by Charles Hugh-Smith

For everyone left out of the Fed’s hyper-financialized, hyper-globalized, hyper-inequality “new prosperity,” there’s always the bargain salmon cassarole.

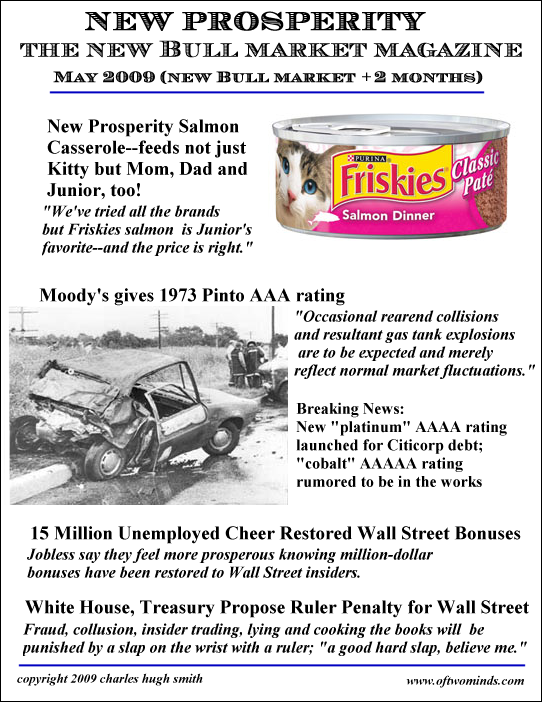

The latest issue of New Prosperity Magazine addresses the Fed’s “Goldilocks” inflation and the coming crack-up boom. New Prosperity Magazine’s maiden issue was published back in 2009, shortly after the Global Financial Meltdown had temporarily disrupted the trajectory of prosperity. (The May 2009 cover is below.)

Interestingly, the magazine updated a favorite cost-saving recipe for salmon casserole from the May 2009 issue. Financial meltdowns hurt everyone who owns any of the assets being repriced lower, of course, but they have a way of hurting those living paycheck to paycheck even harder via rampant inflation of essentials and / or mass layoffs.

The Federal Reserve has a “Goldilocks” problem with inflation: inflation was too cold for the Fed’s taste for the past decade, and now suddenly it’s too hot. The Fed won’t let anything like the financial well-being of the bottom 90% of American households get in te way of its implicit goal, which is protecting the wealth of the top 10% and especially the top 0.01%.

To do that, the Fed will have to recover all the ground lost to 2022’s spot of bother in stocks and bonds, and restore the trajectory of market gains toward ever-richer valuations. To accomplish that, the Fed will need a crack-up boom: a hybrid inflation which eviscerates labor’s modest gains in purchasing power while massively inflating asset valuations.

Higher interest rates are a headwind, to be sure, but a crack-up boom can still be managed if Corporate America can restore the Global-Sweatshop-to-landfill conveyor belt that’s boosted profits for decades.

The Fed will lend a hand by herding all the cash sloshing around into equities. The primary feature of the “new prosperity” that began in 2009 is the inequality of its distribution: those with the most wealth and access to low-cost credit corralled the majority of the gains, while those who already owned the assets that ballooned (housing and equities) did well simply by being older than the generations entering the workforce in the 21st century.

For everyone left out of the Fed’s hyper-financialized, hyper-globalized, hyper-inequality “new prosperity,” there’s always the bargain salmon casserole. Move over, Kitty-Cat, the whole family is sharing your supper.

Here’s the current issue:

And here’s the May 2009 issue:

Recent podcasts/videos:

The Big Problems And Crash Dynamics Of The Spring/Summer 2022 Housing Market Crisis, Simplified (1:08 hr)

My new book is now available at a 10% discount this month: When You Can’t Go On: Burnout, Reckoning and Renewal.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Trending:

Views: 5