By Hanhui Guan, Associate Professor at Peking University, Nuno Palma, Professor of Economics in the Department of Economics, and Director of The Arthur Lewis Lab for Comparative Development at University Of Manchester, and Meng Wu, Postdoc Fellow in Economics at University Of Manchester. Originally published at VoxEU.

In early-13th century China, the Mongols introduced the silver standard, the first paper money in history to be backed by a precious metal. This column studies the rise and fall of paper money in 13-14th century China over three stages: full silver convertibility, nominal silver convertibility, and fiat standard. Military pressure in particular led to the over-issuance of money, especially under the fiat standard. Eventually, over-issuance led to high inflation as the dynasty collapsed. China’s historical experience underscores that economic prosperity hinges on the effective execution of sound policies, a process influenced by the political landscape.

China’s economic performance over recent years has raised global concerns. Compared to its past four decades of miraculous growth, the country is now facing an economic slowdown. A property market crisis, stock market slump, consumer price fall, and currency depreciation have triggered anxiety about whether the world’s second-largest economy is entering a recession. The uncertainty about the country’s future also prompts Chinese policymakers to recalibrate some of its policies and seek new sources for growth (De Soyres and Moore 2024). In a recent talk, President Xi emphasised high-quality financial development. According to Xi, an array of elements will accelerate the construction of a modern financial system with Chinese characteristics: a strong currency, a strong central bank, strong financial institutions, strong international financial centres, strong financial regulation, and a strong financial talent pool (Xinhua 2024).

Looking back to Chinese history, we can find that when managing the state, Chinese rulers and their ministers have often been innovative in developing monetary policies and designing financial instruments. As early as the sixth century BCE, the famous philosopher and politician Guan Zhong noted that regulating the quantity of light money (debased coins) in relation to heavy money (fine coins) was a “mutual relationship between child and mother”. Later, in the 11th century, the first paper money, called jiaozi, appeared in parts of China. In the early 13th century, following the conquering of North China, the Mongols introduced the silver standard, the first precious metal standard backing paper money in history. When Kublai established Mongol dominance over Mongolia, China, and Korea, founding the Yuan Empire in 1271, he announced that silver-backed paper money was the sole legal tender. From then on, a paper money economy, backed by silver, replaced a previously chaotic monetary system that mixed various types of paper money with copper coins, iron coins, and silver ingots (Figure 1).

Figure 1 The evolution of currency formats from 600 BCE to the present

Source: Based on von Glahn (2016: 1–294).

In a recent paper (Guan et al. 2024), we study the rise and fall of paper money in Yuan China (Figure 2 shows an example). Based on a wealth of printed primary sources, we constructed a new and comprehensive dataset of the Yuan Dynasty’s annual money issues, price indices, imperial grants, population, taxation, warfare, and natural disasters. The data series, substantiated with qualitative historical evidence, enables us to study the evolution of the Yuan Empire’s monetary regimes, examine the relationship between paper money issues and the government’s fiscal constraints, and investigate the factors that explain the over-issuance that eventually led to high inflation as the dynasty collapsed.

Figure 2 A 1 guan note zhongtong yuanbao jiaochao 中统交钞 issued by the Yuan

Note: Size: 34x20cm. Preserved in the China Numismatic Museum in Beijing. Reproduced with permission.

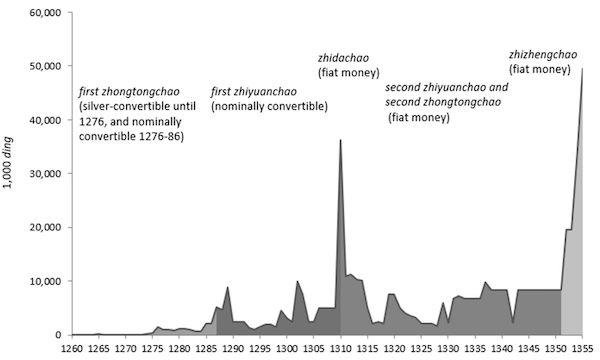

Figure 3 plots the annual nominal money issues. It shows the Yuan government issued four paper monies in total, namely, the zhongtongchao (1260–86), first zhiyuanchao (1287–1309), zhidachao (1310), second zhiyuanchao (1311–51), and zhizhengchao (1352–68). Despite its initially modest quantities, the issuance of the zhongtongchao increased steadily over time. The issuance of the second paper money, zhiyuanchao, was intended to tackle the depreciation of the zhongtongchao. During its 23 years in circulation, the annual issuance of the zhiyuanchao remained relatively stable.

The third paper money, the zhidachao, circulated for only one year, but, compared with the first and second paper money, the size of the issuance was striking. The issuance was a fiscally motivated response to a regime change: it followed the enthronement of the third Khan, Külüg (r. 1307–1311), who seized power through a military coup. However, he died suddenly only one year later, and the zhidachao was abandoned.

From 1311 to 1350, both the zhongtonchao and the zhiyuanchao were reintroduced, and the issuance of paper money varied from 2 million to 11 million ding. The last paper money type, the zhizhengchao, was issued in 1352. Compared with the previous issues, the annual issuances were even more striking. Within two years, the annual issuance soared from 20 million to 50 million ding. Contemporary scholar Wang Yun wrote that unrestrained printing of paper money made it into nothing but empty script (von Glahn 1996: 61–3).

Figure 3 Annual nominal money issues, 1260–1355

Notes: The ding 錠 was the unit of account of silver, with 1 ding of silver being equal to 50 liang of silver. The Yuan government used ding as the unit of account to record fiscal revenues and expenditures, and regulated that 1 ding was equal to 50 guan zhongtongchao. Our last year is 1355 because no data exists after that year.

Sources: See Guan et al. (2024).

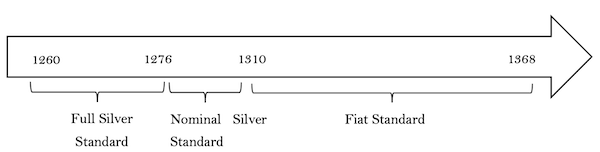

Based on historical narratives, we divide the Yuan’s monetary regimes into three stages: full silver convertibility period (1260−75), nominal silver convertibility period (1276−309), and fiat standard (1310−68). During the first of these, the issuance of paper money was backed by a quantity of silver at a fixed exchange rate. Throughout the nominal silver standard, the new issuance was no longer fully backed by reserves and was only convertible when the local exchange bureau had silver. When the Yuan government began to print the third paper money, zhidachao, in 1310, silver did not play the reserve role, and thus, the monetary system changed to de jure fiat money after 1310 (Figure 4).

Figure 4 Monetary standards during the Yuan Dynasty

Source: Our figure, based on the information in Peng (2020: 501–28).

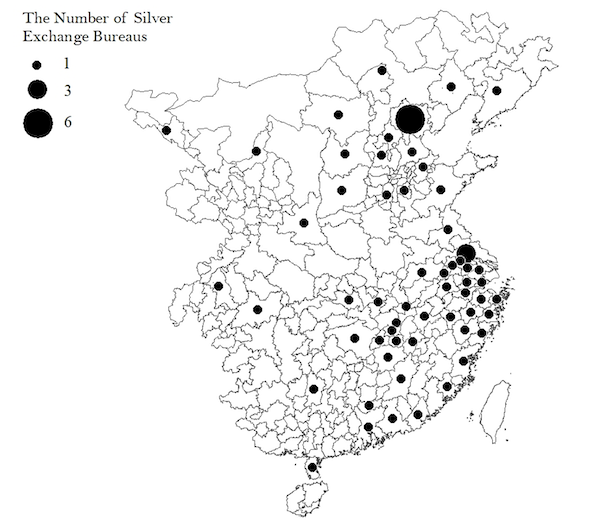

Figure 5 plots the locations of silver exchange bureaus in the 1290s. It shows that the government set up exchange bureaus at provincial-level cities, lu 路, or prefecture-level cities, fu 府 and zhou 州. People could exchange paper money for silver at a discount of 70% to 80% of face value, bring damaged notes, and obtain new notes in exchange by paying a small commission fee of 3%. For people who lived in west or central China, there were fewer places for them to redeem silver. Given the size of China, it would have been costly for people who lived in the remote parts of the west or those who lived in smaller towns to travel to cities to exchange silver.

Figure 5 Location of silver exchange bureaus, around the 1290s

Notes and source: See Guan et al. (2024).

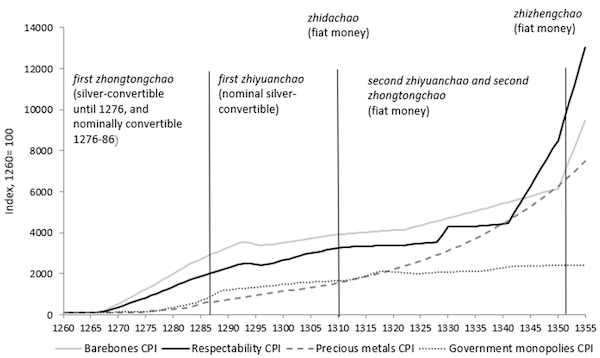

To assess the value of real money issues over time, we construct four price indices: a barebones consumer price index (CPI), a respectability CPI, a government monopolies CPI, and a precious metals CPI. As Figure 6 illustrates, the empire began to experience inflation in the 1270s, when the issuance of zhongtongchao began to grow. The price level also indicates that the 1290s to the 1330s enjoyed price stability. Besides this, we find that during the last decade for which data is available, 1346–1355, the compound inflation rate was 12.7%, corresponding to an approximate doubling of the price level from 1346 to 1355. All four price indices increased over these 96 years but at different magnitudes, as seen in the figure.

Figure 6 Four price indices, 1260–1355

Notes: For methodological details, see Guan et al. (2024).

Source: Our calculations are based on the underlying data collected by Li (2014).

Contemporary observers and scholars documented that warfare, imperial grants, and natural disasters were major causes of the fiscal actions observed. Using econometric analysis, we explored how these factors correlated with the quantities of paper money issued and studied the role of the silver standard in regulating paper money issues. We find that military pressure, particularly civil war, generated fiscal demands that led to the over-issuance of money. By contrast, natural disasters and imperial grants did not trigger the over-issue of money. Warfare was much more likely to increase paper money issues under the fiat standard than during the silver standard period.

Our findings echo studies of the classical gold standard (Bordo and Kydland 1996, Eichengreen 1987, Obstfeld and Taylor 2003). We show that similarly to the classical gold standard, the full silver standard (1260–1275) in Yuan China proved a commitment mechanism that constrained the over-issuance of paper money – while it lasted. The nominal silver standard proved successful given that the price level remained stable into the first half of the fiat standard period. However, by the time the Ming toppled the Yuan Dynasty in 1368, paper money was close to worthless, and towns and cities were resorting to a barter economy (von Glahn 1996: 70). Following the definite collapse of paper money under the fiscally weak Ming regime, China would have to wait several centuries to return to paper money, influenced by Western technology and institutions (Palma and Zhao 2021).

China’s historical experience underscores the notion that sustained success cannot be assumed, both throughout history and in contemporary times. Economic prosperity invariably hinges on the effective execution of sound policies, a process profoundly influenced by the dynamic political landscape.

References available at the original.