A knowledgeable reader took a look at a court filing on the 2020 Santa Cruz Mountains Lightning Complex Fire. The implication for Los Angeles rebuilding its burned out neighborhoods are not pretty. As you will see below, nearly 2/3 of the homes destroyed in the Santa Cruz Mountains conflagration are not being rebuilt. Fewer than 15% have been rebuilt and are now occupied.

We will need to firm this tidbit as more authoritative sources weigh in, but this informed-looking comment on Reddit suggests that most claims will not be paid out in full due to the State of California being the insurer and lacking the capacity to do so. From Reddit:

The issue isn’t insurance companies going bankrupt in California since, as you mentioned, there are virtually no homeowners insurance plans with wildfire coverage that are underwritten by anything other than the California FAIR Plan anymore. The California FAIR Plan is both the underwriter for virtually all of California’s wildfire insurance as well as the guarantee association that is owned/run by the state.

The issue is that the price controls combined with the state pillaging the FAIR Plan’s funds for “other stuff” means that it only has $400 million to cover the losses. This is combined with the fact that California has a potentially >$60 billion budget deficit for 2025 that they don’t know how they’ll fund (the actual deficit isn’t actually known because the state is deliberately excluding certain items from its calculation of it, such as $20 billion that it needs to pay to the Federal Government this year. The deficit is not less than $38 billion with a middle estimate of ~$60 billion. The high estimate is “who knows?”).

The California Department of Insurance’s official plan on how to now “fund” the FAIR Plan’s multibillion dollar exposure is to prevent insurance companies from non-renewing existing plans as of January 9 and to threaten unspecified penalties for insurance companies that don’t retroactively renew policies that were non-renewed in the past few months. That wouldn’t necessarily do much even if it was able to be implemented, never mind that its unconstitutional and has a 0% chance of going through.

Because there’s very few policies written by insurance companies, their exposure is so low that there isn’t really a concern about any of them becoming insolvent. The real issue is that the FAIR Plan is very clearly insolvent, there is no viable mechanism to fund it, and the FAIR Plan itself is supposed to be the entity covering claims against insolvent insurers.

This isn’t a situation that has ever happened in the modern US and no one knows how it’s going to play out.

So everything is like CalPERS.

On top of the elephant-in-the-room “how meager will my insurance payout be?” another big impediment to reconstruction is shortages and inflation. If that’s in play from a major burn more than four years ago, imagine what will happen with the much greater pressure on building supplies with the unheard of scale of Los Angeles reconstruction when that gets going.

Other considerations complicate this picture. IM Doc sees evidence that many of the super-rich who lost homes in the Los Angeles fires won’t return. Recall that he lives in a high-end holiday enclave. Via e-mail:

I have now had 5 patients and friends as of today with their home in Ca a total loss. These are millions of dollars. 2 are uninsured completely.

My real estate agent patient had some news today. Every single available home in our area was sold this week. She now has over 200 squillionaires fighting over any and every home that is coming up on the market. All refugees from California. They know it will be years if ever that they have a home there again and they went out – to any desirable place in the country. The 18 million dollar high end homes are not involved so far. She told me that twice this week they have bid the home up over a million from asking – sight unseen.

The press is already starting to discuss hurdles homeowners whose houses were burnt out face, from insurance payouts being (legitimately) slow due to claims processing being overwhelmed to insurers trying to lowball payouts and policy-holders (and likely regulators and politicians) going to war with insurers, compounded by high odds of widespread underinsurance. High insurance costs would translate into conscious or accidental only-partial coverage.

Readers who are LA-knowledgeable mentioned other impediments to rebuilding. The wealthy Palisades is a family neighborhood. “There’s nothing to go back to: no schools, no grocery stores.” The implication is that families will be strongly inclined to move to functioning communities and may stay there due to not wanting to uproot their kids yet again.

By contrast, in Altadena, which is more middle class, many of the residents are multi-generational. They could not have afforded to buy the homes they lived in and cannot afford to rebuild. Nearly all will be underinsured, particularly in light of the way building costs will be sure to rise as a result of competition for materials and contractors.

Another potential stumbling point is pressure to rezone. For instance, there will be pressure to allow more multi-family housing, the arguments including climate change benefits (lower materials use, cheaper cooling and heating) and arguably faster restoration of housing for if nothing else, the benefit of businesses.

By A Recovering Californian

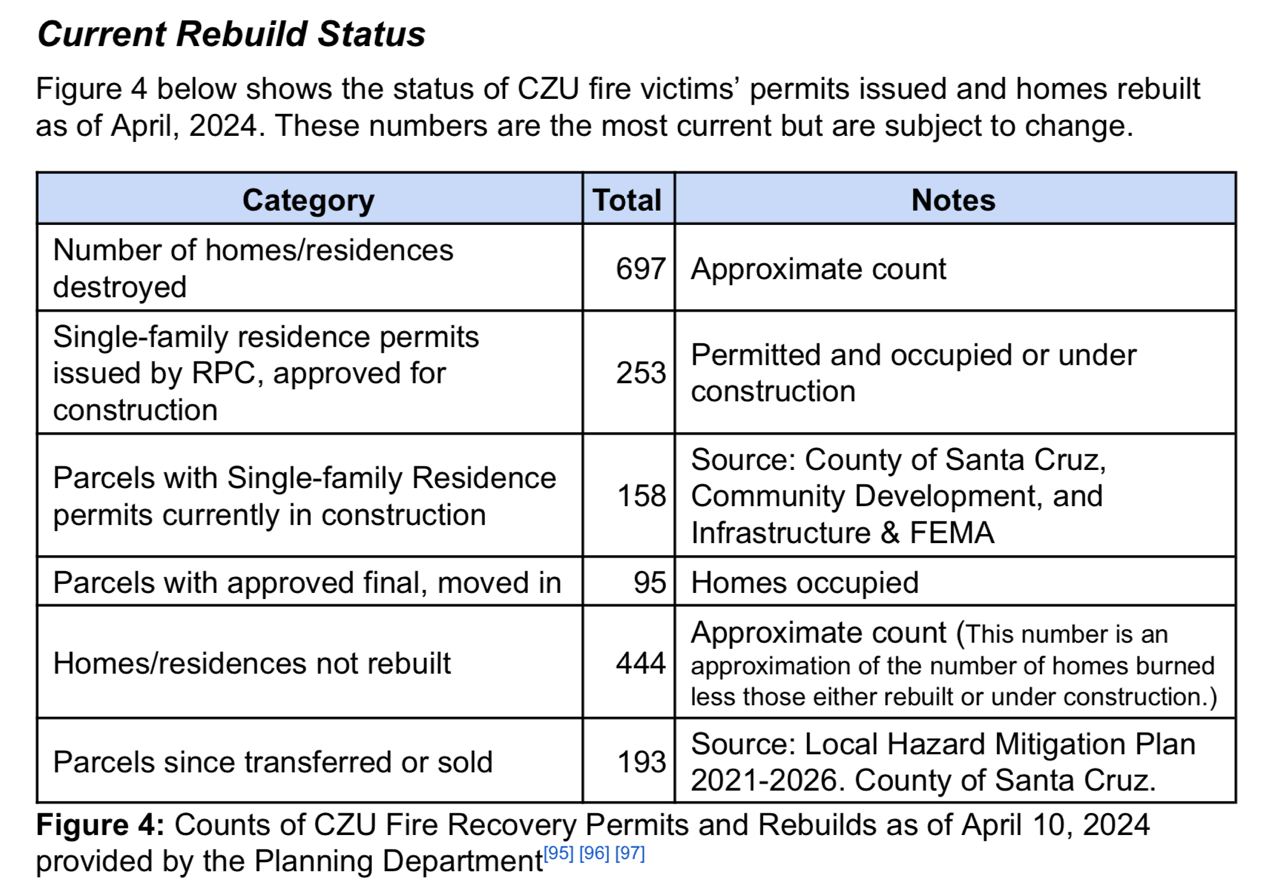

Out of approximately 700 homes destroyed in the 2020 Santa Cruz Mountains Lightning Complex Fire, only 95 have been rebuilt and occupied 4 years later, with only 158 more in construction. Nearly two-thirds are not being rebuilt.

A lot of the problem is that building materials are in short supply and subject to gouging and inflation. Of course, most lumber for U.S. construction is harvested these days in Canada, so tariffs may also come into play. Most of the hardware we used to build our new house came from Mexico or China, so add those tariffs as well.

LA is somewhat different, but expect re-zoning fights over density in the predominantly single-family dwelling areas of Pacific Palisades and Altadena. The few who do rebuild will see 5-fold increases in insurance premiums, which is what is being seen in the Santa Cruz Mountains. The hit to the state FAIR insurer of last resort program from the L.A. fires is already estimated at $26 billion.

As I mentioned, my mantra remains population growth and density. When I started high school in 1971 the population of California was 19.9M and remained stable throughout the decade. Today the population of LA County alone is over 20M. Density is up, intrusion into wildland is up, and camping by those living rough has been a factor in many recent fires (we don’t know the cause of the current fires). Of course, everything in LA is quick-and-cheap stick-built construction that everyone knows is going up in flames in a hot minute when embers start blowing in 60-100 mph Santa Ana winds.

Note also that the open lands of the Santa Monica Mountains are not managed by the state of California but Federal government. Seems like this was under Trump leadership 2017-2021. Of course, Congress needed to cut funding so that Genocide Joe could arm Ukraine and Israel.

Management of the rest of this area is under a web of local agencies funded by local property taxes, which are still ridiculously low compared with the rest of the country since Prop 13 in 1978. The San Gabriel Mountains above Altadena are U.S. Forest Service lands — Angeles National Forest and San Gabriel National Monument. All the Newsom-bashing is wrong on this point.

It was mainly the Federal Bureau of Reclamation that allowed LA real estate hustlers to steal millions of acre-feet of water from the Owens Valley in the eastern Sierra Nevada and from the Colorado River. That infrastructure is aging; the big reservoir in the Palisades was offline for repairs (not negligently — this is supposed to be the rainy season).

Here’s the punchline from the June 2024 Santa Cruz County Grand Jury report on rebuilding after the 2020 fire: