It was awfully conveniently timed that Trump announced the establishment of a “strategic” crypt fund in the middle of a crypto market sad that could have turned into a rout. As anyone with an operating brain cell knows, there is zero reason for a sovereign currency issuer like the US to hoard baseball cards crypto, particularly given its lack of use in the real economy for much beyond tax evasion, paying criminals, and money laundering. This is simply a particularly obvious payoff to a key group of Trump election campaign supporters, for an activity with not only no value, but actual negative consequences: facilitating crime, reducing tax receipts, diverting investments out of productive activity into speculation.

And this handout is taking place as Musk and DOGE are going on their ideologically-driven rampage though the Federal apparatus, routinely going well beyond their claim to be cutting fat and hacking out muscle, bones, and organs. See the post yesterday on the cost-cutting at the USDA, which seems guaranteed to hurt farmers and lower agricultural output. And the dumb chump public is supposed to applaud? When food prices are already seen as too high? Instead of the purported Klaus Schwab globalist “Eat zee bugs” scheme, we are seeing the direct operation of Lambert’s Second Rule of Neoliberalism: “Go die!”

But this grotesque handout actually represents continuity of policy, but with characteristic concern about plausible deniability, as in ability to posture about broader benefits. As we’ll describe below, there’s a long, proud history of seemingly cost free or low cost financial market subsidies to pet party backers on both sides of the aisle. Sometimes they actually have benefitted interest groups which support both political parties because they have the financial means to do so and have policy interests they want to move forward regardless of which party is in charge.

And that’s before getting to other elements of the lack of justification for the program (save the enriching friends of Trump part):

A U.S. crypto reserve makes no sense. No clear purpose, contradicts decentralization, opens laundering loopholes, concentrates control, chokes innovation, and feels like a slush fund or ETF setup for institutional bailouts. If crypto is decentralized, why centralize the reserve?

— Michael Gogel (@mgogel) March 2, 2025

But first, an overview of the crypto bro payoff scheme. The Financial Times headline flags that everything is going according to plan. From Crypto prices jump as Trump names tokens included in strategic reserve:

A reserve has been championed by crypto traders, who believe something akin to Fort Knox for gold — which would buy and hold bitcoin — would offer legitimacy to the asset class.

Proposals are already working their way through state and federal legislatures. One Republican-backed Senate bill seeks to direct the US Treasury to buy 1mn bitcoin, worth roughly $94bn based on current market prices.

The bills have faced opposition, including from some Republican lawmakers who say they put taxpayers’ funds at risk, and the reserve itself will raise concerns over potential conflicts of interest. Some Trump advisers have investments tied to the market….

Bitcoin rose as much as 11 per cent to $95,084 on Sunday before retreating slightly to $93,165 on Monday, while ethereum gained as much as 14 per cent to $2,541, before falling to $2,448 on Monday.

Solana, the token that represents the blockchain that hosts most memecoins — including Trump’s own coin, climbed 26 per cent to $180 but fell to $170 on Monday.

Ada, which represents the cardano blockchain, soared 71 per cent to $1.15 per token on Sunday. XRP, the coin affiliated to payments group Ripple, rose 37 per cent to $3.

The comments at the pink paper ranged from incredulous to scathing. A few examples:

Un addition to the bad optics of handouts to campaign backers, we have top Trump officials feeding at the trough:

Jaw-dropping corruption in the US:

Trump’s billionaire crypto czar is heavily invested in a fund whose top 5 holdings are the 5 in the US government Crypto Strategic Reserve.

Mere hours before Trump announced it, someone bought $200 million in Ethereum & Bitcoin on 50X LEVERAGE pic.twitter.com/LQWZceeTvB

— Ben Norton (@BenjaminNorton) March 3, 2025

We’re all going to pay more in taxes to fund Sack’s exit from his crypto positions.

— Parker Conrad (@parkerconrad) March 2, 2025

David Sacks is up there among the biggest pieces of shit in the US

He literally cried for the government to save his bags when SVB collapsed…now did it again with his crypto fund

He’s a shitstain on America. The day he finally ends up in jail should become a national holiday https://t.co/PqMQaoI9RW

— Rho Rider (@RhoRider) March 2, 2025

Only one conservative Trump supporter has come out and said what an insane grift the Crypto Strategic Fund is as far as I can see

But 99% of them are thinking it but are too scared to disagree with Trump

Let’s pause: If you’re too scared to challenging the President when he… https://t.co/uCwYVyJW2T

— @jason (@Jason) March 2, 2025

We are pained to point out that this sort of grift has a proud history, particularly in recent years, although with the “cash for friends of buddies of the Administration” part a wee bit less obvious.

Let’s start with some original sins that pretty much everyone in the general public is unaware of: massive subsidies via underpriced insurance, which includes policies that allow market participants to set aside unduly low risk reserves. The mother of all is underpriced FDIC insurance. This is particularly troubling since many banks park their derivatives exposures in their FDIC insured entities. Now admittedly some “derivatives” like interest rate and foreign exchange swaps in major currencies are pretty plain vanilla. But after the crisis, and it appears to be continuing, there’s not enough official minding of this risk store.

Since the crisis, regulators in the major economies have made a concerted effort to move derivative transactions to central counterparty clearing houses for derivatives transactions. The theory is to reduce counterparty exposure and thus contagion in a crisis. However, the risk reserves in these clearing houses are margin posted on particular exposures. The margins are set too low because (you cannot make this up!) professionals claim that derivatives would become unaffordable if the margins were set high enough to cover the true risks. The official posture is that these clearing houses are not backstopped. No one in the markets believes that. In a crisis, they are sure to be treated as too big to fail.

Thanks to deregulation of the financial services industry, many activities that once were limited to banks moved to institutions that competed with banks without paying FDIC insurance. Money market funds are the prime example. During the financial crisis, the posture of government shifted from protecting the banking system to protecting an ever-growing list of market participants. Perry Mehrling has described the change in posture as going from “lender of the last resort” to “dealer of the last resort”. So in the crisis, money market fund holders got a massive gimmie via suddenly being guaranteed up to $250,000, just like FDIC depositors, to prevent runs on money market funds after a large fund, Reserve, famously “broke the buck” via holding subprime asset-backed commercial paper.1

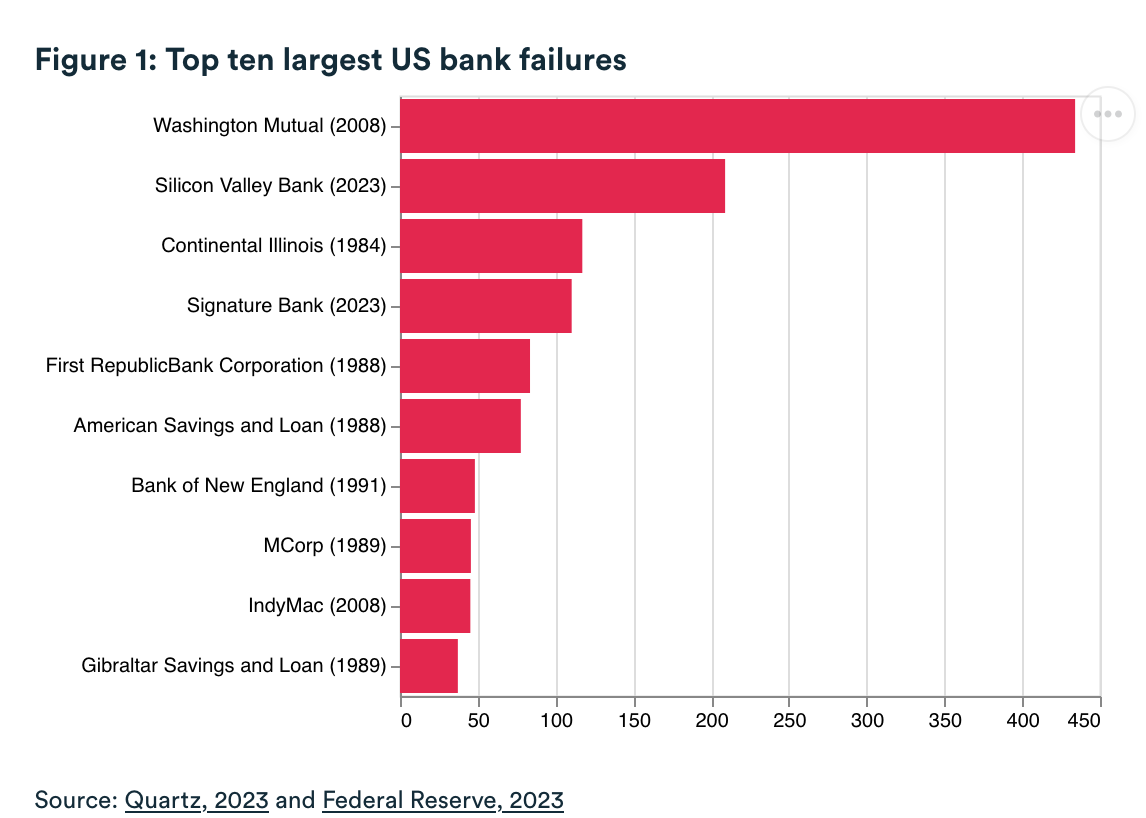

Back to the question of deposit guarantees. During the crisis, uninsured depositors at smaller banks that had big subprime origination business and failed with a lot of bad loans in their pipelines (as in set to be securitized) like IndyMac and New Century were not rescued.2 Fast forward to the recent shift from that policy with the unseemly salvation of uninsured depositors in the above mentioned SVB, Silicon Valley Bank and the crypto-catering Signature Bank.

To make a long story short, Silicon Valley Bank was too connected to fail. The excuse for the bailout of its unsecured depositors was that there were companies that had payroll on deposit and wiping that out would stiff the workers and potentially ruing the companies. While it is true that companies of any size pretty much always have more cash at their bank than deposit guarantee limits,3 no one harbored such tender concerns for the companies that had the misfortune to be IndyMac and New Century customers. Nor did anyone then or later suggest creating a special bailout facility solely to protect these companies’ funds. But those venture capital investees are so much more special than other businesses.

And despite those crisis wipeouts, no one suggested restoring the Fed payments facility to allow companies to hold pending payroll payments safely at the central bank. God forbid the prospect of competition or risk reduction!

Admittedly, another widely recognized but not-officially-admitted rationale was the wobbly state of many mid-sized and pretty big banks, due to a combo of wrong-footing the sudden Fed interest rate increases (as in having serious but not recognized interest rate losses) and/or having meaningful exposures to commercial office space, which were expected to show credit losses as current tenants did not renew leases as a result of “work from home” persisting beyond the Covid crisis.

But the biggest driver was that Silicon Valley Bank was too connected to fail. There were company executives that claimed that after receiving venture capital funding, they were required to conduct all their payments activities through Silicon Valley Bank so that the VCs could spy on them on an ongoing basis. Even more important, the venture capitalists themselves (the firms and their principals) had very large balances at Silicon Valley Bank. Peter Thiel said he had $50 billion “stuck” there.4

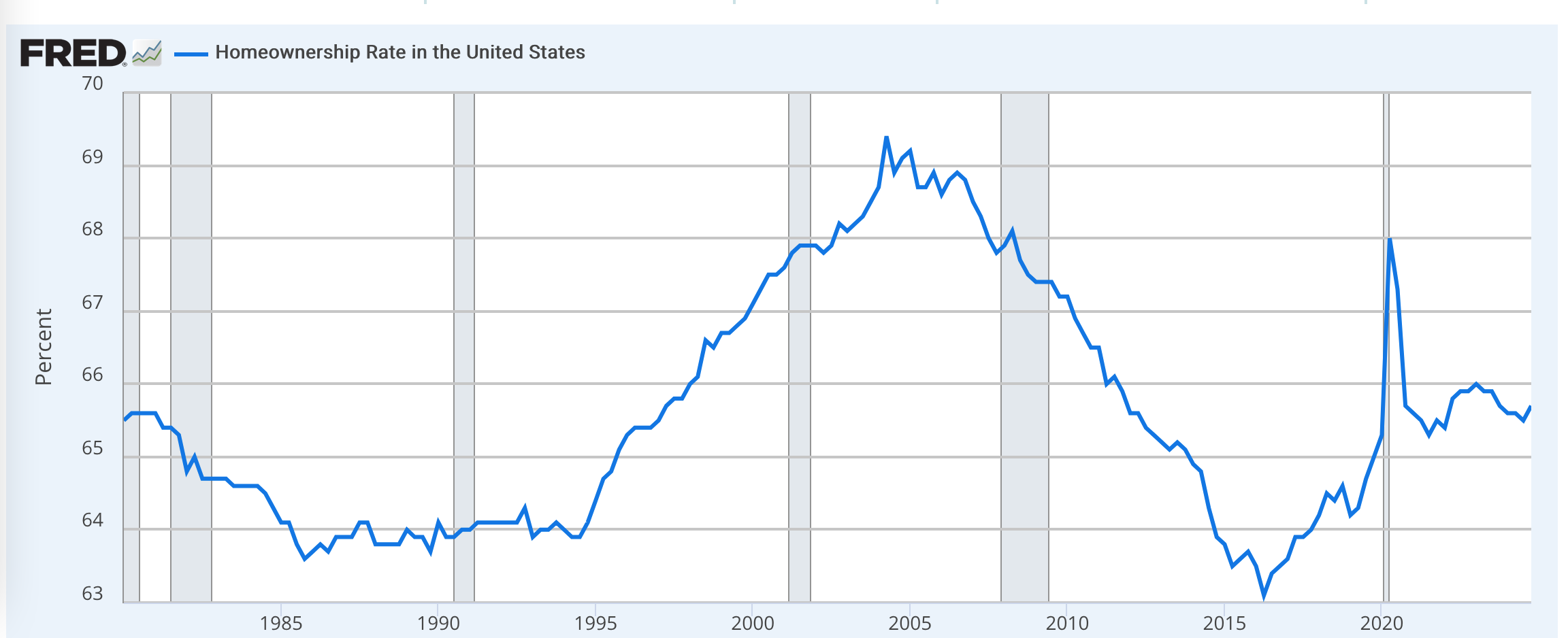

Readers can likely add to this walk down memory lane, but a final and very large example are the mortgage market subsidies via Fannie, Freddie, and the FHA. On paper, these are meant to boost homeownership since that leads to more conservative, as in establishment-favoring behavior. Note that it is not necessary to provide for stable residences (which also supports family formation) via supporting home buying. Germany (at least until neoliberalism started to eat into this system) gave tenants very strong property rights, so that many would live in the same rental apartment or home for decades. I have written repeatedly about the analogue in New York City’s rent stabilization system (which unlike rent control, allows landlords to increase rents in line with the allowed increases, which are set after much arm-wrestling to reflect increases in the owners’ costs.5). The key tenant protection was that the landlord had to offer a lease renewal to tenants that were current on their rent payments. The building I lived in in Manhattan had many tenants that had not only lived there for decades, but even made substantial improvements in their apartments, like putting in marble or granite flooring.

The aim of these German policies was to keep housing affordable. That in turn would support the competitiveness of German industry via wage payments not having to support housing rentierism.

But back to the key point of how the mortgage guarantors Freddie and Fannie served as Democratic party aligned influence machines. The case is set out long from in the Gretchen Morgenson and Josh Rosner book, Reckless Endangerment. They describe how the head of Fannie, Jim Johnson, used the massive mortgage guarantee fees to build what we would now see as NGO, with a big housing/mortgage research arm, and more important, the active creation of a pro-homeownership coalition, uniting many Democratic faction, particularly the Congressional Black Caucus. A piece by the respected writer/investigator Bethany McLean in Vanity Fair gives a sense of Johnson’s outsized influence and methods.

The pre-crisis homeownership rate was clearly a historical anomaly, particularly given that real wages have been stagnant for decades.6

Sadly I don’t have access to the Morgenson/Rosner book now, but they argued, credibly, that the Fannie/Freddie subsidize plus other successful initiatives by the Johnson-coordinated housing coalition played a meaningful role in the overly-permissive lending that led to the crisis. But lots of friends of the Democrats made out in the meantime.

So to come full circle: many are unhappy with the operation of the Federal government because they think a good bit of the money is going to bad or wasteful uses. But the employees, which are the focus of the DOGE slash and burn, are, as comparatively modestly paid workers, a small part of equation even when the actually are tasked to questionable initiatives. The big part of the grift are things these employees do not even remotely control, which is the approval of programs that are set out to enrich pet interests: Pentagon pork, tax breaks for activities the recipients would likely engage in anyhow, subsidized loans and activity guarantees, and now the big grift of payoffs not even credibly masquerading as a fund. But the Trump action is enough of a change in kind, as opposed to merely degree, as to sound large alarms about what might be next.

_____

1 Defenders point out that the Temporary Guarantee Program for Money Market Funds made money, since it collected fees and didn’t in the end have to make any payouts. But this ignores the three card monte of the rescue programs: of the massive and ultimately hugely distorting interest rate reductions to negative real interest rates, the Fed further subsidizing banks and mortgage/housing investors via QE (designed to lower longer-term Treasury and mortgage interest rates). A second factor was the $180 billion bailout of AIG. We will spare you mining our archives, but at the time, we (along with experts like Neil Barofsky, Special Counsel to the TARP) disputed Fed claims of the money they “made” from AIG.

2 WaMu depositors escaped this fate because JP Morgan bought the bank…and by all accounts got a monster bargain.

3 It would be an operational nightmare to fragment payroll across many banks to keep totals at risk below the FDIC ceiling.

4 Thiel was accused of triggering the run. Note it’s hard to evaluate this claim. Not that I am defending Thiel, but panic and rumors go through many channels. In other words, Thiel looks to have been intensified worries and thus transfers out of Silicon Valley Bank via his action, but it’s not clear similar behavior would have taken place mere hours or days later otherwise. From the Financial Times:

Peter Thiel said he had $50mn in Silicon Valley Bank when it went under, even after his venture fund warned portfolio companies that the tech-focused lender was at risk.

The veteran technology founder and investor was widely blamed for precipitating a bank run in which depositors tried to pull more than $40bn in 24 hours last week. His venture capital firm Founders Fund was among those that had advised clients to spread their deposits to other lenders as concerns about the bank mounted.

But Thiel told the Financial Times this week that he had maintained a substantial personal account at SVB even as fears mounted over its fate and later resulted in a run on the bank that ultimately toppled it.

“I had $50mn of my own money stuck in SVB,” said Thiel, who co-founded tech companies PayPal and Palantir in addition to Founders Fund.

5 In practice, the increases somewhat lagged inflation when inflation was high and exceeded the rate of inflation when inflation was low. The system was designed to preserve landlords’ profits on rentals.

6 I don’t have an explanation for the Covid spike and reversal. It looks like a data anomaly. Perhaps people buying homes in the exurbs/boonies for work from home, owning two homes for a bit that was mistakenly classified as two households owning a home, and that reversing as one of those residences was sold? Informed input would be appreciated.