by John Mauldin

The latest data shows inflation is still with us at an 8.5% annual rate. That means we can expect the Fed to keep tightening, trying to reduce demand and relieve pressure on consumer prices.

At the same time, we’ve seen declining GDP growth the last two quarters. Some people raise measurement issues. Fine. Grant that and you can say we have stagnant GDP growth. These weak numbers certainly don’t suggest an urgent need to “cool” the economy. But that’s what the Fed is doing.

Markets evidently think the Fed will stop hiking sooner rather than later. They are literally not paying attention to what multiple Fed officials are saying in speeches all over the country. Let’s look at what normally uber-dove Neel Kashkari says:

“The idea that we’re going to start cutting rates early next year, when inflation is very likely going to be well in excess of our target, I just think it’s unrealistic,” Minneapolis Fed president Neel Kashkari said.

He further stated that, “I think a much more likely scenario is we will raise rates to some point and then we will sit there until we get convinced that inflation is well on its way back down to 2% before I would think about easing back on interest rates.” He went on to state that the Fed “is far away from declaring victory on inflation, and while this is the first hint that price movements are moving in the right direction, it doesn’t change my path for rates.”

We have a name for concurrent inflation and recession: stagflation. That term arose in the 1970s when they had high unemployment, which (so far) isn’t a problem this time. But it was also a different demographic situation, with Baby Boomers reaching working age and more women able to enter the workforce. Labor supply was outpacing labor demand. Not so now—though this could change somewhat, we aren’t going to see those 1970s demographic circumstances again. This is new territory.

I’ve noted many times how past mistakes leave our economic policymakers with no good choices. The Fed is inducing recession—or at least amplifying it—in order to control inflation. The mechanism by which they are doing this is the yield curve. It is already deeply inverted and set to become more so.

I have written about yield curves extensively in this letter over the last 23 years. Yield curves as inverted as the current one have always predicted a future recession. Always. While stagnant GDP doesn’t feel like a recession to most of us, the inverted yield curve says we are going to get a recession that feels like a recession.

But if inflation also sticks around, the yield curve could look more like a yield whip over the next year or two—snapping loudly as it constantly adjusts to new events and interventions. Today we’ll revisit the yield curve topic as well as inflation and think about how they may behave going forward.

This Is Not Normal

We’ll start with a quick yield curve update. I last addressed this in my Curve Ball letter back in April. Much has changed in the subsequent four-plus months.

(Quick refresher: The Treasury yield curve is simply a graph showing government bond interest rates from the shortest maturity to the 30-year long bond. Normally, it slopes upward from left to right because inflation risk grows with time. As a lender, you face higher odds of loss if you tie up your money for 30 years than for six months. You demand a higher yield to cover that risk.)

Here is the yield curve graphic I shared in that April letter.

Source: GuruFocus

At that point, the curve rose swiftly from one month out to the 2–3-year area, then flattened. The 2-year/10-year interest rates were slightly inverted, which is the classic way a deeply inverted yield curve begins. It wasn’t yet sufficient to signal a future significant recession, but was definitely headed that way.

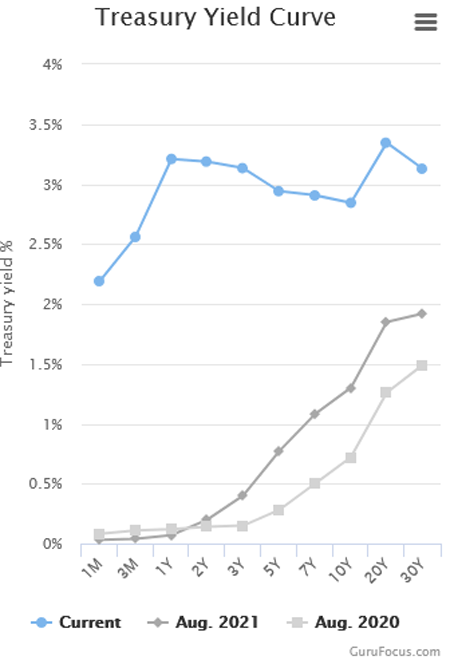

Here is how that same graph looks now.

Source: GuruFocus

Note the blue line begins above the 2% mark, instead of down close to zero as it did in April. One-year interest rates are higher than 30-year bonds. That’s an inversion and it’s not normal.

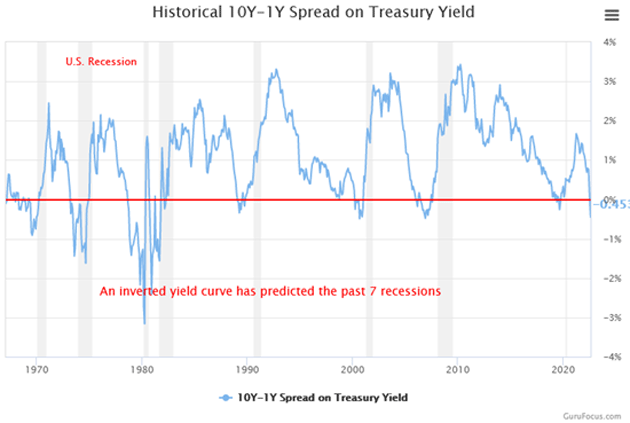

Here’s a different view, measuring changes over time in the “spread” between the 1-year and 10-year Treasury yields. When it goes below zero (i.e., the shorter-term bond yields more than the longer-term one) recession usually follows soon. That’s where we are now.

Source: GuruFocus

The Federal Reserve doesn’t directly control longer-term yields, but it has a lot of influence—mainly through its “quantitative easing” bond purchases. Those have ended and will soon reverse. This may raise the right end of the curve, making it less inverted, but we also have more rate hikes coming on the short end. It’s not yet clear how all that will shake out.

We are in uncharted waters. The Fed is raising rates into an inverted yield curve and has clearly expressed its intention to continue doing just that.

Recession Probability

This awareness that an inverted yield curve signals recession isn’t new, nor did it appear from thin air. My first economic mentor, the late Dr. Gary North, was teaching me about inverted yield curves in the early 1980s. To my knowledge, there was no real research, just anecdotal observational analysis, but it still held. Then my friend and economist Campbell Harvey, now at Duke University, first proved its forecasting accuracy in his 1986 University of Chicago doctoral dissertation. Others quickly confirmed and expanded on his conclusions.

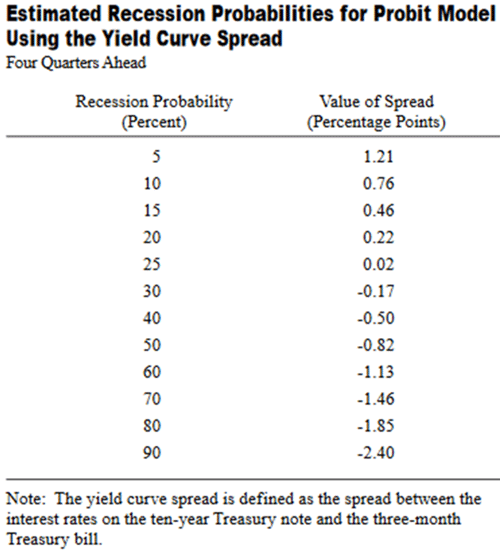

In 1996, New York Fed economists Arturo Estrella and Frederic S. Mishkin authored a paper comparing the yield curve to 19 other indicators and, importantly, finding a connection between the yield spread and recession probability.

To summarize, Estrella and Mishkin found the yield curve is most predictive of recession a year or so ahead of time. In fact, they concluded an inverted yield curve was the only useful predictor of recessions. Examining all the data from 1960‒1995, they calculated the probability a recession would occur four quarters ahead, based on the spread between 3-month and 10-year Treasury securities. They summarized it in this table.

Source: New York Federal Reserve Bank

Let’s look at the actual yield curve as of Friday morning (August 12th). The 2-year/10-year spread is a negative 0.32%. That is better than last Friday which was a negative 0.42%.

Source: Bloomberg

Well then, what am I worried about? That’s only a 40% chance of a recession. Except every time we have reached this point in the last few decades, we ended up having a significant recession, as in 2001 and 2007.

The yield curve is flashing a strong recession signal three to four quarters out. What makes this curious, and a little more difficult to predict, is that we already have a stagnant/negative growth with two straight quarters (if revisions show Q2 still negative) of declining GDP.

Inversions typically precede recession by anywhere from a few months up to two years. The yield curve is usually back to normal by the time recession actually arrives. But nothing about all this is “typical” so maybe this time is different.

Or more likely, the real recession is still coming.

Rough Transition

One of the mysteries presently vexing us is why long-term yields haven’t risen more, given the very high inflation we are enduring. Bond investors seem to have a great deal of faith that the Fed, or something, will make inflation recede sharply and soon.

I have learned to be very cautious in saying “the market is wrong,” because it usually isn’t. But on this point, I really think the market is wrong—possibly because it is no longer a “market” in any meaningful sense. So much intervention for so long has turned it into something else.

Last week my friend/business partner Steve Blumenthal flagged a report from Bridgewater’s Bob Prince on “Transitioning to Stagflation,” an ominous but probably accurate title for where we are headed. Here’s the core of it.

“We are still in the early stages of this transition, and the path will depend a lot on how central bankers play their difficult hand, so one should not be firmly committed to one scenario or another. But as things now stand, odds favor a stagflationary environment that could last for years.

“[Monetary] policies were very successful, stimulating a high level of nominal demand and a rapid recovery in employment markets in response to the pandemic. But this stimulation was applied for too long, and the offsetting monetary tightening is now coming too late, resulting in what we now have, which is a monetary inflation. Given the inertia of a monetary inflation, bringing it under control to the point that inflation approaches what is now discounted in the markets (2.5%) will require an aggressive tightening of monetary policy over a sustained period, and a significant and sustained weakening of employment markets. As central banks pursue their dual mandate of maximum employment and stable prices, they will not be able to achieve both at the same time and will be forced to choose between too-low growth in order to achieve their desired inflation rate, or too-high inflation in order to achieve their desired employment conditions. In managing through this, we see them toggling back and forth in their prioritization, trying to avoid both an unacceptably deep economic contraction and an unacceptably high inflation rate, culminating in a long period of too-high inflation and too-low growth, i.e., stagflation.

“The markets are discounting a very different scenario. They are discounting one sharp round of tightening—comprised of a rise in short-term interest rates to just above 3%, combined with more than $400 billion of contraction of the Fed’s balance sheet—and that this will be enough to bring inflation down to 2.5% with stable growth and no dent in earnings. From there, markets are discounting that the achievement of these goals would allow a subsequent 1% drop in rates from their peak.

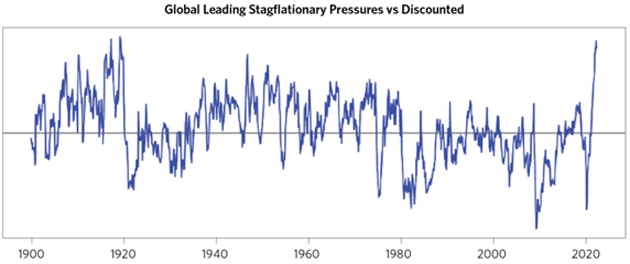

“Asset returns are driven by how conditions unfold in relation to what is discounted. Our approach is to have an excellent reading of current conditions and a time-tested understanding of the cause/effect linkages, leading to a reliable probabilistic assessment of what comes next: an optimal response to known conditions. Today, our indicators suggest an imminent and significant weakening of real growth and a persistently high level of inflation (with some near-term slowing from a very high level). Combining this with what is discounted, the difference between what is likely to transpire in the near term and what is discounted is the strongest near-term stagflationary signal in 100 years, shown below. Longer term, as we play it out in our minds, we doubt that policy makers will be willing to tolerate the degree of economic weakness required to bring the monetary inflation under control quickly. More likely, we see good odds that they pause or reverse course at some point, causing stagflation to be sustained for longer, requiring at least a second tightening cycle to achieve the desired level of inflation. A second tightening cycle is not discounted at all and presents the greatest risk of massive wealth destruction.”

Data estimated through June 2022. Estimates based on Bridgewater analysis.

Source: Bridgewater Associates

The Bridgewater report goes on to describe how all this tightening will unfold and what it needs to do in order to bring inflation down to the 2.5% area. They expect about two more years of tightening to reach that point.

Markets aren’t priced for anything like that scenario. This means, among other things, mortgage rates will continue to choke the housing market, with substantial knock-on effects including many lost jobs.

That won’t be an accident. It’s what the Fed wants.

Whither Inflation

My friend and Duke professor Campbell Harvey (the same Campbell Harvey who wrote that 1986 paper mentioned above) recently did a

Source: Rob Arnott and Research Affiliates

Will the FOMC say “mission accomplished” at 6.5% inflation? What happens if we get a recession in 2023 like the yield curve is predicting? Do they lean into the recession or keep fighting inflation? Bob Prince thinks (like a lot of other smart people) the Fed will worry more about the recession and cut rates, letting inflation stay uncomfortably high but believing that an actual real recession will be enough to bring down inflation as demand will get crushed across the board by a recession.

Stagnant or negative growth and high inflation? It takes us back to stagflation, which is a very difficult economic situation for businesses and investors to deal with. If, as Prince and others suggest, the Fed then resumes its fight against inflation after the recession has ended, the ensuing financial bear market could be much worse than what we have seen now.

The problem is there are a lot of “ifs” in those assumptions. What if the Fed does not take its foot off the brakes in 2023 and simply says we have to stop inflation. Interest rates on the short side will be in the 3.5 to 4% range. Will they pause? Or continue on with their inflation-fighting march? The simple answer is none of us know. And frankly, I don’t think anybody in the FOMC including Jerome Powell knows what they will do either until they get to the situation. They really are data dependent.

Waking to a Nightmare

How this goes depends a lot on the next few economic reports. Currently the federal funds rate, the Fed’s primary policy rate, is at 2.5%. It will likely be at least 3% after the September meeting, maybe higher if August inflation and jobs data remain strong. It’s easy to imagine 4% by year-end if inflation isn’t falling fast enough. They need to get real rates to a positive number, at least, and that is probably a lot higher than 4%.

A yield curve starting at 4% and bending down to 2.5% 10-year yields is possible, I suppose, but I can’t imagine it staying that way very long. Some combination of yields needs to move differently.

One possibility is long-term yields rise, restoring normal slope to the yield curve. That would mean higher mortgage rates, with all the attendant economic damage, as well as higher interest costs on the federal government’s gargantuan debt. Hardly benign—but quite possible with QT about to begin in earnest.

More typically, the short end of the curve moves down, which would mean the Fed stopped hiking and maybe even cut short-term rates. I think this is both more likely and more dangerous. Fed officials know they can’t let inflation get out of control. But they also want to see a “soft landing” for the economy. I see high risk they will take some kind of “pause” in the rate hikes later this year. They’ll say they want to reevaluate data, blah, blah, blah.

This will grow more likely if unemployment rises. I mentioned productivity a few weeks ago and relayed the story of United Airlines needing to hire 4‒5% more workers just to cover absentee and sick workers. I’ve since seen several similar stories. The Labor Department also updated productivity for Q2, revealing the worst quarterly drop since 1948. That’s terrible for many reasons, but it could sustain hiring activity. (And it won’t be good for earnings, as productivity has been the driver for much of the earnings growth for the last 40 years.)

Another scenario—which is possible, though I think unlikely—is a substantial improvement in inflation. It would almost have to include a big drop in energy prices that didn’t spring from recession-induced falling demand. I can’t imagine what would do that. I can more easily imagine the opposite as Europe faces a long, cold winter.

Tossing all that around, I think extended stagflation is our most likely destination. I don’t believe the Fed can produce a soft landing and I see no reason to think inflation will ease back to 2019 levels in 2023. Further out? Absolutely. I still believe in my low inflation/deflation scenario over the longer term. That means slow growth, given our debt situation.

The government and the Federal Reserve’s policy errors created the current situation. I see many more opportunities for policy error in the future, with potential results ranging from bad to calamitous.

But these things unfold slowly. We could easily get a few good months that lull everyone to sleep. If so, we may wake up to a nightmare.

The Cleveland Clinic and British Columbia

Sunday, I leave paradise to travel to the Cleveland Clinic where I will spend three days being probed and prodded, scanned and stress tested. Normally, it takes 1‒2 days depending on whether they do a colonoscopy or not. I’m having to spend extra time due to some eye issues. My partner Olivier Garret just came back from his third session and he was raving about the Cleveland Clinic. I echo that sentiment. After a certain age, we all need semiannual deep physical exams. If you don’t have a major executive health program near you, you might consider coming to the

John Mauldin

Views: 23