by confoundedinterest17

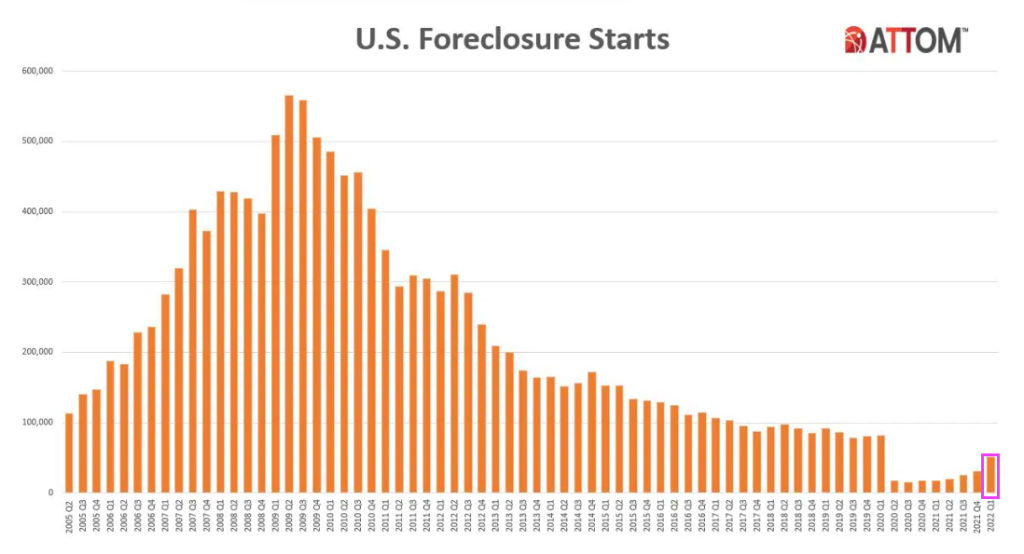

I remember this headline from CNBC from THU, OCT 14 2021: Foreclosures are surging now that Covid mortgage bailouts are ending, but they’re still at low levels.

But the foreclosure surge never materialized.

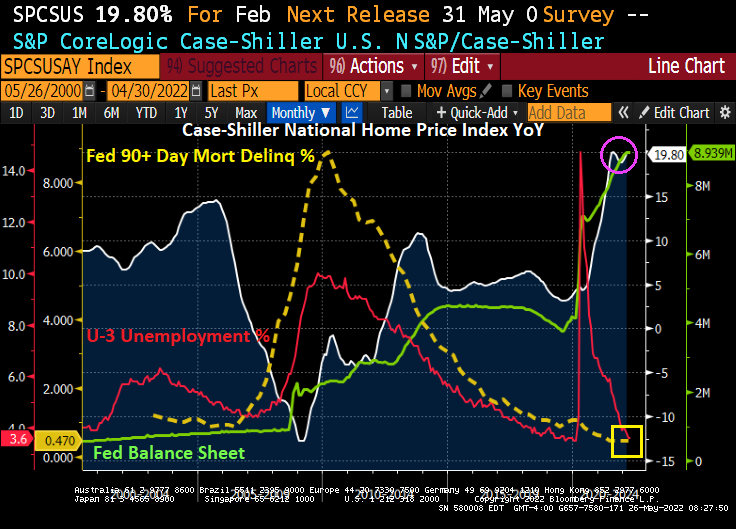

If we look at 90+ days late for mortgages (yellow line), we see that the surge in unemployment with the Covid outbreak and subsequent government shutdowns (red line) did not lead to a surge in mortgage foreclosures.

This situation is quite unlike 2008 when collapsing home prices and the subsequent surge in the unemployment rate led to a 90+ days late surge on mortgages (yellow line).

Difference between today and 2008? The Federal Reserve’s asset purchase (green line) surge happened twice AFTER the 2008 housing crash. Once in late 2008 through 2014, then a second, bigger surge in March 2020 after the Covid outbreak. One big difference is the surge in home prices, home price growth was 3.69% YoY in December 2019 and skyrocketed to 19.80% as of February 2022. This translates to a massive increase in homeowner equity, leading to a lower probability of default.

So, there you go. Powell and The Federal Reserve made housing unaffordable for millions of Americans, but The Fed did help thwart another mortgage default crisis. BUT we will see what happens with future rate hikes from The Fed.

Here is Attom’s US Foreclosure Starts chart. Yes, that is hardly a surge, although foreclosure starts did rise in Q1 2022.

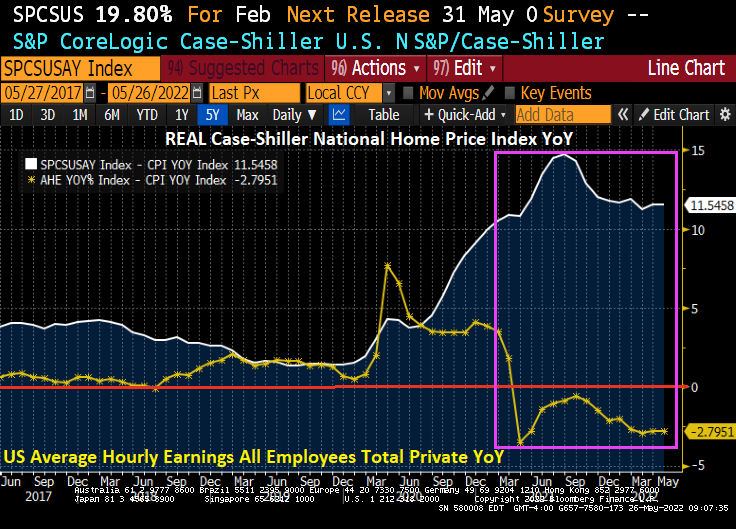

So, The Fed has helped make housing simply unaffordable. Look at the growth of REAL home prices relative to REAL average hourly earnings.

The kids at The Fed aren’t too sharp when it comes to making housing affordable.

Views: 5