Yves here. The sorry and at least until the Fed relents, worsening state the US housing market, undermines the Biden Administration cheerleading over the state of the economy. Many people are subject to close to obligatory sales: death, divorce, disability (lower income making house unaffordable), and job-related relocation. This is not just an inconvenience but potentially damaging to anyone caught with a house they can’t sell or sell well. For instance, Mountain Brook, Alabama is somewhat market-condition insulated due to having a public school system rated in the top 1% of the US and pretty affordable home prices relative to incomes of the local afflueza. The house next door to ours, which was an updated house, unlike my mother’s, took 60 days and two price reductions to sell, the last to a discount of over 7% to the original asking price. Imagine how this translates now, both to less well-protected markets and the further increase in mortgage rates.

Do readers have sightings? Are there pockets in the US where houses are still selling without too much in the way of seller price concessions, say due to high buyer demand (like a major corporation moving operations there)? After all, real estate is always local….

By Wolf Richter, editor of Wolf Street. Originally published at Wolf Street

All that makes sense, but why are there still any cash-out refis when people could take cash out via HELOCs, without losing a 3% mortgage?

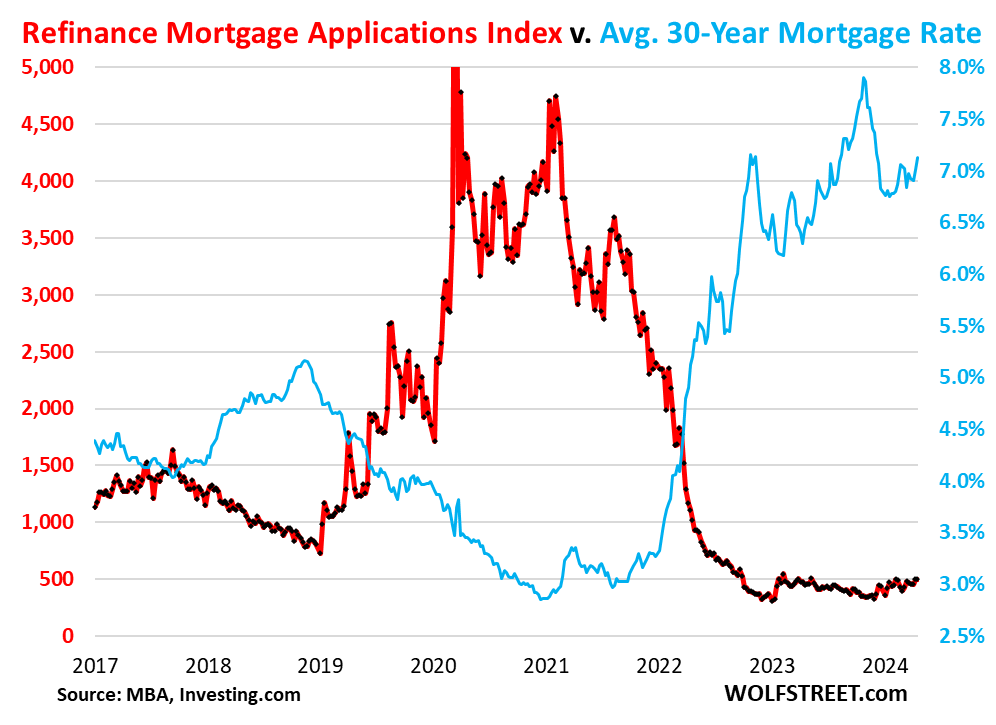

Mortgage rates continue to trudge higher from the abandoned Rate-Cut-Mania low. The average conforming 30-year fixed mortgage rate rose to 7.13% in the latest week, the highest since early December, according to the Mortgage Bankers Association today, as the 10-year Treasury yield has re-surged amid the Fed’s vigorous backpedaling on its December rate-cut visions after the presumed-vanquished inflation raised its ugly head again.

The MBA’s measure of the average 30-year fixed mortgage rate has risen 37 basis points from the Rate-Cut-Mania low of 6.76% in early January:

Still going higher. A daily measure, produced by Mortgage News Daily, which leads the fray by a few days, surpassed 7.13% a week ago and hit 7.50% yesterday, the highest rates since mid-November when Rate-Cut Mania was two weeks old. Today it’s at 7.43%. At the end of October, this measure kissed 8% for a day.

Housing market still frozen because prices are still too high

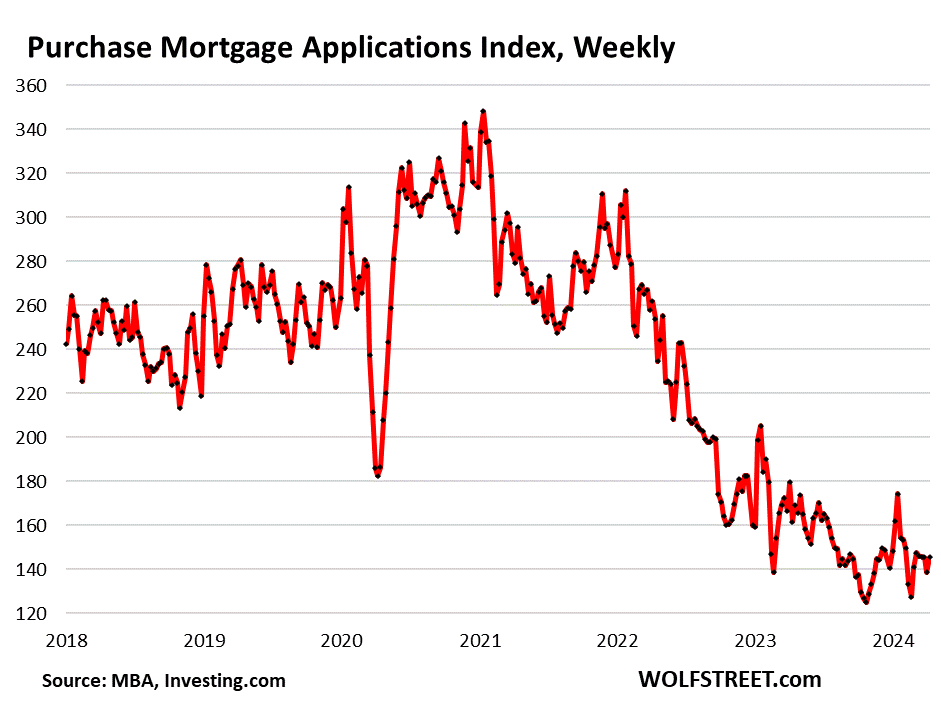

Mortgage applications to purchase a home have been wobbling near the record lows set in November and then again in February in the data going back to 1995. The cute mini-spike after the holidays during the waning days of Rate-Cut Mania only lasted a couple of weeks, though it created all kinds of hoopla, and didn’t really budge much from the record lows.

This is how far mortgage applications to purchase a home have plunged from the same week in the prior years – a sign that the housing market remains frozen because prices are still too high. While many potential sellers are still thinking that this too shall pass, many potential buyers have gone on strike:

- From 2023: -10%

- From 2022: -43%

- From 2021: -51%

- From 2019: -48%

The low level of mortgage applications to purchase a home tells us that sales of existing homes will continue to drag along the low levels that have been in effect for over a year:

Mortgage applications to refinance a home have been wobbling along historic lows for 18 months. They had seen a huge boom during the 2.5%-3.0% mortgage-rate era, and as mortgage rates began to rise in the fall of 2021, when the Fed began to pivot from raging inflation being just a “transitory” nothingburger to the fastest rate hikes in decades and the biggest QT ever. The mortgage market saw this coming and rates shot higher from these record low levels, and refis began to plunge.

In the latest reporting week, refis were down by 66% from the same week in 2019, and by 84% from the same week in 2021.

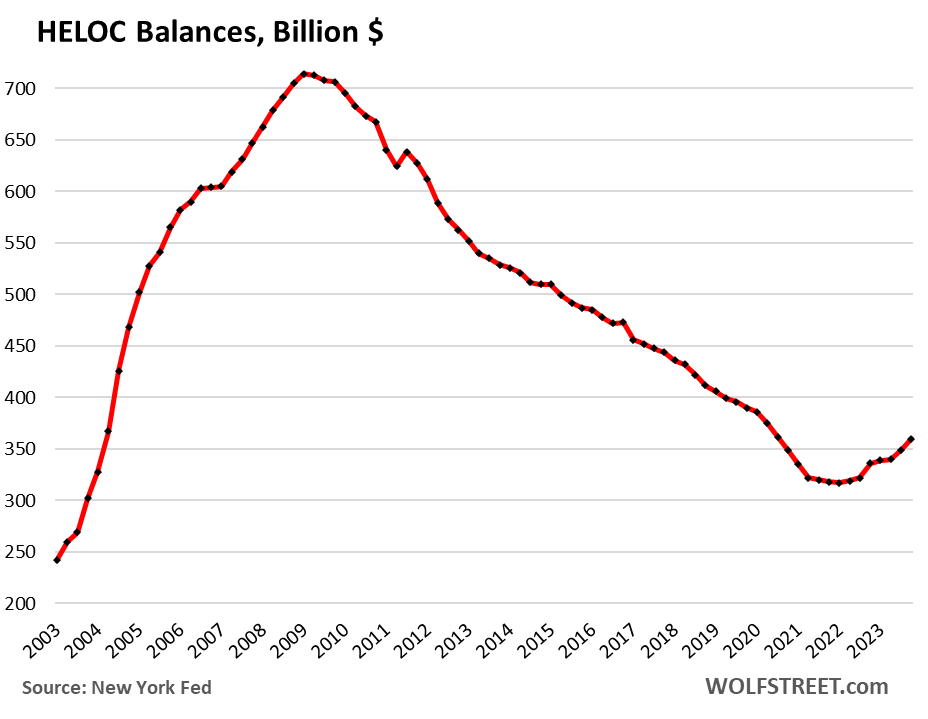

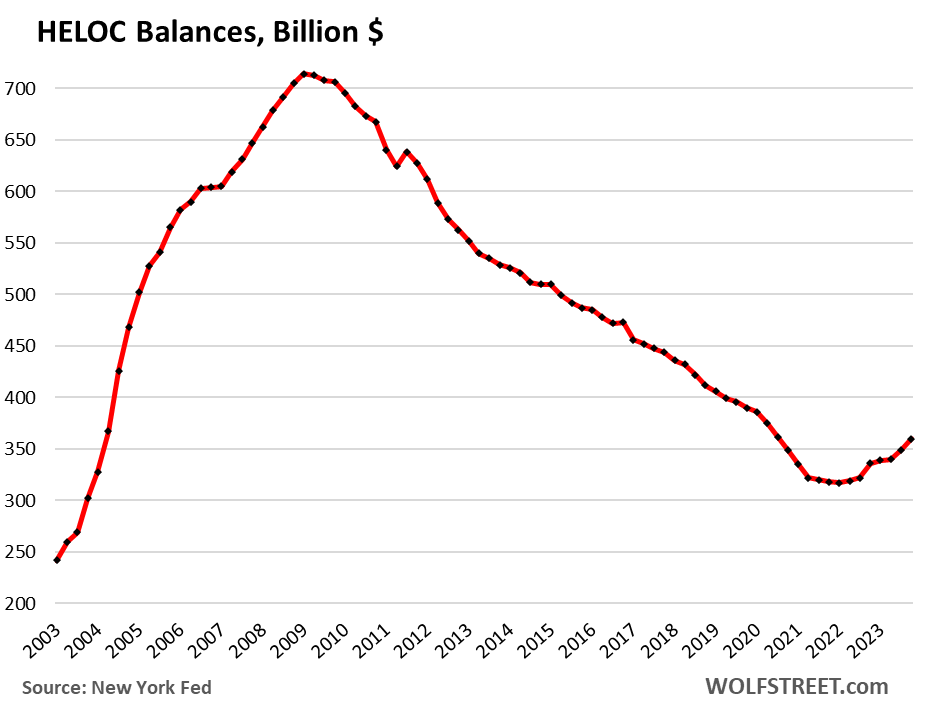

Why are there still any cash-out refis? Because people don’t know about HELOCs?

No-cash-out refis vanished almost entirely as mortgage rates have surged, as you’d expect.

But as you’d not expect, there are still cash-out-refis, though volume has plunged. This according to data from the AEI Housing Center.

Cash-out refis (brown stripes) have accounted for nearly all refis for over a year. Non-cash-out refis, in solid brown, have essentially ended (chart and data via AEI’s Housing Center):

Which is puzzling. It just doesn’t make sense. If people have enough equity in their home to get a cash-out refi, they could instead get a HELOC for the cash-out amount. If they need $100,000 to fund a big emergency, or want $100,000 to fund a bet-the-farm startup or a crypto Hail-Mary gamble, why not get a HELOC for $100,000 at 7% and keep the old 3% $500,000 mortgage? Would save a lot of money over getting a 7% $600,000 new mortgage.

HELOC balances have been rising, so some people are following this strategy. But why were there still any cash-out refis at all? They should be down to near zero, logically speaking, with HELOCs taking their place. Perhaps because people don’t know about HELOCs? Or because people can’t do math?

HELOC balances remain low, but after declining for 13 years from the peak in 2009, they turned around in 2022 when mortgage rates began to surge and as refis began to plunge. Since that low in Q1 2022, through Q4 2023, outstanding HELOC balances increased by $43 billion, according to New York Fed data.