What Federal Reserve chairman Jay Powell says on Friday in his speech at the Jackson Hole symposium should swiftly ripple across the markets. From interest rate sensitive short-duration fixed income assets through to stocks, the dollar and thus commodities.

As Nicholas Colas, Co-founder of DataTrek Research, says, these markets all talk to each other. Indeed, it was the bond market’s soothing communication — in the shape of falling yields — that gave equity investors the confidence to deliver the sharp summer rally.

The problem for stock market bulls is that some of the bond chatter may soon prove less supportive as it passes on a worrying message from the energy sector.

Oil prices and Treasury yields have been whispering to each other since the 1970’s says Colas, as energy costs influence general price inflation, which of course impacts bond yields.

“These two markets are still in close touch: WTI crude prices retested their Russian invasion of Ukraine highs on June 8th and 10-year Treasury yields saw their year-to-date peak on June 14th. Lower oil prices since have helped keep something of a lid on 10-year yields,” says Colas.

He adds that the bullish or bearish case for any asset class or security needs support from other markets. “It is hard to be a high conviction bull on U.S. stocks, for example, without also believing that 1) oil prices will decline, 2) high yield spreads will tighten, and 10-year yields will remain capped around 3%”.

And there’s the rub. Benchmark Treasury yields have moved back above 3% and observers of a technical mindset are pointing out that the head and shoulders pattern that may have suggested further downside for yields has morphed into something more dangerous for bond prices.

Source: Bank of America

Now, Paul Ciana, technical strategist at Bank of America, is asking “should the 4% yield debate be resurrected”.

“If the aforementioned daily chart moves to invalidate the head and shoulders top in favor of a wedge continuation pattern with a break above 3.1% then yes we should start resurrecting some higher yield scenarios because they may be entering a rare ‘launch’ phase,” Ciana wrote this week in a note.

Powell could provide the fuel for this launch. But so could oil. Supply concerns continue to underpin the oil price. Goldman Sachs earlier this month forecast a Brent price around $120 a barrel in the fourth quarter.

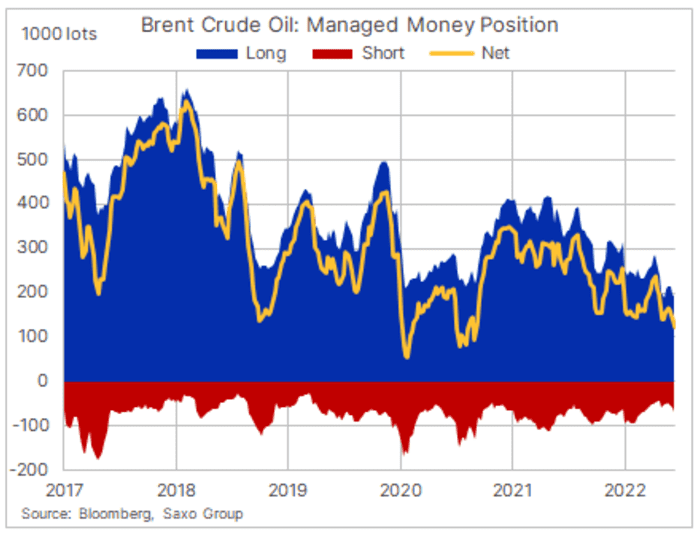

And Ole Hansen head of commodity strategy at Saxo Bank notes that speculative positioning leaves that market vulnerable to a pop higher.

Source: Saxo Bank

“With oil fundamentals still very supportive, the market seems to be realizing the energy market is not the best hedge against an economic slowdown, and it has raised the risk of a response from speculators who recently cut bullish oil bets to an April 2020 low,” says Hansen.

“A recovery at this point may force money managers to reassess their exposure in Brent and WTI with a potential short-squeeze brewing.”

From oil, to bonds, to stocks, the whispering never stops.

Markets

S&P 500 futures ES00, -1.59% were down 0.3% to 4,189 and Nasdaq 100 futures NQ00, -2.02% dipped 0.4% to 13,103. The dollar index DXY, -0.13% eased back 0.2% to 108.31 and 10-year Treasury yields TMUBMUSD10Y, 3.035% rose 3.3 basis points to 3.063%. Gold GC00, -1.06% fell 0.7% to $1,759 an ounce and Bitcoin BTCUSD, -3.40% was down 0.8% to $21,482.

The buzz

Federal Reserve Chair Jay Powell will speak on the economic outlook on the second day of the Jackson Hole symposium at 10 a.m. Eastern.

Quite a big batch of U.S. economic data on Friday. The July core PCE price index, an important inflation gauge, was up 4.6% year-on-year, down from 4.8% in June and 0.1% lower than economists’ forecasts.

Personal consumption rose 0.1% in July on a seasonally adjusted basis, but this was well below June’s 1.1% gain and also less than the 0.4% rise expected.

The University of Michigan consumer sentiment survey comes out at 10 am Eastern.

Shares in Dell Technologies DELL, -9.81% are down 5% in pre-market trading after the computer maker revealed results and called the end of the pandemic-era IT sales boom.

Twenty million U.S. homes are struggling to pay their utility bills says National Energy Assistance Directors Association.

And on that note, the U.K energy regulator raised the cap that British households can be charged for gas and electricity to £3,549 ($4,200) a year. Last summer, the price cap for the typical customer stood at £1,138 and the increase reflects the surge in energy prices as countries chase reduced supply in Europe.

Best of the web

Data centers prepare for blackouts

Inflation is not hurting corporate profit margins

Mouse embryos can now be created synthetically

Student loan forgiveness raises inflation, budget risks

The chart

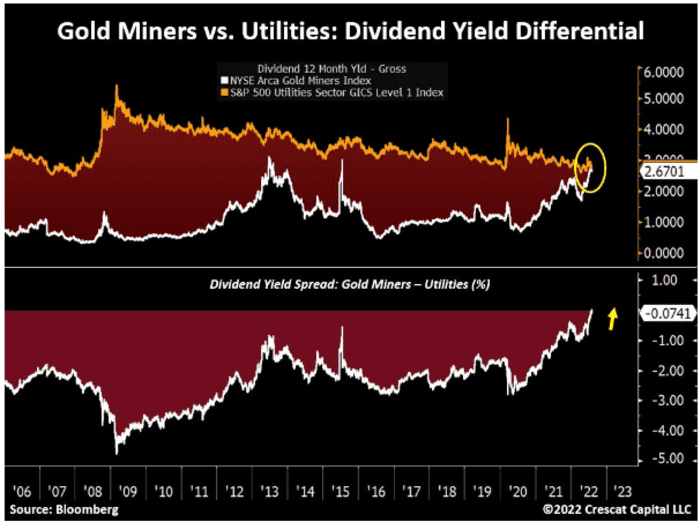

Hedge fund Crescat Capital reckons higher inflation is going to prove a lot stickier than many think. And it thus favors assets that offer protection for this scenario, such as natural resources producers like oil and gas groups, and metal miners.

Particularly gold miners in the exploration phase. These may be snapped up by bigger producers, which have tended to underinvest of late, says Kevin Smith, Crescat’s chief investment officer. That lack of spending has helped support dividend payments among medium and big cap gold miners. Now, as the chart shows, for the first time ever the cohort yields nearly as much as the utility sector.

Source: Crescat Capital

Top tickers

Here were the most active stock-market tickers on MarketWatch as of 6 a.m. Eastern.

| Ticker | Security name |

| TSLA, -1.86% | Tesla |

| BBBY, +2.39% | Bed Bath & Beyond |

| GME, -3.88% | GameStop |

| AMC, -5.85% | AMC Entertainment |

| APE, -7.10% | AMC Entertainment APE |

| NIO, -0.80% | Nio |

| AAPL, -1.79% | Apple |

| NVDA, -5.29% | Nvidia |

| AMZN, -2.72% | Amazon.com |

| BABA, +0.03% | Alibaba |

Random reads

Bach not worse than the bite: classical music calms down pooches.

Their eyes are not allowed to meet across a crowded room, in this nightclub.

This zookeeper dressed up as an ostrich — here’s why.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.