Yves here. This article on the effort to move to cleaner energy sources suffers from being written by economists. It sees falling costs of these new power technologies as having the promise of faster uptake. But it also presents offsetting forces, such as “‘distributional effects” (key interests not wanting their rice bowls broken; also lower income households being unable to afford green tech absent big subsidies, which are being cut due to competing demands like more war). Another bugboo is “populism” as in supposedly ideologically-motivated opposition to climate-friendly policies.

That is not to say that there is not substantial “because freedumb” opposition to efforts to reduce greenhouse gases, since they entail a lot of government intervention: subsidies, taxes, prohibitions, regulation. But here and in many cases, resistance to uptake of these newer energy sources is not due simply to libertarian cussedness but often to bona fide issues that transition touts are loath to acknowledge.

Back in the stone ages of my youth, I had a gig where I got to evaluate pretty much all the oddball tech deals that came in over the transom to a well-heeled VC fund. They had bona fide experts on normal tech like computers, software, communications. I got all the “none of the above” deals, like a new way to make synthetic diamonds, thin film solar panels, advanced batteries, a new cooking technology, and even what are now called QR codes (this over a decade before smart phones). They figured someone was going to have to figure them out de novo and I would be as good as anyone else they had to assign to do that.

I quickly worked out that most investors got derailed by letting the inventors pull them into focusing on whether the new technology performed as advertised. That was necessary but far from sufficient to see if an investment made sense.

The critical questions, which I soon inferred many monebags overlooked, were:

1. What were the competing products and technologies, and how did this offering stack up? The inventors almost without exception defined competition too narrowly, as around their technology, and not in terms of what customers or consumers would see as potential substitutes.

2. How much will consumers/customers need to change behavior to employ this new technology?

3. How long will it take to achieve production efficiencies?

Let’s start with electric vehicles. Sales in the US have stalled. One common belief, with a lot of merit, is prices are still too high for many potential buyers. But there is a tendency to wave off #2 type issues, above all, charging. There aren’t enough EV charging stations relative to what will be, and arguably now is needed, so home charging remains very important. The cost of having an EV run out of charge is higher than having a gas car go empty, since an EV has to be towed. So there’s greater downside and cost. Most importantly, despite the press tending to focus on consumers not yet eating enough of the EV dogfood, there’s a failure to deal with the faltering state of the US grid, the reported failure of utilities to invest to increase capacity, and the resulting potential for brownouts and rolling blackouts. I am sure readers can add other EV questions, like heavier cars leading to shorter tire life, and replacing tires is not just a hard cost but also a time cast.

So this article implicitly ignores some of the neglected real world issues with a big technology/infrastructure changeover as bona fide reasons for foot-dragging.

By Pierre-Olivier Gourinchas, Research Director and Economic Counsellor International Monetary Fund; Director, Clausen Center for International Business and Policy; S.K. and Angela Chan Professor of Global Management in the Department of Economics and Haas School of Business University Of California, Berkeley; Gregor Schwerhoff, Economist International Monetary Fund; and Antonio Spilimbergo, Deputy Director, IMF Research Department International Monetary Fund. .Originally published at VoxEU

The ambition of the Paris Agreement is to limit global warming to “well below 2°C”. This column argues that while some progress towards this aim has been made, substantially more policy action is required. Since 2015, new challenges have emerged for climate policy, including rising populism, shrinking fiscal space, a surge in inflation, higher interest rates, and concerns for energy security. At the same time, technology has progressed faster than expected, bringing a substantial cost reduction for green energy. The success of green policies in containing greenhouse gases depends on the race between political backlash and technological progress.

Recent developments in climate policy paint a gloomy picture: the UK government is backtracking on previous climate commitments; the US is delaying and watering down planned pollution regulation; and China and India continue to build coal power plants. 1 As a result, current efforts are far from sufficient to honour the 2015 Paris Agreement, which requires limiting global warming to “well below 2°C” (Black et al. 2023).

Since then, new political challenges have been added to existing ones (Gourinchas et al. 2024). Among the existing domestic challenges are the distributional effects of climate policy. Even a well-designed climate policy, with minimal impact on aggregate activity (Metcalf and Stock 2023), could lead to significant sectoral reallocation. This causes political resistance from sectors expecting to shrink. The voluntary nature of the Paris Agreement is another existing challenge. It causes concerns about losing competitiveness through climate policy if other countries do not comply.

Among the new challenges are the economic effects of the COVID-19 pandemic and its aftermath. Government programmes to support households and sectors affected by the pandemic have resulted in much-reduced fiscal space to finance the green transition. At the same time, the surge in inflation forced central banks to raise interest rates. Higher rates curtail financing for clean technology investments more than for conventional technology, because clean technology typically has a more front-loaded investment profile (Hirth and Steckel 2016).

Additional new challenges arise from the effect of Russia’s invasion of Ukraine on energy supply. With the abrupt decrease in energy trade from Russia to Europe, concerns about energy security soared and remained high for over a year (Figure 1.) The scramble to secure energy supply resulted in increased investments in fossil fuel infrastructure, especially oil and natural gas (IEA 2023). At the same time, Russia re-directed its supply of oil and natural gas away from Europe to China and India at a discount, which increased the consumption of these fuels in these two countries.

Figure 1 Weekly number of US and European newspaper articles referencing “energy security” and “green transition”, 9 October 2021 to 9 October 2023 (9 October 2021 = 100)

Sources: ProQuest, IMF staff calculations.

Note: The green transition line comprises both “green transition” and “energy transition.”

A third group of challenges arises from rising populism. Populist movements have tended to challenge climate policies following the narrative that climate policy is a project of the ‘elites’, who stand against the will of ‘the people’, similarly to what happened to health policies during COVID-19 (Fiorino 2022, Spilimbergo 2021). Being so visible, carbon pricing – the most efficient economic tool for emission reductions – has become a primary target and source for discontent. For instance, the ‘yellow vest’ protests in France stopped an increase in gasoline taxes in 2018, and the recent protests in Europe in the agriculture and transportation sectors are focused on the Green Deal. As a result of rising populist pressures, governments have leaned against previous climate policy instead of advancing it. In the US, the Inflation Reduction Act (IRA) achieved support in the US Congress partly through potentially protectionist measures, such as local content requirements that might contravene WTO rules. This reduces the opportunities for trade partners to benefit from the US green investment push. The IRA also generates an estimated $391 billion in expenses (CRFB 2022), while carbon pricing would have generated a revenue.

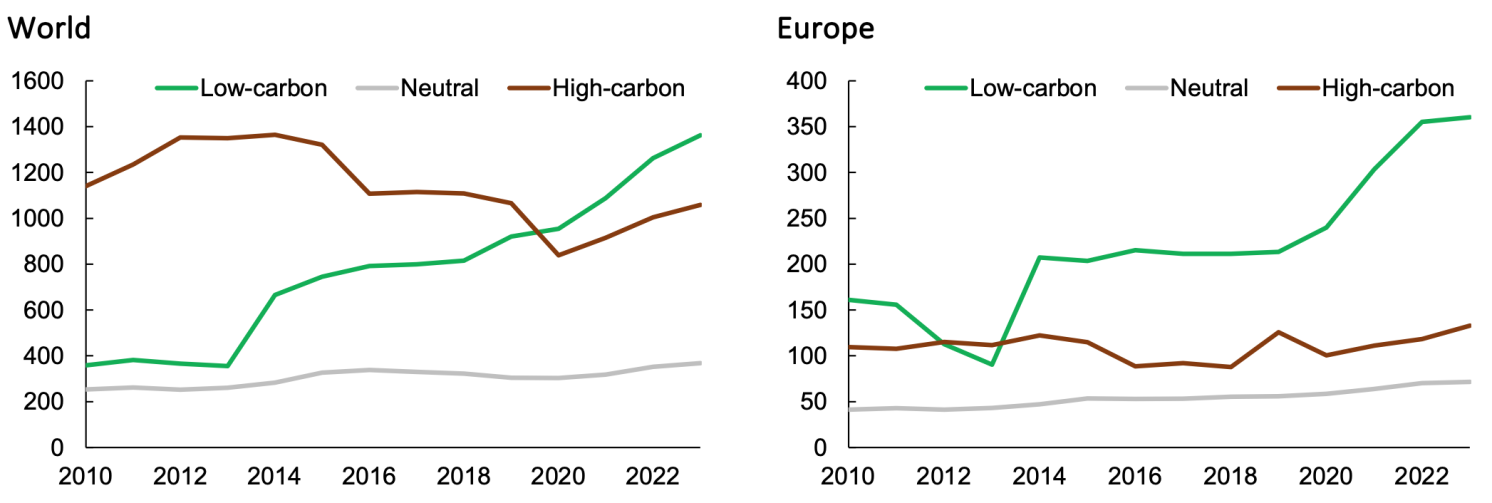

At the same time, climate policy was supported by significantly faster than expected technological achievements. This translated into rapid declines in the prices of low-carbon energy. As a result, the share of investments allocated to low-carbon energy technology has surpassed the share going to high-carbon energy technology (Figure 2). This process is self-reinforcing through two mechanisms. The first is learning by doing. This is most striking for solar panels: it is estimated that each doubling in cumulative production capacity in solar photovoltaics reduces prices by 22.5% (Creutzig et al. 2017). The speed of these developments has surprised even experts. Until recently, World Energy Outlook reports from the International Energy Agency projected solar energy production well below the level of what eventually materialised.

Figure 2 Global energy investment, 2010–23 (billions of 2021 USD)

Sources: IEA (2023b), IMF staff calculations.

Note: Low-carbon = renewables, nuclear, fossil fuels with carbon capture and storage, and energy efficiency; Neutral = electricity networks and storage; High-carbon = fossil fuel generation and fuel production; 2023 numbers are IEA estimates from May 2023.

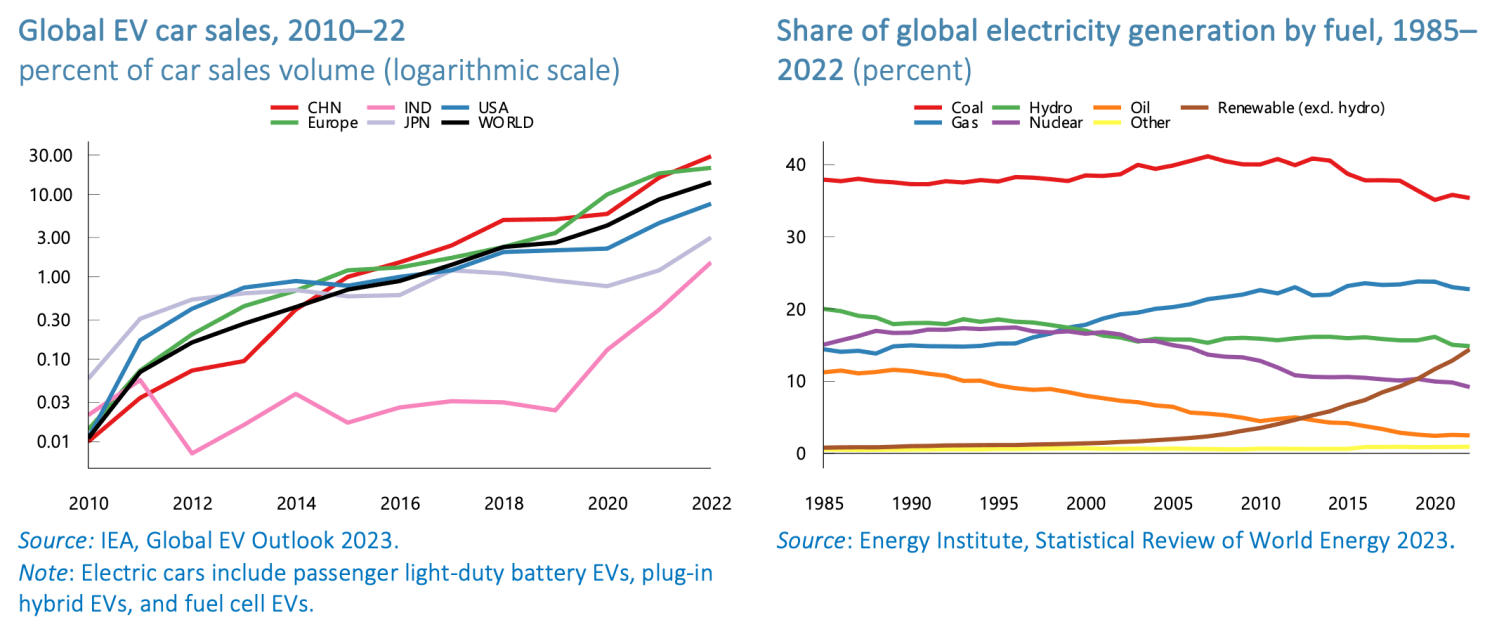

The second self-reinforcing mechanism is network externalities. Until a few years ago, applied research, supply chains and human capital were fully locked into a fossil fuel equilibrium. For example, refuelling a conventional car is extremely convenient due to a dense network of petrol stations. Now, electric vehicles and renewable energy generation have reached considerable market shares and continue to grow strongly globally (Figure 3). As low-carbon infrastructure expands, low-carbon technology becomes locked in. Already, the boom in low-carbon technology is significantly affecting investments in oil and natural gas, and market expectations are changing (Bogmans et al. 2023). Tellingly, even the energy crisis of 2022 did not cause an increase in investments for fossil fuel-based powerplants (IEA 2023). For automobile manufacturers, for example, it is more profitable to invest all research and development funds into one technology in order stay at the technology frontier. Once a critical threshold is reached, a new self-sustaining equilibrium of electric vehicles can emerge (Koch et al. 2022).

Figure 3 Global electric vehicle (EV) sales and electricity generation sources

How should policymakers navigate the race between political backlash and technological progress? First, they should further enable low-carbon technology development. Reinforcing the ongoing shift to clean technology could involve restricting sales of high-pollution goods, taxation, or phasing out polluting technologies (Van Der Ploeg and Venables 2023). The government also has an important role in directing basic research towards technologies – such as green hydrogen and negative emission technology – that are currently still expensive but are needed at a large scale by mid-century. In addition, the diffusion of technology to emerging markets and developing economies needs to be actively supported. Key to this are climate policies, both among innovating countries and recipients of technology transfers, as well as lower trade barriers (Hasna et al. 2023).

Second, climate policies should be designed to ensure fair burden sharing within and across countries, to prevent further political backlash. Surveys show that support for climate policies increases when they are effective, social fairness is ensured, and the policies are communicated well (Dechezleprêtre et al. 2022). Climate policy also needs to be designed in a way that supports international cooperation. On this, the IRA is an interesting example. The protectionist features of the policy package are not cooperative and should not be imitated. At the same time, the package is expected to accelerate low-carbon technology deployment in the US and, as a result, boost clean technology innovation. The net effect on other countries could well be positive. It is hoped that these positive spillovers will be sufficient to avert a harmful round of protectionist retaliation from other countries. But designing climate policies that are fully consistent with the international trading system is possible – and would be even more beneficial.

See original post for references