Yves here. It’s surprising to see continued pain in the housing market, as contrasted with consumer spending continuing to be pretty good despite ongoing Fed “kill the labor market” efforts. Recall that Fed economists have long seen home prices as a much bigger driver of the wealth effect (“people who feel richer spend more”) than stock prices. You’d think that works in reverse. Perhaps there’s a lot of anchoring in how owners see the price of local houses, that even if they know intellectually that prices are down, they choose to believe on some level that the old prices, and even higher, are not far off.

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

Mortgage-rate buydowns, “smaller product footprints,” and “de-amenitizing” to bring down payments: D.R. Horton.

Homebuilders, in order to sell new houses at a decent clip in this new mortgage-rate environment – even as sales of previously owned homes have collapsed because sellers refuse to accept reality – are using a variety of strategies, outlined by D.R. Horton in its Q3 conference call, including:

- Mortgage-rate buydowns

- Smaller houses (“smaller product footprints”)

- “De-amenitizing” the houses (cheaper appliances, floors, countertops, simpler roof, no deck in the back?)

- And other incentives (free upgrades, etc.)

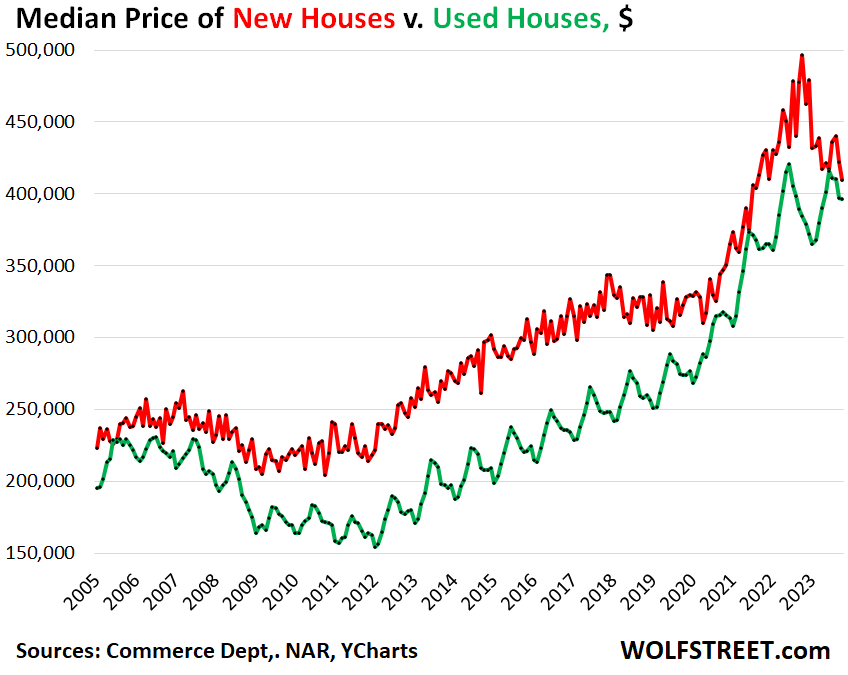

So the median price of new single-family houses sold in October fell by 3.1% from September, to $409,300 (red line), the lowest since August 2021, down by 17.6% from a year ago, which had been the peak, according to data from the Census Bureau today. The three-month moving average is down by nearly 12% from its peak in December last year (green).

These are contract prices and do not include the costs of mortgage-rate buydowns and other incentives such as free upgrades. But they do reflect the lower price points due to smaller footprints and the “de-amenitizing.”

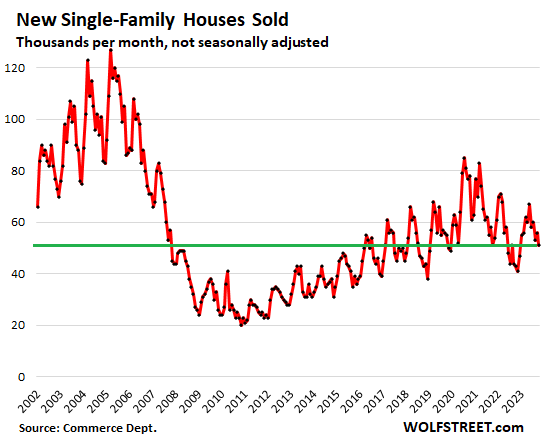

Sales of new houses – not seasonally adjusted, and not the annual rate of sales – fell to 51,000 houses in October, and while this was up by nearly 19% from a year ago, when the market was freezing up, it was still down by 7% from October 2019.

As you can see in the chart below, these sales levels would be nothing to write home about. But in the new mortgage-rate environment, and compared to the collapse in sales of previously owned homes (-27% compared to October 2019), they’re decent and document the effectiveness of bringing down payments via mortgage rate buydowns, “smaller product footprints,” and “de-amenitizing”:

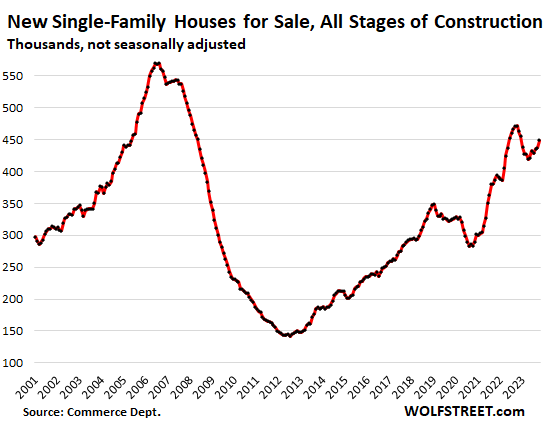

Inventory for sale of new houses at all stages of construction rose to 449,000 houses in October, which translated into 8.8 months supply at the current rate of sales – more than ample inventory and supply, and homebuilders are motivated to make deals to move this inventory:

Homebuilders have figured out this market, unlike current homeowners who are thinking about selling. Homebuilders have to build and sell homes no matter what mortgage rates are, while homeowners who’d want to sell are clinging to their hopes that “this too shall pass,” and they’re not putting their homes on the market, as the national median price, after peaking in June 2022, is on the way down.

Homebuilders are now aggressively competing with sellers of previously owned houses. And they also have to compete with the rental market, including newly-built-for-rent single-family houses by large landlords.

And monthly payments via bought-down mortgage rates make a difference and lower price points make a difference. The national median price of new houses has been falling faster than the national median price of existing houses (via the National Association of Realtors), and they’re now very close, which is unusual:

- Prices of new houses: -18% from peak (October 2022), $409,300

- Prices of existing houses: -6% from peak (June 2022), $396,100

What D.R. Horton said.

In their earnings call for Q3, D.R. Horton executives addressed questions about mortgage-rate buydowns and their other strategies to keep sales up in this mortgage-rate environment. Here are some of the key points (transcript via Seeking Alpha):

“To adjust to changing market conditions and higher mortgage rates, we have increased our use of incentives and are reducing the size of our homes where possible to provide better affordability for our homebuyers. We expect to continue utilizing a higher level of incentives in fiscal 2024, particularly rate buydowns in the current interest rate environment.”

“The average rate can move quite a bit through the quarter, but we tend to stay about 1 to 1.25 points below market at any given time.”

“About 60% of our total closings are used with some form of a rate buy-down … the most successful incentive we have seen.”

“Our buyers are focused primarily on affordability. And for us, the way we deliver that affordability is through the monthly payment process. And that’s obviously been a big driver for the rate buydowns, but also introducing smaller product footprints, and de-amenitizing some of the homes a bit and letting people do things to improve their homes after the closing when their financial position perhaps has changed and they can afford a little more.”

“Over half of our business [is] first-time homebuyers because despite what’s happening with interest rates, those buyers need a place to live. They don’t already own a home, so they’re not a discretionary buyer. They’re in the market looking at buy versus rent opportunities. So, if we can stay competitive with the rental market on that front, we’re going to continue to capture first-time homebuyer market share.”