest hurdles is: US investors want more sweeteners from Washington before committing. According to the WSJ, those include financial support, insurance against expropriation or sudden tax increases, and waivers to the Foreign Corrupt Practices Act.

Elsewhere, companies like Perpetua Resources, which is developing the only US antimony mine in Idaho, are receiving massive government handouts in the name of national security.

It’s an arrangement that’s worth taking a quick look at. The largest shareholder in Perpetua is the former Wall Street hedge fund manager Paulson & Co., and the chairman of Perpetua is Marcelo Kim, a partner at Paulson.

If Paulson & Co. sounds familiar, that’s probably because it was in on the ABACUS investment, paying Goldman $15 million to put together a collection of toxic subprime securities sold by Goldman to long investors so that Paulson could bet against it. John Paulson, whose multi-billion payoff on that bet turned him into a superstar in some circles, later stopped managing money for outside clients and turned his firm into a family office.

Are these really the people the US is relying on to supply antimony necessary for the country’s beloved bullets?

It’s quite the reward for Paulson. Perpetua Resources gets a $1.8 billion low interest loan, the Pentagon is covering the permitting costs, once the Idaho mine is up and running Perpetua will have a monopoly on domestic supply of antimony, which also happens to be skyrocketing in price — up more than 200 percent this year.

It’s convenient for US policymakers to believe that by further enriching the wealthy and well-connected that will somehow unleash that famous American ingenuity and magically solve the problem, but there’s little evidence it’s working.

US overreliance on China has been known for some time and yet the problem never seems to improve. Seemingly every month there’s a new proclamation like “the recent discovery of lithium reserves in southwest Arkansas may enable us to reshape the balance of power in global mineral markets” while simultaneously rebuilding America’s “industrial base.”

Ah yes, the industrial base that each successive administration now tries unsuccessfully to bring back. The day after China unveiled its export restrictions, there was a hearing on Capitol Hill entitled, “The Imperative to Strengthen America’s Defense Industrial Base and Workforce.”

What does that look like? According to Responsible Statecraft, ‘witnesses proclaimed that deep-tech innovations including AI, autonomy, software and adjacent tech are vital to both the development of state-of-the-art weaponry but also towards the “hyper-scaling” of production processes key towards developing competitive arsenals.’ More:

The hearing’s witnesses may well believe their efforts bolster America’s competitiveness and national security in increasingly tenuous times. And yet, their affiliations suggest their efforts also line their pockets, all while advancing contentious AI-backed and autonomous military production and weapons systems.

What this strategy ignores is that by sweetening the pot for investors on Wall Street and in Silicon Valley, Washington is turning to the very same people who created the problem in the first place.

Key Point Memory Holed

You can read countless stories from the media and think tanks about the dangers of US reliance on China, and not a single one will mention how American financiers put the country in this position. For a refresher we can turn to a magisterial 2019 piece from Matt Stoller and Lucas Kunce at The American Conservative.

Their story of lost American leadership and production describes the destruction of America’s once vibrant military and commercial industrial capacity due to public policies focused on finance instead of production. Here’s the brief history:

Bill Clinton took the philosophical change that Reagan had pushed on the civilian economy, and moved it into the defense base. In 1993, Defense Department official William Perry gathered CEOs of top defense contractors and told them that they would have to merge into larger entities because of reduced Cold War spending. “Consolidate or evaporate,” he said at what became known as “The Last Supper” in military lore. Former secretary of the Navy John Lehman noted, “industry leaders took the warning to heart.” They reduced the number of prime contractors from 16 to six; subcontractor mergers quadrupled from 1990 to 1998. They also loosened rules on sole source—i.e. monopoly—contracts, and slashed the Defense Logistics Agency, resulting in thousands of employees with deep knowledge of defense contracting leaving the public sector.

Contractors increasingly dictated procurement rules. The Clinton administration approved laws changing procurement, which, as the Los Angeles Times put it, got rid of the government’s traditional goals of ensuring “fair competition and low prices.” They reversed what the New Dealers had done to insulate American military power from financiers.

The administration also pushed Congress to allow foreign imports into American weapons through waivers of the Buy America Act, and demanded procurement officers stop asking for cost data. Mass offshoring took place, and businesses could increase prices radically.

This environment attracted private-equity shops, and swaths of the defense industry shifted their focus from aerospace engineering to balance sheet engineering. From 1993 to 2000, despite dramatic declines in Cold War military spending and declines in the number of workers in the defense industrial base and within the military, defense stocks outperformed the S&P.

Stoller and Kunce’s conclusion:

In short, the financial industry, with its emphasis on short-term profit and monopoly, and its willingness to ignore national security for profit, has warped our very ability to defend ourselves.

That diagnosis assumed that the US national security industry exists to defend Americans, however. If we cast our gaze out over the world’s bloodstained landscape today where the US proxy forces of Nazis, jihadists, and Zionist genocidaires are busy setting the world on fire today, it’s hard to come to any conclusion other than the fact that we are the bad guys.

If that’s the case and the US defense industry is primarily a tool to spread freedom for the plutocrats to rape and pillage more of the earth, well, would it be such a bad thing if the Chinese took advantage of our ruling class’ greed to pull the plug?