Yves here. Below, Wolf Richter demonstrates how fabulously overvalued Tesla stock is. Yours truly is not a stock jockey, but even allowing for that, I have difficulty thinking of any previous case where the valuation of a large-cap company was held aloft essentially based on the cult of personality of its founder. Admittedly, a cohort of Tesla equity buyers have long been true believers; recall how Tesla stock was very richly valued when there were genuine questions as to whether it would ever become profitable.

A second interesting question is how much Musk’s political clout will fade when Tesla stock price falls to more realistic levels, which is quite a long way. Admittedly Musk’s ownership of Twitter is now a big source of his power. But the popular press likes to over-hype celebrities until their fortunes turn, and then pile on them. And Musk has a very thin skin. So a Musk reversal of fortune, even though he is virtually assured to remain comfortably a billionaire, could be an interesting spectacle.

There’s also the related of if and when recriminations will start in the US as to why our carmakers are being so comprehensively shellacked in the EV market by Chinese producers. Back in the late 1970s and 1980s, the US business press regularly and pointedly criticized the loss of US manufacturing prowess, then to Germany and Japan, with fingers pointed at sclerotic US executives. I see comparatively little of this sort of thing now. Apparently we now have the best of all possible elites.

Admittedly, US car buyers will be shielded from that reality of the superiority of China’s EVs as long as possible by tariffs and other import restrictions. But there’s a stunning failure to acknowledge that higher-than-necessary transportation costs translate into uncompetitive labor costs. This effect is admittedly not anywhere as pronounced as for housing. Note that Germany recognized that issue explicitly, promoting (until recently) affordable rental costs and strong tenant rights so that renters could and often did stay in the same flat for decades. The US seems to have lost the plot, that our rentier capitalism, with high housing, healthcare costs, higher education, and now car costs, can’t become competitive unless these are brought under control. With the extreme bloat in those categories, and the industry incumbents wielding great political power, I’m not holding my breath.

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

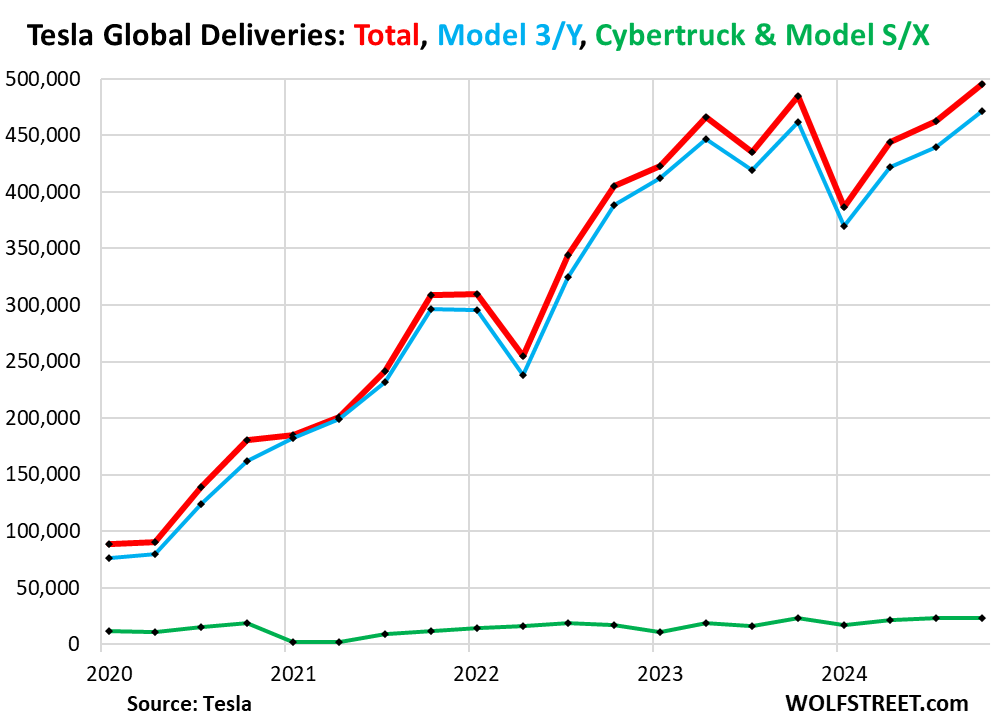

Tesla reported today that global deliveries for the whole year 2024 fell by 1.1% to 1.789 million vehicles, as is Q4 deliveries ticked up only 2.3% year-over-year to 495,570, a new record by a hair. And the growth story is over.

But Tesla’s EV competitors are making hay in the rapidly growing EV market. Tesla’s biggest EV competitor, China’s BYD, announced that deliveries of its battery-electric vehicles in 2024 jumped by 12%, to 1.764 million EVs. In Q4, it delivered 595,413 EVs, up by 13.1% year-over-year, outpacing Tesla’s Q4 deliveries by 100,000 vehicles or by 20%!

Other Chinese EV makers, whose names are familiar in the US because their shares/ADRs are traded in the US markets, announced big gains in EV sales in 2024, including:

Li Auto Inc. [LI], annual sales: +33% to 500,508 EVs; Nio [NIO], annual sales: +39% to 221,970 EVs; and Xpeng [XPEV], annual sales: +34% to 190,068 EVs.

Even US legacy automakers GM and Ford have been reporting big increases in their battery-electric EV sales in the US in 2024 through Q3 (Q4 deliveries will be announced over the next days):

- Ford EV sales in 2024 through Q3, in the US: +45% to 67,689 EVs

- GM EV sales in 2024 through Q3, in the US: +24% to 70,450 EVs

GM killed its popular Bolt and Bolt EUV in 2023 but came out with a bunch of new models that just recently have hit dealer lots. So in Q3, GM’s EV sales jumped by 60% year-over-year.

So this decline at Tesla in 2024 is a sign of trouble at Tesla – is Musk the biggest problem there now? – while overall EV sales continue to grow at a rapid pace, even as ICE vehicle sales have stalled at low levels.

For Q4, Tesla’s deliveries eked out a record at 495,570 vehicles, just 2.3% above Q4 2023 (red in the chart below), including:

- Model Y and Model 3: 471,930 (+2.3% year-over-year, blue)

- Cybertruck, Model S, and Model X: just 23,640 (+2.9% year-over-year, green).

The Cybertruck had been the great hoopla-hope-promise, and it has been in production for a full year, but deliveries are apparently growing at a modest pace:

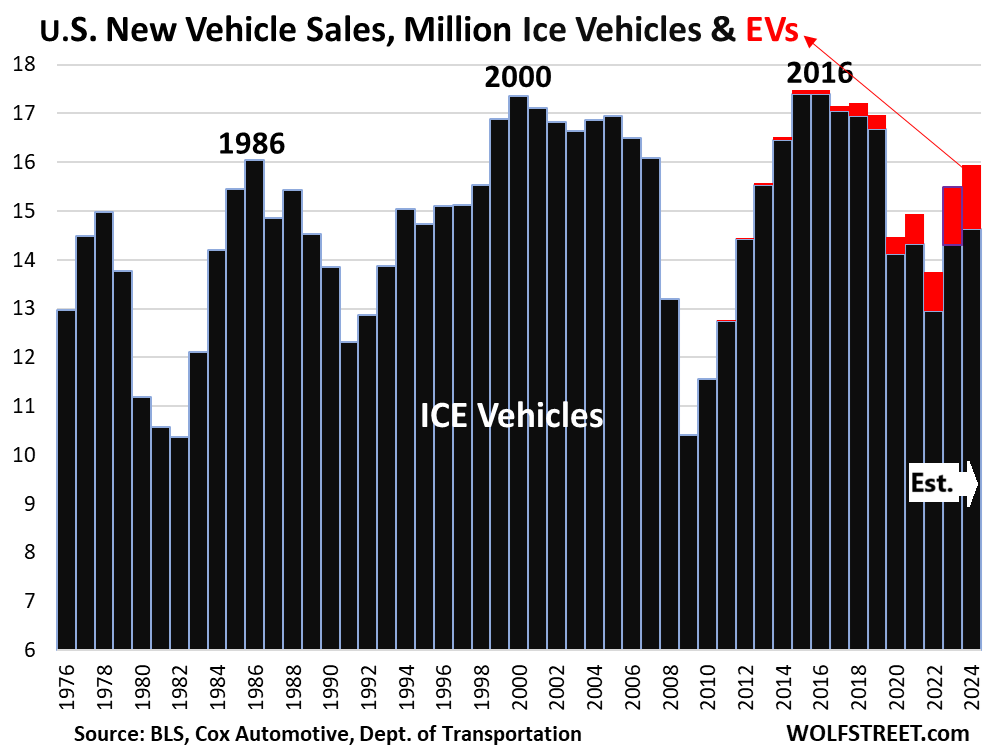

The other automakers will report their US delivery figures over the next few days. So while we wait, let’s assume that EV sales grew by only 10% in the US in 2024, dragged down by Tesla, after having grown by 46% in 2023. Then total EV sales would exceed 1.3 million (EV = red segments), while ICE vehicle sales, including hybrids, would come in at about 14.6 million (ICE = black columns). And Tesla’s role in the EV segment, while still large, is diminishing rapidly, as other EV models surge:

So How Much Should Tesla Be Worth?

With stagnating vehicle sales, losing market share, getting passed by a Chinese competitor (BYD), as other competitors catch up, Tesla is now in the same position as Ford and GM, that trade at P/E ratios between the single digits and maybe 15.

P/E ratios currently:

- Ford: 11.1

- GM: 5.5

- Stellantis: 2.7

- Honda: 7.3

- Toyota: 9.6

- Tesla: 103.2

These legacy automakers with their low P/E ratios are not good deals. They’re not undervalued. That’s where automaker stocks are – and for a good reason.

The auto industry in the US, as you can see from the chart above, has been a no-growth industry for decades, interrupted by big plunges, bankruptcies, and bailouts. Similar dynamics played out in Europe, Japan, and other developed markets.

Only rampant price increases and going forever upscale have allowed automakers to increase their dollar-revenues, even as unit sales stagnated and fell. In fact, because they kept pushing up prices of their models to increase their profit margins and dollars sales, their unit sales have fallen because their models have gotten too expensive.

Tesla is still hyping a lot of stuff that it’s going to blow your socks off with, like it used to hype the Cybertruck, the Semi, and all the other things. The biggest two hype-and-hoopla elements currently are AI and a robotaxi that doesn’t exist yet.

So OK, let’s give Tesla’s hype and hoopla the benefit of the doubt, and say that as Ford trades at a P/E ratio of 11.1, Toyota at 9.6, Honda at 7.3, and GM at 5.5, then Tesla should reasonably trade at a P/E ratio of up to 15 maybe, to be valued for reality. So divide Tesla’s current share price of $378 by about 7, to get a share price of $54, at which point it would trade with at a P/E ratio of about 15, still far higher than the major automakers in the US. It still would be relatively high for an automaker.

I’m obviously just kidding. Wall Street doesn’t care about reality or P/E ratios. Wall Street sells hype and hoopla, and Musk has long known this, and has perfectly played this game, which allowed him to fund and build the company, and its success so far. That was a huge accomplishment.

As Tesla became a profitable global automaker that now sits on $33 billion in cash, it shook up the legacy automakers, forced the entire industry to invest huge amounts in developing and manufacturing EVs and batteries for EVs, many of them in the US, which has entailed a boom in factory construction in the US, etc. etc. So this was all good and very hard to do, and Tesla managed to do it.

But now Tesla is just another mid-sized automaker with stagnating vehicle sales amid EV competitors that are eating its lunch. So it should trade like an automaker.