By Flavio Calvino, Economist, Directorate for Science, Technology and Innovation Organisation for Economic Co-Operation and Development, and Luca Fontanelli, Post-Doctoral Researcher in Economics University Of Brescia. Originally published at VoxEU.

Artificial intelligence (AI) is rapidly transforming economies and societies. AI is already reshaping the demand for skills (Restrepo et al. 2018, Taska 2020), and AI-driven products and services have become an integral part of people’s daily routines, although they may not be fully aware of it (Tamura 2019).

AI is often considered a general-purpose technology (GPT) with the potential to bring significant improvements to adopters (Brynjolfsson et al. 2018). It could play a critical role in addressing societal challenges, such as health and climate change, by fostering breakthrough innovations (Agrawal et al. 2018). Although AI presents significant opportunities for boosting productivity and wellbeing, it also poses risks – for example, for financial markets, inequalities, and democratic values (Danielsson 2018, Pastorello et al. 2019, Acemoglu 2021).

Despite the centrality of AI in economic and policy debates (Gans et al. 2018, Bholat 2020), empirical research on its diffusion across firms is still limited, especially at the international level (see Acemoglu et al. 2022 for evidence on the US, and Calvino and Fontanelli 2023 for a more comprehensive literature review).

A Portrait of Firms Using AI Across Countries

Based on representative data from 11 countries, our recent analysis (Calvino and Fontanelli 2023) focuses on the characteristics of firms using AI, the role of complementary assets, and the links between AI use and productivity.

Our study is based on a distributed microdata approach that leverages a common statistical code developed by the OECD, executed in a decentralised manner on official firm-level surveys, thanks to the collaboration of experts across countries in the context of the AI diffuse project.

The common features of these data sources are their high degree of representativeness and the presence of information about the use by businesses of digital technologies – notably including AI – together with firm characteristics and outcomes – including employment and turnover, which allow building a proxy of labour productivity. The analysis focuses on 11 countries: Belgium, Denmark, France, Germany, Ireland, Israel, Italy, Japan, Korea, Portugal and Switzerland. Further information about the data, survey questions, and definitions is available in Calvino and Fontanelli (2023).

The cross-country analysis is carried out pioneering the use of a common statistical code, developed by the OECD, which is then run in a decentralised manner on the country-specific surveys by national experts. The country-specific outputs are then used for cross-country analysis, with consistency checks and metadata validation steps carried out in close cooperation with the experts from each country.

The analysis of the cross-country patterns of AI use by firms highlights five key findings.

Firm Size

AI use is more widespread among large firms. This may be relevantly related to their higher endowments or capabilities to use intangibles and other complementary assets required to leverage the potential of AI fully. This is presented visually in Figure 1, which highlights the positive relationship between shares of AI use and firm size class across countries.

Figure 1 Shares Of Ai Use by Firm Size Class: Cross-Country Findings

Notes: based on data for Belgium, Denmark, France, Germany, Israel, Italy, Japan, Korea, Portugal, and Switzerland. The y-axis shows the ranking for shares of AI users. Circles’ size is proportional to the number of countries for which the relation holds. See Calvino and Fontanelli (2023) for additional details.

Source: elaborations based on Calvino and Fontanelli (2023).

Firm age

Younger firms tend to have higher shares of AI use. Start-ups are more likely to introduce more radical innovations, especially in the advent of new technological paradigms.

Firm Sector

ICT and Professional Services have the highest sectoral shares of AI users. This indicates that AI use is not yet equally distributed across all sectors of the economy. Considering that AI is at a relatively early stage of diffusion, this suggests that its full potential as a GPT is yet to be fully realised.

Firms’ Complementary Assets

The use of AI is significantly linked to the presence of complementary assets, such as ICT skills and training, firm-level digital capabilities (proxied by the use of other digital technologies), and digital infrastructure. More general skills and innovative activities appear also positively associated with AI use.

Firm Productivity

On average, AI users tend to be more productive than non-users, with productivity premia being more pronounced among larger firms. But this does not seem to reflect the use of AI alone.

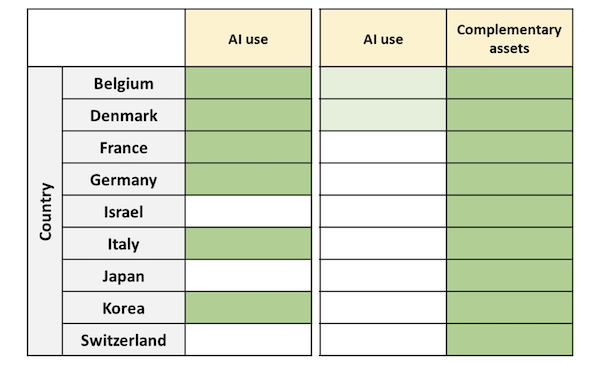

In fact, the above-mentioned complementary assets, especially those related to the digital transformation, play a critical role in the productivity advantages of AI users. When the regression analysis takes their role into account, as highlighted in Figure 2, the productivity premia of AI users significantly reduce or disappear, while complementary assets remain significantly linked with productivity.

Figure 2 Ai Use and Labour Productivity: The Role of Complementary Assets

Notes: based on the coefficients of regressions of (log) labour productivity (dependent variable) on AI use and additional controls. In the right panel the role of complementary assets is also taken into account. See Calvino and Fontanelli (2023) for additional details. Dark green: relation is positive and significant; light green: relation is positive and significant with lower magnitude with respect to the left panel.

Source: elaborations based on Calvino and Fontanelli (2023).

Our study is complementary to other recent OECD analyses on AI diffusion across firms based on microdata. These include work by Dernis et al. (2023), which focuses on companies and universities that have an AI-related online presence across four countries, and work by Calvino et al. (2022) that combines different sources of microdata (IPRs, online job postings, websites, and firm financials) to identify and characterise different types of AI adopters in the UK.

Policy Discussion

The evidence outlined above suggests that some firms – those that are larger, that have higher digital capabilities, and which are likely to be more productive already – are those currently exploiting AI more intensively. Initial evidence for one country (France) also seems to highlight that some more direct effects of AI on productivity may start emerging for firms that develop their own AI algorithms, likely endowed with higher digital capabilities and complementary assets.

Polarised adoption of AI, mainly by larger and more productive firms, combined with a role of AI in strengthening their advantages may imply that existing gaps between leaders and other firms could widen in the future, with relevant implications for social outcomes.

In this context, policymakers can play a crucial role in fostering an inclusive digital transformation, through a broad policy mix that affects incentives and capabilities and that captures synergies across policy areas.

This would include not only measures raising awareness about new technologies and developing firms’ absorptive capacity, but also providing relevant credit tools, fostering competition, improving knowledge production and sharing, and strengthening the foundation of digital infrastructure and skills.

Focusing on these complementary policy areas may enable AI use and its returns to be more widely spread across firms and sectors, fostering an inclusive digital transformation in the age of AI.

Authors’ note: The views expressed here are those of the authors and cannot be attributed to the OECD or its member countries. Please see Calvino and Fontanelli (2023) for additional details and notes.

References available at the original.