Yves here. It is useful and welcome to see data, as opposed to conjecture and assertion, around the position of the dollar. We’ve argued that the logical reserve currency successor by virtue of the size of the underlying economy, China’s renminbi, is not likely to assume the role soon if ever. For starters, China is unwilling to assume the burden of running regular trade deficits and eschewing capital controls. The Euro ceased being a candidate after the 2008 crisis exposed its limitations and Eurozone governments weren’t willing even to consider possible reforms. But some smaller currencies are gaining ground.

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

The US dollar has been the dominant global reserve currency for decades, amid many global reserve currencies. And there are lots of people, institutions, and governments that want to see an end to this “dollar hegemony.”

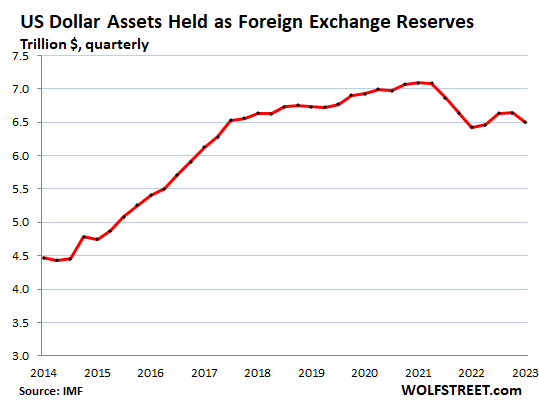

But central banks other than the Federal Reserve are still holding large amounts of US-dollar denominated assets – $6.5 trillion in total – such as US Treasury securities, US government-backed MBS, US corporate bonds, US agency securities, even US stocks (the Swiss National Bank), all of which combined make up the USD-denominated foreign exchange reserves that central banks other than the Federal Reserve hold.

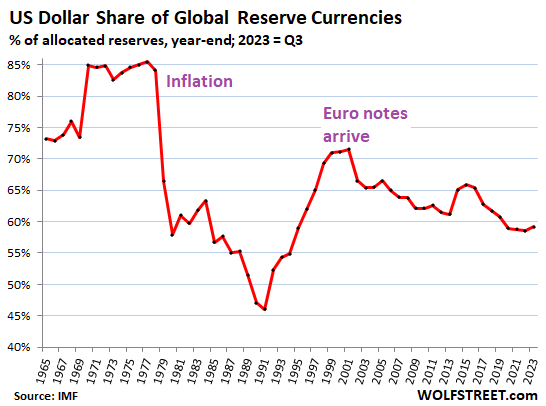

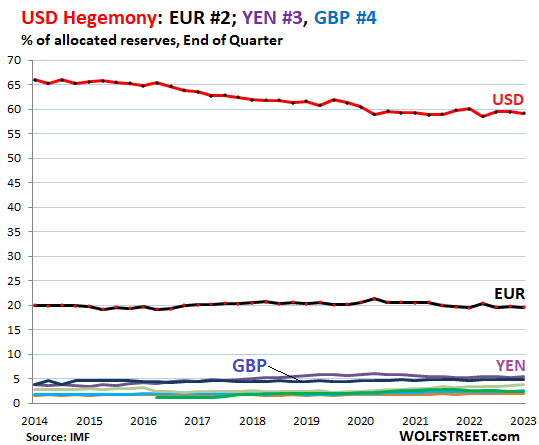

The share of USD-denominated foreign exchange reserves dipped to 59.2%, according to the IMF’s COFER data released on December 31 for Q3 2023. For the past 20 years, the USD’s share has been on a slow downward trend, with other currencies nibbling at it from all sides. The euro was #2, the yen #3, the British pound #4. The Chinese renminbi dropped to #6, behind the Canadian dollar (more on all those in a moment):

In dollar terms, the holdings of USD-denominated assets at foreign central banks dipped to $6.5 trillion. Note that the Fed’s holdings of Treasury securities and MBS are not included in foreign exchange reserves. No central bank’s holdings in its own currency are included.

Since 1965, the USD’s share of global reserve currencies has gone through a tumultuous history, including the collapse of its share starting in 1978 through 1991 from 85% to 46%. This came after inflation exploded in the US in the late 1970s, and the world lost confidence in the Fed’s ability to manage inflation. And the decline of the USD’s share continued even as inflation began to fade in the 1980s.

But by the 1990s, confidence returned gradually and the dollar’s share rebounded until the euro came along and put a stop to the gains by the USD (2023 through Q3)

The Other Major Reserve Currencies

The euro’s share (#2) has been roughly stable at around 20% for years. In Q3, it dipped to 19.6% (black line, red dots in the chart below). The other currencies are the colorful tangle at the bottom of the chart:

The USD Is Losing Ground Against the Tiny “Other Currencies” Combined

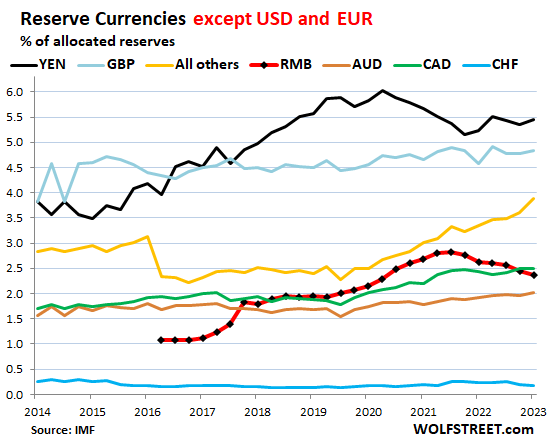

The chart below shows the colorful tangle magnified. China is the second largest economy in the world, yet its currency plays only a minuscule and declining role as a reserve currency, and is no threat to the US.

But note the surge of the yellow line, “all other currencies” combined, each of which has a smaller share than even the swiss franc, but combined, they’re making headway.

- #3, Japanese yen, 5.5% (purple).

- #4, British pound, 4.8% (blue).

- #5, Canadian dollar, 2.5% (green), bypassing the Chinese renminbi.

- #6, Chinese renminbi, 2.4%, sixth quarter in a row of declines, lowest since Q4 2020 (red), amid the reality of capital controls, convertibility issues, and other issues. Central banks appear to be leery of holding RMB-denominated assets.

- #7, Australian dollar, 2.0% (brown).

- #8, Swiss franc, 0.18% (blue).

- “All other currencies” combined (yellow) have a total share of 3.9%. The largest one of them has a share even smaller than the Swiss franc’s share of 0.18%. But their combined share has risen from 2.5% in 2019 to 3.9% currently. These tiny reserve currencies combined are taking share from the USD:

Dollar-Exchange Rates and Foreign Exchange Reserves.

The USD exchange rate matters. Foreign exchange reserves are measured in USD. For reporting and comparison purposes, the holdings in EUR, YEN, GBP, CAD, RMB, etc. are translated into USD figures at the exchange rate at the time. So the exchange rates between the USD and other reserve currencies change the magnitude of the non-USD assets – but not of the USD-assets.

For example, Japan’s holdings of USD-denominated assets are expressed in USD. But its holdings of EUR-denominated assets are translated into USD at the EUR-to-USD exchange rate at the time. So the magnitude of Japan’s holdings of EUR-assets, expressed in USD, fluctuates with the EUR-to-USD exchange rate, even if Japan’s holdings don’t change.

The exchange rates between the USD and other currencies can fluctuate wildly. The yen dropped a lot in 2022 and then again in 2023 against the USD. So the value of yen-denominated assets held by central banks (other than the Bank of Japan) would have declined when expressed in USD, and it would have pushed down the share of the yen-denominated foreign exchange reserves expressed in USD.

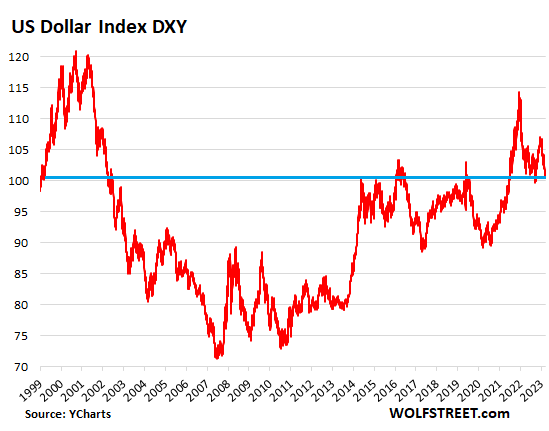

But over the long run, the currency pairs are amazingly stable, despite massive fluctuations in between. The Dollar Index [DXY], which is dominated by the euro and yen, is back at 101, where it had been in 1999 (data via YCharts):